In last year’s 2018 preview, The Great Housing Reckoning, MB wrote:

…as the year deepens, China’s macro economy will slow and underlying demand for steel will wane, meaning bulk commodities will be very exposed after stocks build in H1. At current prices, most of the global cost curve for iron ore is in the money and all of it is for coking coal. Both still have supply gluts, for iron ore especially, expressed already through unprecedented discounting spreads for lower grade ores.

These forces will do major damage to Australia’s terms-of-trade, pushing it back towards the lows of late-2015, well below official forecasts and dramatically intensifying the income squeeze across the economy. It is, in fact, a potential trigger for further interest rate cuts. Not to mention political chaos as tax cuts are greeted with collapsing revenue forecasts, risking the sovereign rating all over again by year end.

That is not the end of the difficulties that China presents to Australia in 2018. As it slows, China itself will face a renewed monetary dilemma that first played out in 2015.

Its choice will be whether or not to cut interest rates again. That will boost capital outflows and threaten a resumption of falls in the yuan. This phenomenon will be intensified by booming US markets as tax cuts kick in, sucking in capital flows. We do not see China cutting rates but nor does this situation enable it to relax the tough capital controls it has had to apply to control its currency.

This means that for the first time, Australia will face the simultaneous pressure of receding Chinese capital from its housing market and receding demand from commodity markets, weakening the two central pillars of the economy – mining and households – simultaneously.

As already said, we do not foresee a repeat of China’s sharp slowing of 2015. In part that is because China’s external environment will remain firm as the US is strong and the European recovery broadens.

But Australia has benefited very disproportionately from the recent Chinese stimulus and the same will happen in reverse as it comes off.

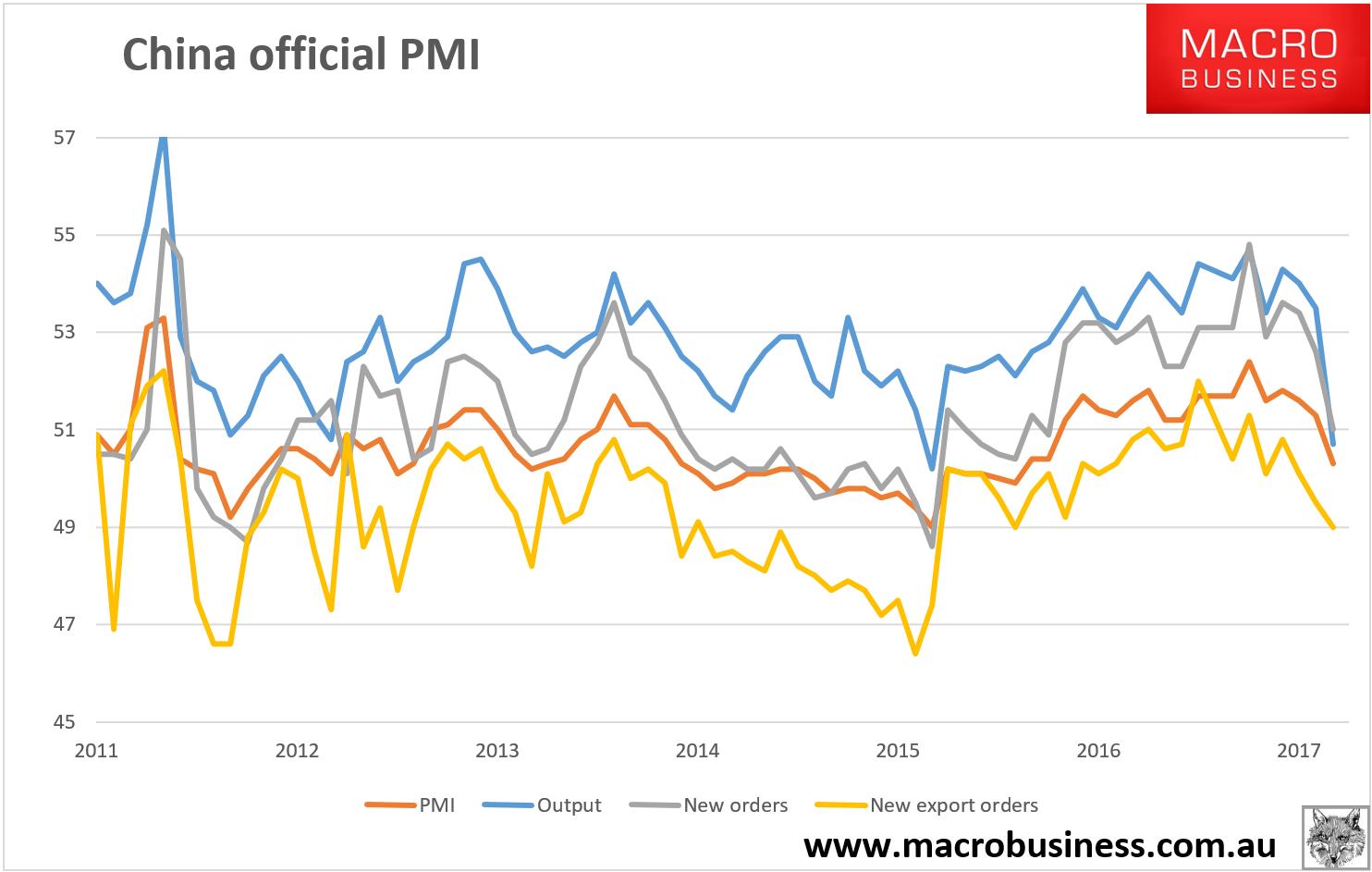

Yesterday we saw the beginning of this in China’s tanking PMIs:

There’s more data confusion ahead as Winter shutdowns pass but the weakening trend is clear.

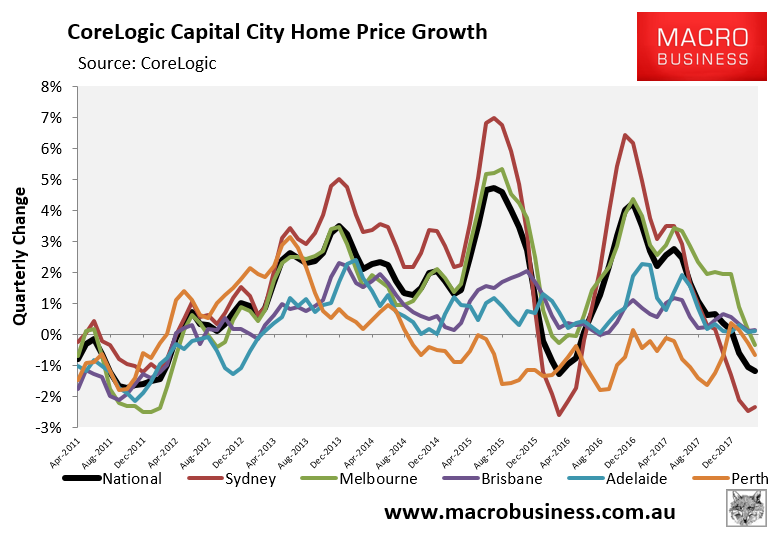

Moreover, CoreLogic released February data showing Australian house prices are falling nearly everywhere in part owing to the Chinese withdrawal:

Anyone who knows the Australian economy knows that it has only two growth engines: houses and holes. The latter provides income that is leveraged in global markets to inflate the former and drive consumption. When both of these engines are shut off, the only thing left is a fiscal lifeline to keep Australia from slipping into recession. That’s already been thrown with some $100bn in infrastructure projects underway and tax cuts planned.

But to think that even substantial fiscal stimulus can carry the economy forward, let alone grow it at the RBA’s and Treasury’s above trend outlook, is only the latest act in the bubble manager’s circus.

Australia is in trouble, again.