In MB’s 2015 Christmas special report, we forecast that 2017 would be “Judgement Day” for the Australian economy, due to four shocks:

a continued global shakeout in commodity prices;

a continued unwinding of the mining investment boom;

falling housing construction and prices; and

the closure of the Australian car manufacturing industry.

As it turned out, 2017 saw the Australian economy perform better than we expected, thanks to the unrelenting strength of the Australian housing market, which registered its fifth year of growth, as well as strengthening immigration levels, government spending and considerable Chinese stimulus.

This better than expected performance meant that Australia chalked up another year of economic growth, meaning the nation has now registered 105 quarters without GDP falling in two consecutive quarters – the definition of a ‘technical recession’. In the process, Australia this year broke the Netherlands’ growth record.

Advertisement

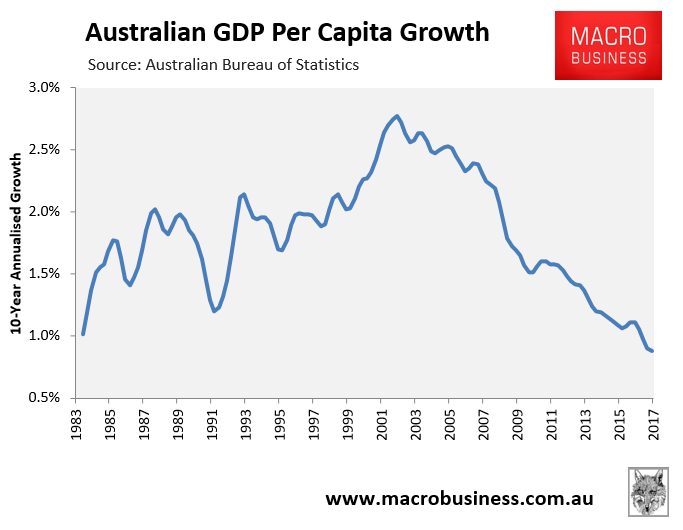

That said, Australia’s real GDP growth of 2.4% in the year to September was lacklustre in light of the 1.6% increase in the population, thus continuing the long trend of falling per capita growth to below the early-1980s and 1990s recessions:

The key question for 2018 is whether growth can accelerate from the current anaemic rate, given the housing cycle is so long in the tooth and the lack of alternative growth drivers? Indeed, we see developments in the housing market as the key determinant of the economy’s performance next year.

Advertisement

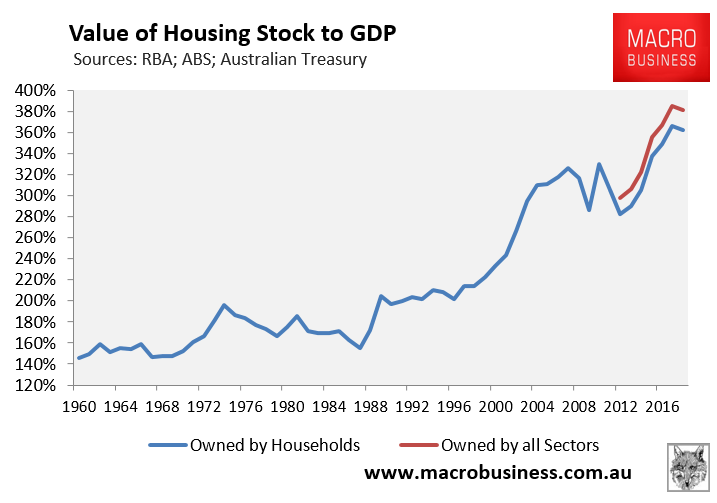

Housing valuations have reached radioactive levels:

After five years of unrelenting growth, Australia’s housing values have hit unprecedented levels and are among the most expensive in the world.

The ratio of Australia’s dwelling values to GDP hit an all-time high 386% as at June 2017 but retraced to 381% in September:

Advertisement

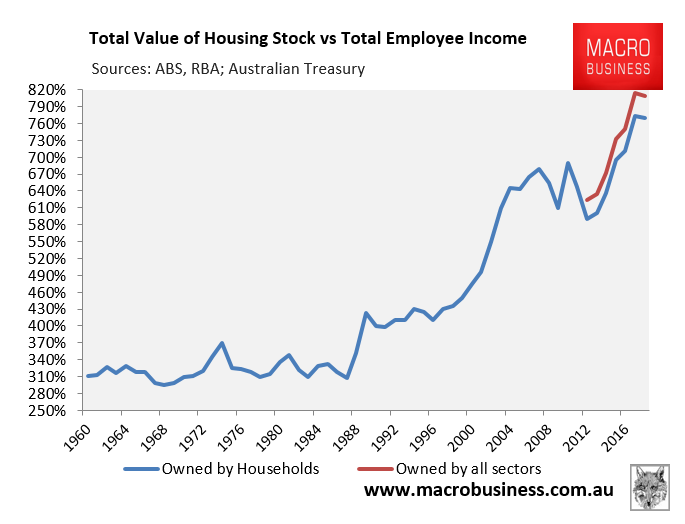

Whereas the ratio of Australia’s dwelling values to employee income hit an all-time high 814% in June 2017 before retracing to 809% in September:

Advertisement

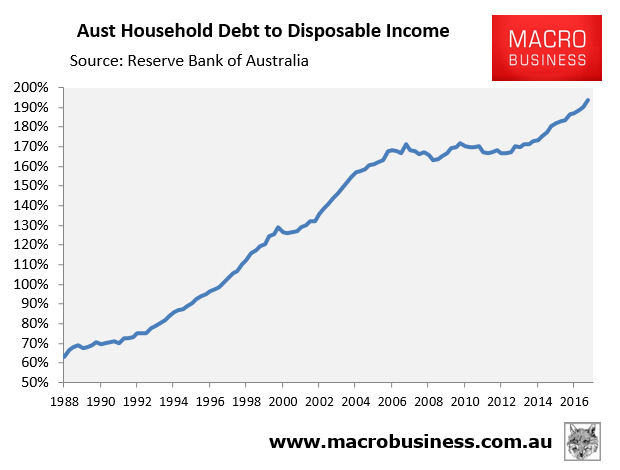

Not surprisingly, Australia’s household debt also surged to the highest level on record in 2017, hitting 194% of household disposable income, or 122% of GDP – the second highest debt load in the world (behind Switzerland):

Apologists for Australia’s housing bubble often claim the market is two-speed, so while Sydney and Melbourne housing is very expensive, the same cannot be said for the rest of Australia.

Advertisement

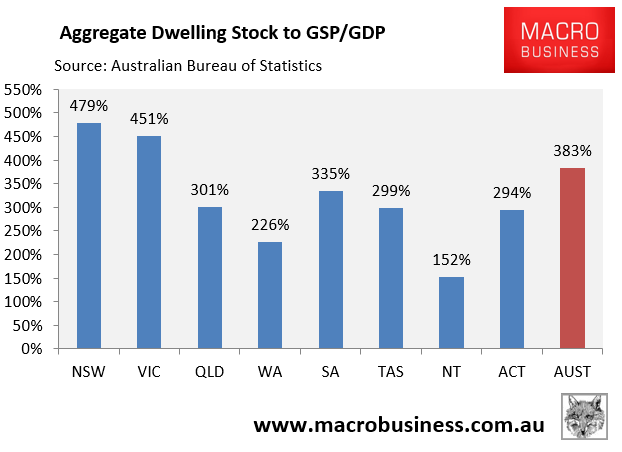

They have a point. As shown in the next chart, New South Wales’ and Victoria’s dwellings were valued at 479% and 451% of gross state product (GSP) respectively as at June 2017, well above the national average of 383%:

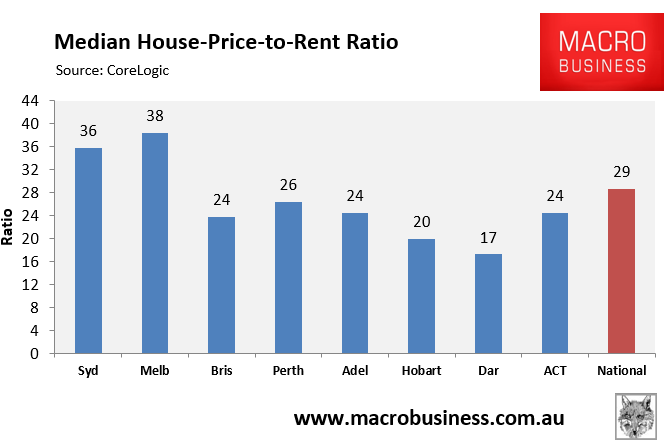

Sydney and Melbourne housing is also by far the most expensive in Australia when measured against rents, easily surpassing the national average:

Advertisement

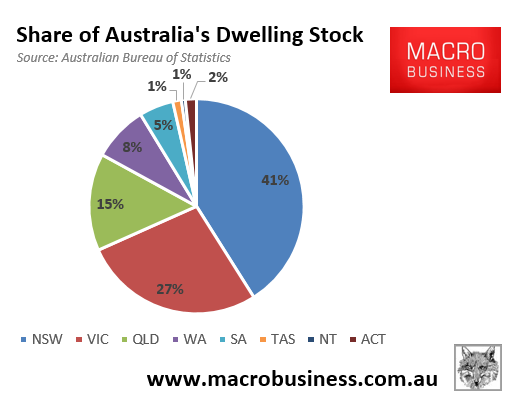

However, while Australia’s housing bubble is indeed concentrated in Sydney and Melbourne, this does not mean that it is less of a problem for the nation as a whole. According to the Australian Bureau of Statistics (ABS), New South Wales and Victoria jointly accounted for 68% of Australia’s housing stock by value as at June 2017, which means that any significant downturn in prices in either major market will have significant ramifications for the broader Australian economy.

Advertisement

Prices are beginning to roll over:

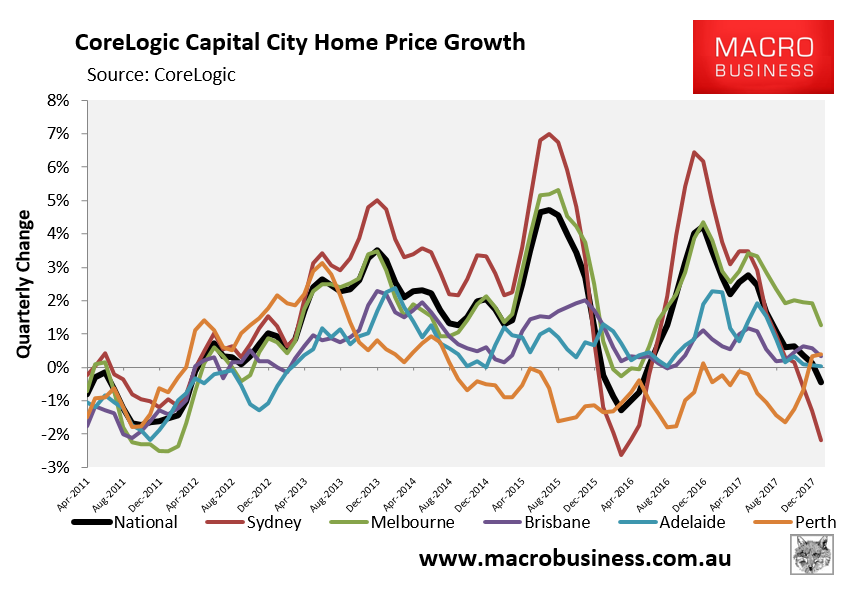

Over recent months, it has become apparent that the Australian housing market is slowing, led by our biggest market, Sydney.

Quarterly price growth has weakened across all major markets, except Perth, with Sydney experiencing the sharpest decline:

Advertisement

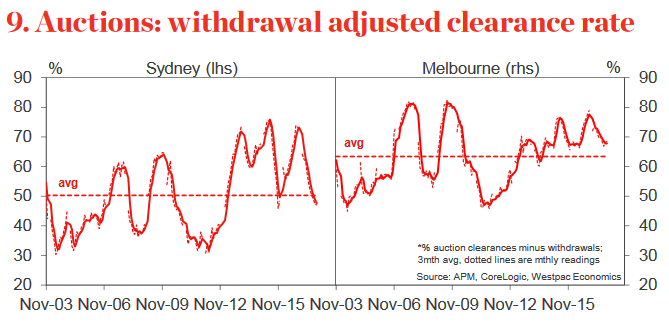

Auction clearances, too, have turned sharply lower, again driven by sharp falls in Sydney:

Advertisement

While one could make the case that Sydney experienced a similar brief downturn in prices and auction clearances in late-2015, which ended up being a false signal, there are reasons to believe that the correction this time around is genuine.

First, the Reserve Bank of Australia (RBA) preemptively lowered interest rates by 0.75% from May 2015, which forestalled the decline in Sydney dwelling prices and sowed the seeds of the subsequent boom. While MB believes the next move in interest rates is likely to be down, this is unlikely to arrive anytime soon as the RBA under Phil Lowe appears determined to see some deleveraging, so not until the economy is experiencing a clear downturn.

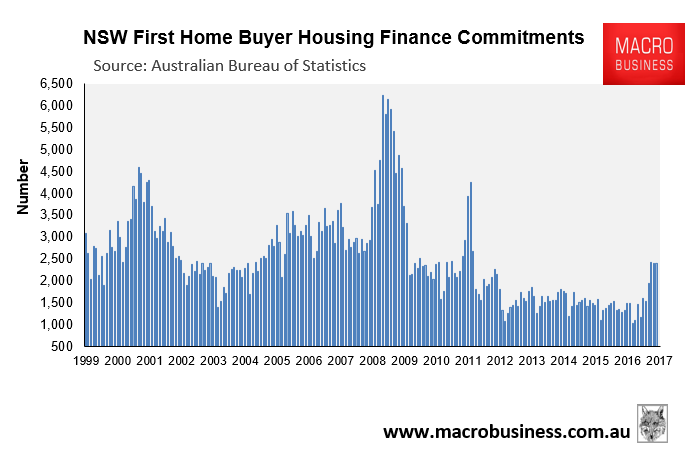

Second, the recent falls in Sydney dwelling prices has occurred despite first home buyer (FHB) stamp duty concessions from the State Government, implemented on 1 July 2017, which has driven an 81% increase in FHB commitments relative to the same time last year:

Advertisement

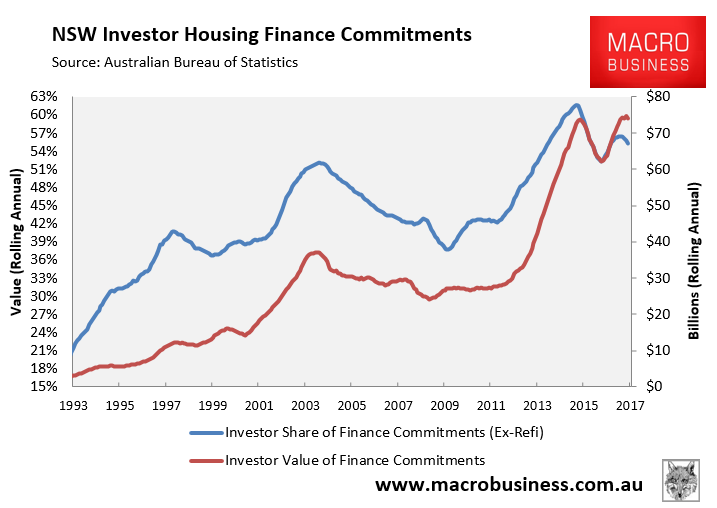

Normally, such stimulus would send prices soaring. However, this boost in FHB demand is being more than offset by a retreat in investors, who dominate the Sydney market and whose demand is now in decline:

Advertisement

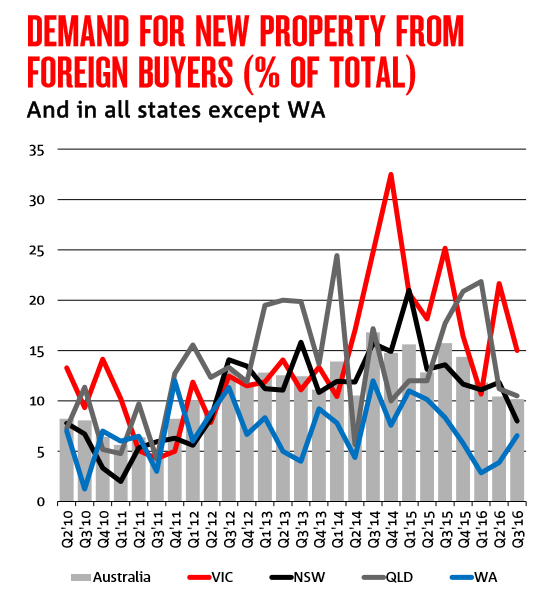

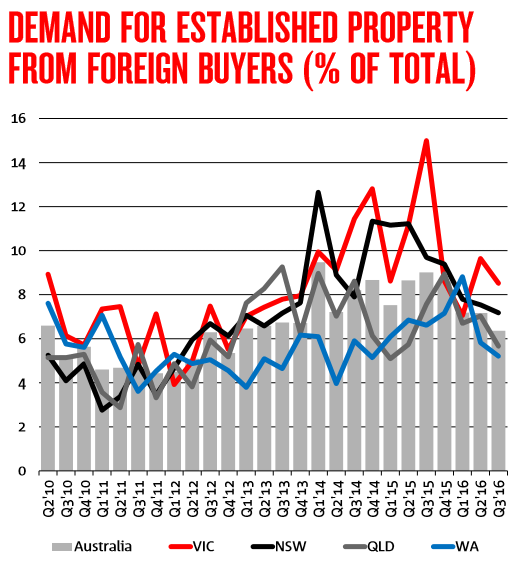

Survey data also suggests that foreign buyers have pulled back sharply from the Sydney housing market:

Advertisement

The New South Wales State Government, along with its peers, has also introduced a stamp surcharge on foreign buyers, which has helped cool foreign demand at the margin and will likely continue to do so, especially in light of the ongoing crackdown against currency outflow from the Chinese Government.

The Australian Prudential Regulatory Authority (APRA) recently announced that it would expand its macro-prudential toolkit beyond its current limits on investor and interest-only mortgages to also include tighter requirements on how lenders assess living expenses and total indebtedness. Therefore, the headwinds facing domestic investors is likely to stiffen.

Melbourne’s housing market is currently far stronger than Sydney’s, although its price growth and auction clearances have also moderated. Given the downturn underway in Sydney, the general lack of affordability, and the tighter conditions for investors and foreign buyers, MB believes that Melbourne dwelling values are also likely to commence falling sometime in 2018.

Advertisement

Again, as shown above, New South Wales and Victoria together account for 68% of Australia’s total housing stock by value, so if/when a correction hits Sydney and Melbourne, its impact on the national economy will be material.

Dwelling construction to fall in 2018:

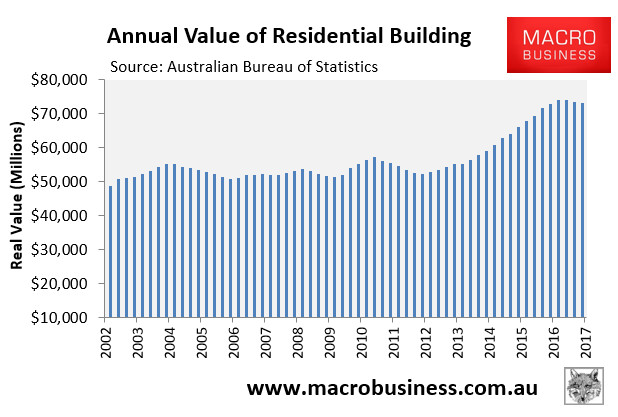

In addition to the budding downturn in dwelling prices, Australia’s epic apartment construction boom has begun to unwind. This is significant because rising dwelling construction has been one of the Australian economy’s major growth drivers since the mining construction boom ended in late-2012:

Advertisement

As shown above, the real value of residential building construction appeared to peak in the March quarter of 2017 and has since declined, albeit slowly.

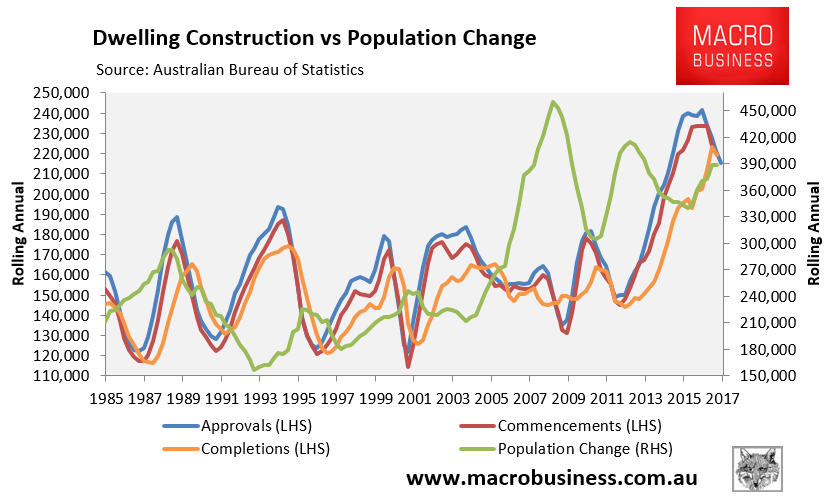

The latest dwelling construction data from the ABS also shows that dwelling approvals and commencements are well past their peak, whereas dwelling completions have a few quarters left to run before peaking:

Advertisement

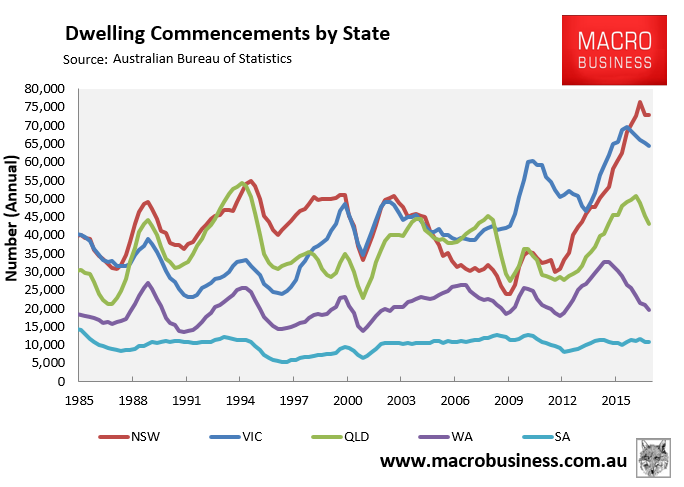

The next chart breaks down dwelling commencements by major jurisdiction and shows that the boom appears to be past its peak everywhere:

Advertisement

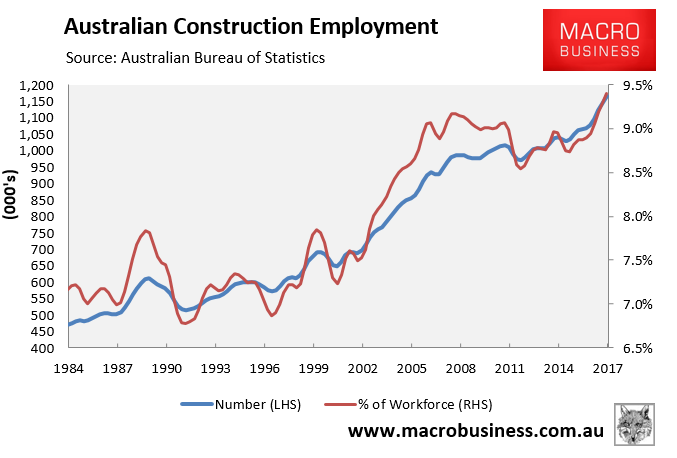

As the dwelling construction cycle turns, it should weigh heavily on employment. There are currently 1.17 million Australians (9.4% of the workforce) employed directly in the construction sector, which has increased from around 700,000 at the beginning of the mining boom:

Over the past few years, the the dwelling construction boom offset the decline in mining investment. However, in 2018, we will see employment activity in the housing construction industry fall, dragging on overall jobs growth and economic activity.

Advertisement

Infrastructure investment may already have peaked:

The other major recent driver of the Australian economy and construction jobs has been the mini-boom in infrastructure projects. Like dwelling construction, this kind of investment only adds to economic activity while the amount being spent is increasing. That is, it is no good remaining on a high plateau of spending, it must increase every year to add to growth.

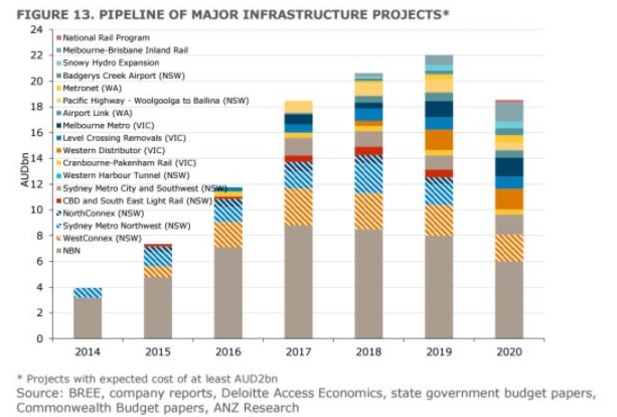

The below chart from ANZ suggests that there is still some modest growth in train for 2018 and 2019:

Advertisement

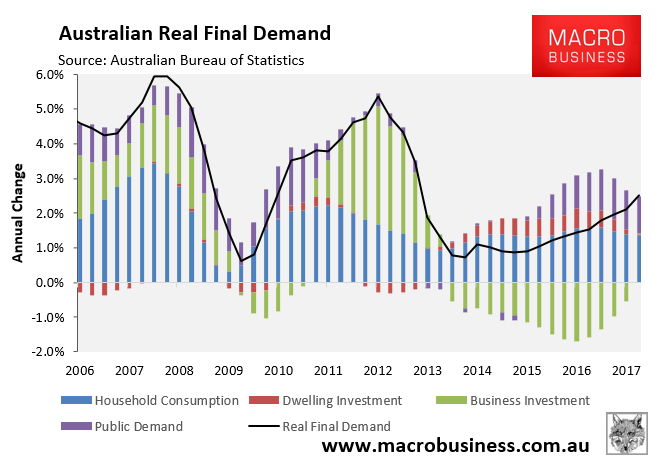

This year has seen public demand contribute 1.1% of Australia’s Final Demand growth, around 40% of the total of 2.5%. But next year the contribution to growth falls dramatically, even more so in 2019, and then begins to take away from growth at double that pace.

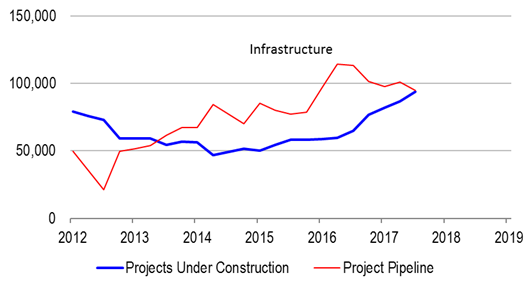

However, just last month Credit Suisse suggested infrastructure investment might already have peaked, following the bigger-than-expected increase in construction work done in the September quarter:

Advertisement

The issue is that the more we use up the infrastructure spending pipeline today, the less growth there is available for tomorrow, unless new projects are added. According to Access Economics, by the end of 3Q, the pipeline of likely infrastructure projects had thinned out to be almost equal to the value of projects already underway. From this starting point, there is negligible growth in the offering. Note that the Access Economics data are consistent in that they compare stocks to stocks, rather than stocks with flows. Therefore, the relative depth of the project pipeline derived from their data is a meaningful leading indicator of growth.

So, Australia is likely facing only modest increases in infrastructure investment in 2018. Either way, there isn’t much in the infrastructure pipeline to offset the pending falls in dwelling investment.

Economy too reliant on Sydney and Melbourne:

Advertisement

The monster-sized booms in Sydney’s and Melbourne’s dwelling construction, prices and infrastructure investment has tilted Australia’s economic activity towards these jurisdictions.

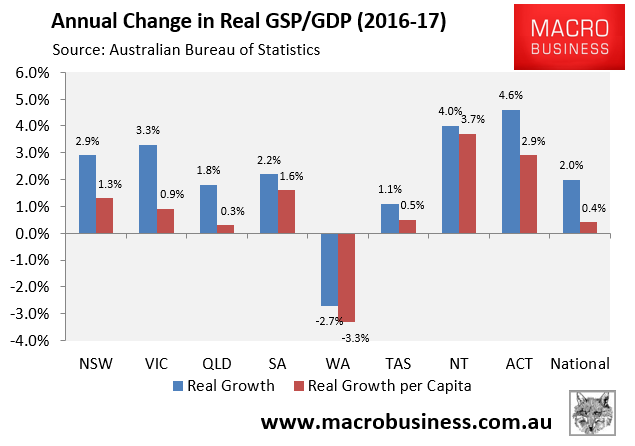

The annual state accounts showed that New South Wales and Victoria were the key drivers of Australian GDP in the year to June 2017, growing by 2.9% and 3.3% respectively; albeit driven to a significant extent by strong population growth:

Advertisement

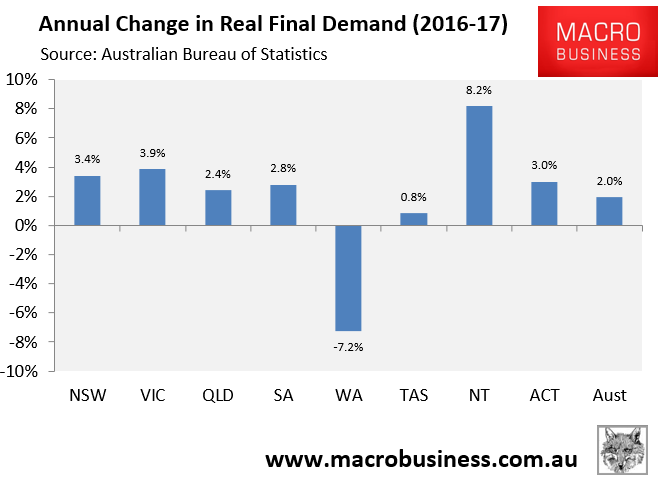

Excluding net exports, their contributions to the nation’s economy was even greater, with New South Wales’ final demand growing by 3.4% in the year to June 2017 and Victoria’s growing by 3.9% – beating all other jurisdictions except the Northern Territory:

With another mining boom unlikely to return for decades, given the massive supply capacity already built, the obvious question is: what will drive economic activity across the Australian economy once the boom in dwelling prices and construction unwinds?

Advertisement

Where will growth come from?

The next chart tracking the contributors to Australian domestic economic activity (final demand) illustrates the dilemma facing the Australian economy in 2018 and beyond:

Advertisement

While the end of the mining investment slump means the headwinds from falling business investment have likely disappeared, and therefore will have stopped being a drag on growth (and will contribute a little) this benefit is likely to be offset by falling dwelling investment. As noted above, public demand – which captures the current infrastructure mini-boom – is unlikely to deliver much growth in 2018 or 2019 before subtracting from growth.

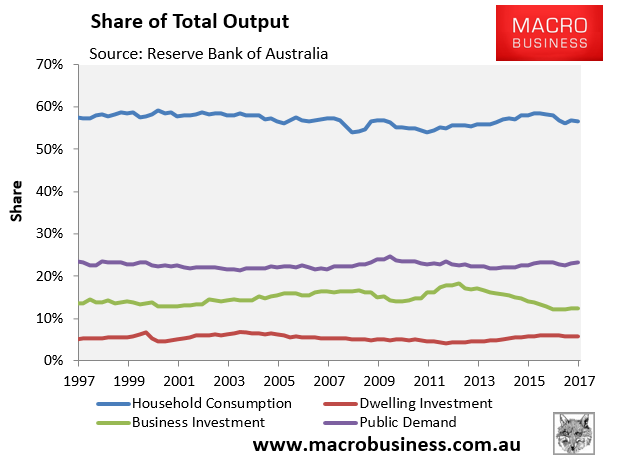

Therefore, Australia’s growth performance in 2018 will very likely hinge on household consumption – the biggest driver economic activity (57% of GDP currently) – that is the hope of the RBA and Treasury.

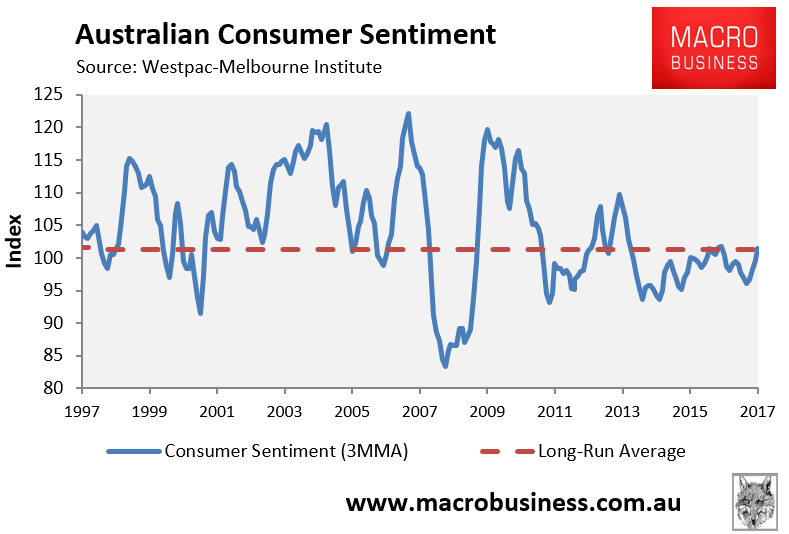

However, consumer sentiment is soft, running at the historical average, despite being so late in the business cycle:

Advertisement

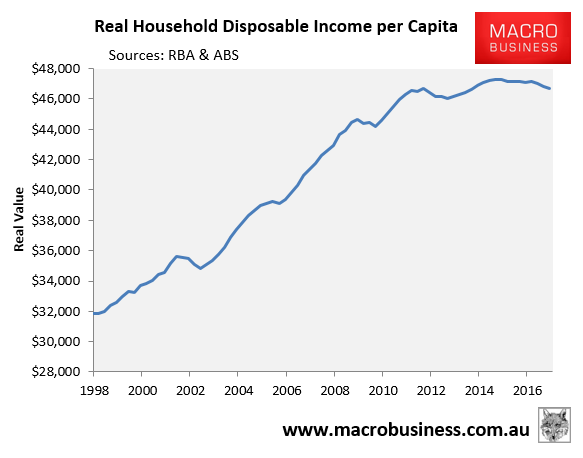

Household incomes are stagnating because of weak wages growth:

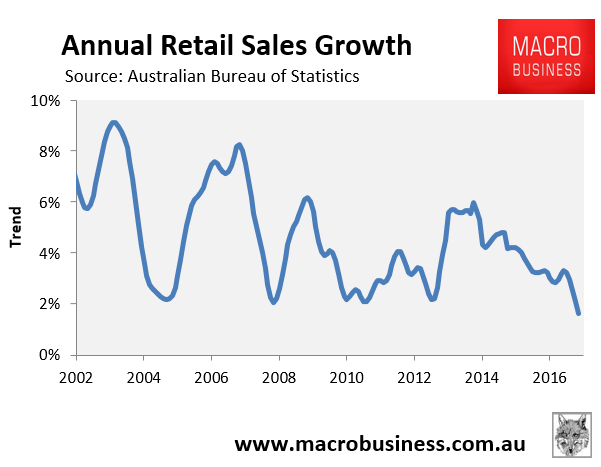

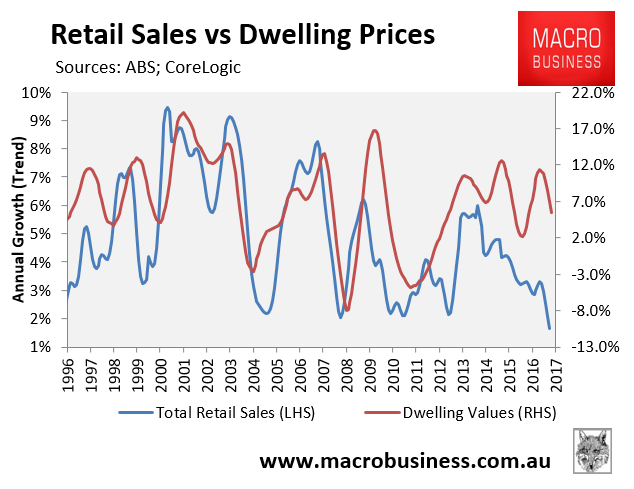

Retail sales growth is anaemic, tracking at the lowest level in the series’ 34-year history:

Advertisement

And debt sits at a record high as a share of income (see chart above).

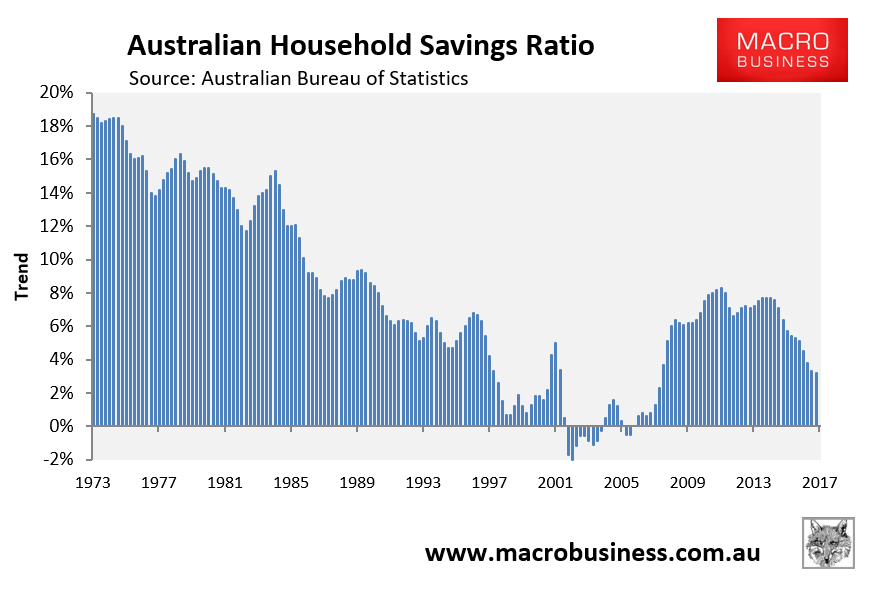

However, it is arguably the falling savings ratio that best highlights how the Australian consumer is stretched.

Advertisement

The saving patterns of households can be a big driver of economic activity. The proportion of income saved directly influences household consumption, which is worth 57% of GDP:

In Australia, the saving rate has been falling since late-2011, currently tracking at the lowest level since the Global Financial Crisis:

Advertisement

This means that expenditure growth over that period has outpaced income growth. As shown above, household consumption growth has been fairly stable in Australia in spite of stagnating incomes precisely because the saving rate has fallen. In other words, Australian households are drawing down their savings in order to maintain a constant level of consumption.

There are obviously limits to this phenomenon. At some point, the household savings rate must stabilise, and falling house prices may well be the trigger for it. And in the absence of a pick-up in wages growth, this means household consumption growth must necessarily fall.

Advertisement

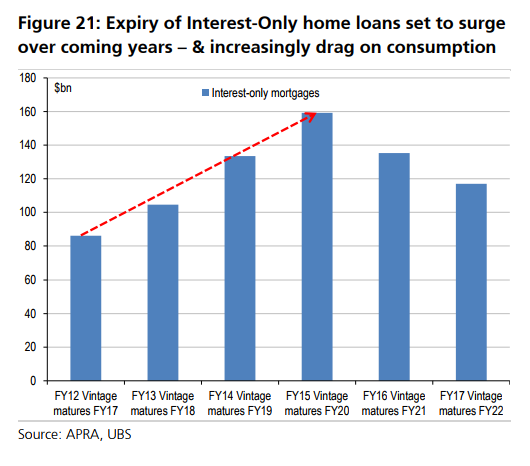

Australian households’ heavy debt burdens obviously adds to the headwinds facing consumption in the absence of stronger wages growth, which will be exacerbated by APRA’s crack-down on interest-only lending. According to analysis by UBS, the volume of interest-only mortgages due to expire will rise to $105 billion in 2018, then $133 billion in 2019, and $159 billion in 2020:

Borrowers switching from interest-only to principle and interest mortgages are facing a 35% to 50% increase in mortgage repayments, according to UBS, representing another drain on household cash flow and consumption.

Advertisement

MB does not see a material pick-up in household income growth. Sure, we witnessed a small wages bounce in the September quarter on the back of the recent minimum wage decision. But this effect is a temporary sugar hit only. Households will need to continue to run down their savings, and increase their debt, in order to maintain current consumption growth – an unsustainable situation.

Historically, there has also been a reasonably strong correlation between dwelling price growth and retail sales:

Advertisement

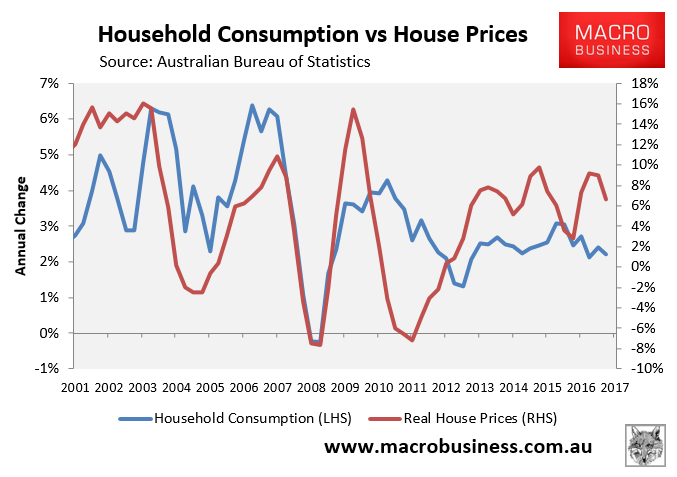

As well as dwelling price growth and household consumption:

Presumably, as dwelling values rise, consumers generally feel more comfortable about their personal finances, which means they feel comfortable reducing the amount of income that they save each period (the so-called ‘wealth effect’), as well as increasing their consumption spending.

However, with Australian dwelling price growth clearly in retreat, led by Sydney, this will act as a constraint on households’ willingness to continue drawing down their savings and leveraging-up with debt, as well as spending.

Advertisement

Therefore, we see weaker household consumption expenditure growth in 2018, and corresponding weaker economic activity.

National income recession to reassert itself:

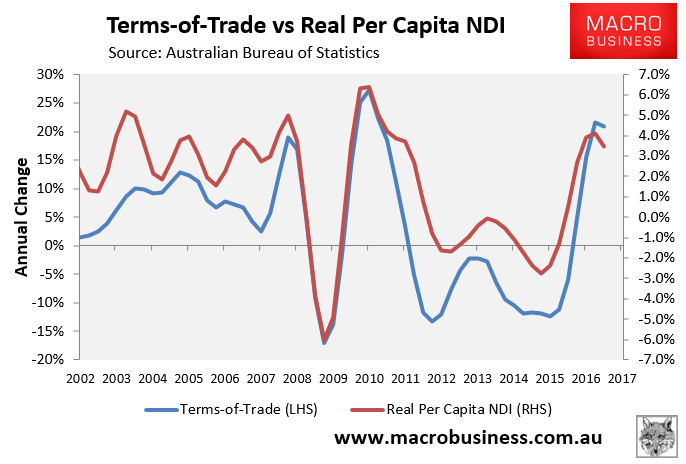

The 2016-17 financial year saw an unexpected mini boom in commodity prices, causing a big rebound in Australia’s terms-of-trade and national disposable income (NDI) growth:

Advertisement

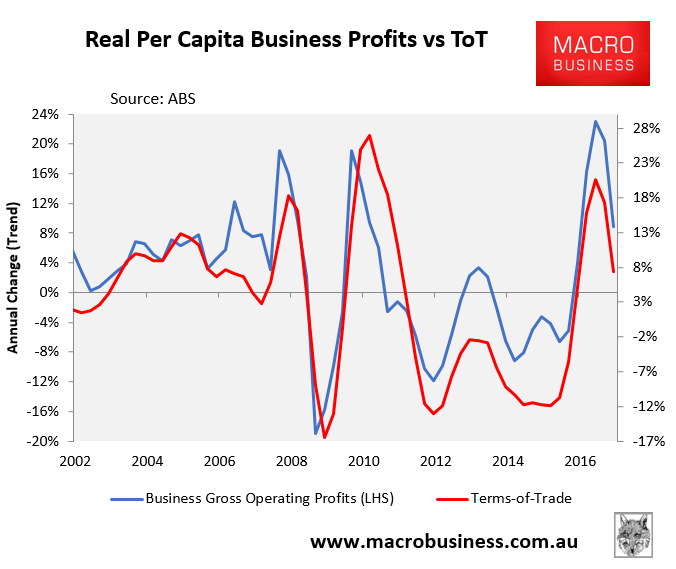

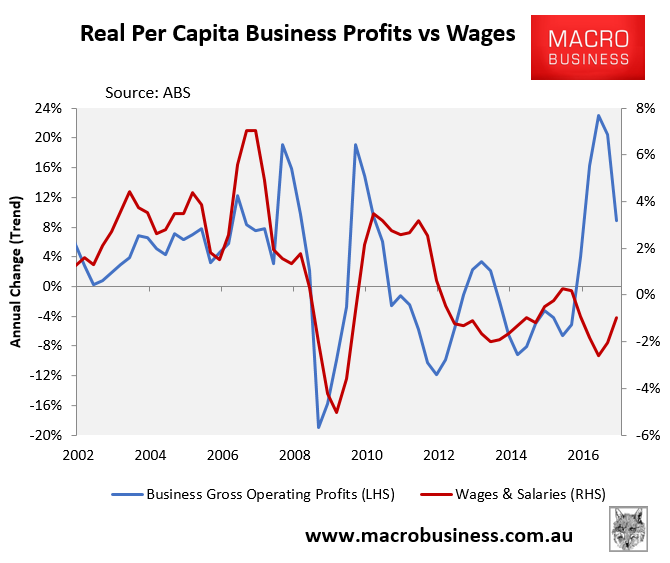

While the fruits of this income mini-boom flowed exclusively to Australian businesses, rather than workers:

Advertisement

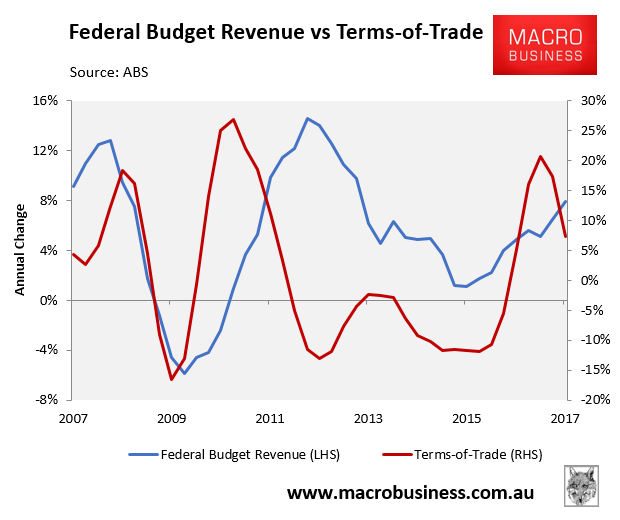

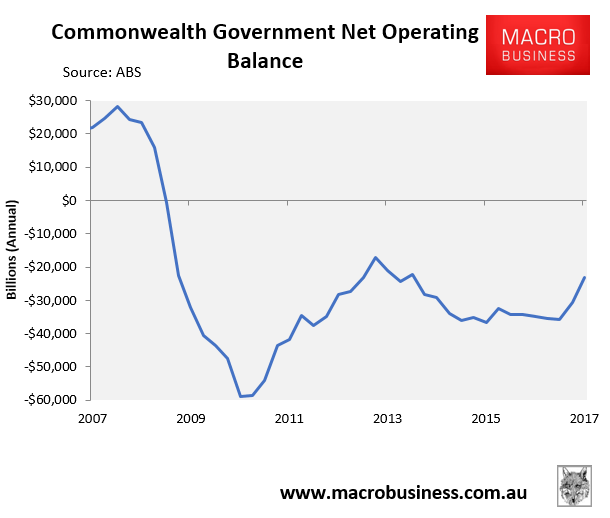

It also filled the government’s coffers with extra tax revenue, thereby helping to reduce the Budget deficit and facilitating the significant public investment that has contributed to Australia’s current economic growth:

Advertisement

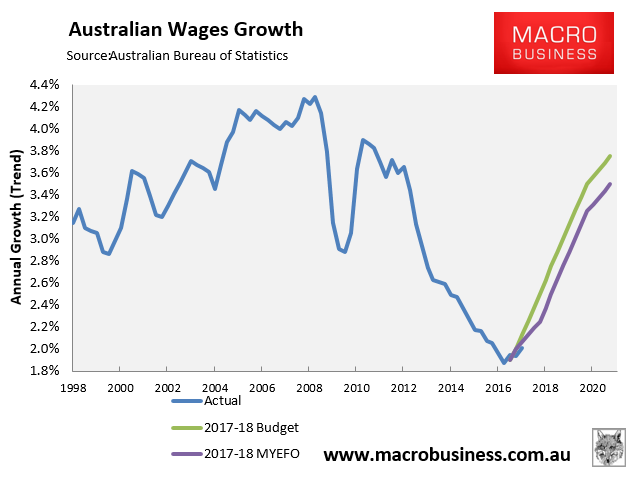

As illustrated above, the terms-of-trade is already in retreat on the back of falling commodity prices, and MB believes that these falls will accelerate in 2018. This means that business profits, national income and the federal Budget will all take a hit. It also all but extinguishes hopes that strong business profits will eventually flow to workers in the form of higher wages, thereby smashing the May Budget’s and the Mid-Year Economic and Fiscal Update’s optimistic forecasts of a wages explosion – a central plank to the federal government’s planned path back to Budget surplus:

Advertisement

The one area of hope for transmission of some of this income to households will be tax cuts, which have already been mooted and are likely to come in the lead up to the 2019 federal poll. But they are unlikely to be large enough to alter the consumer crush that is underway.

Commodity prices to continue falling in 2018:

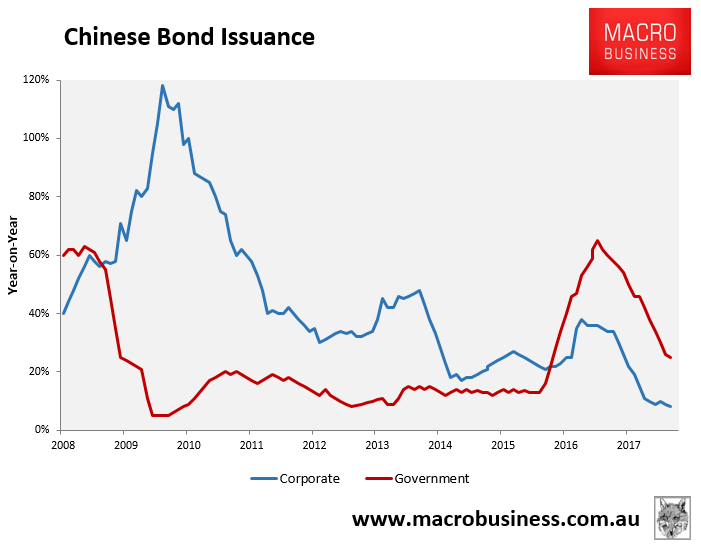

MB does not see the Budget and profits boom lasting much longer. The Chinese stimulus that has driven the big spike is clearly on a downward slope with the government and state-owned enterprise credit binge for infrastructure falling away fast:

Advertisement

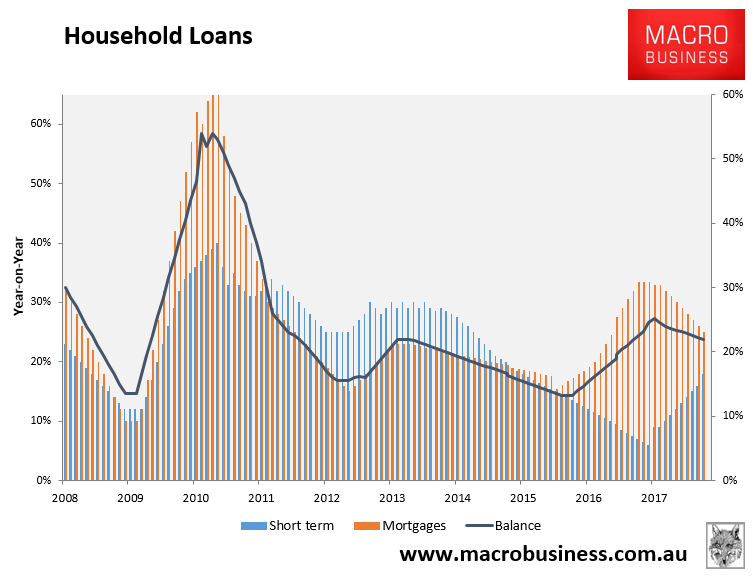

In tandem with a clearly slowing housing price and construction cycle, for which mortgage growth is slowing:

Advertisement

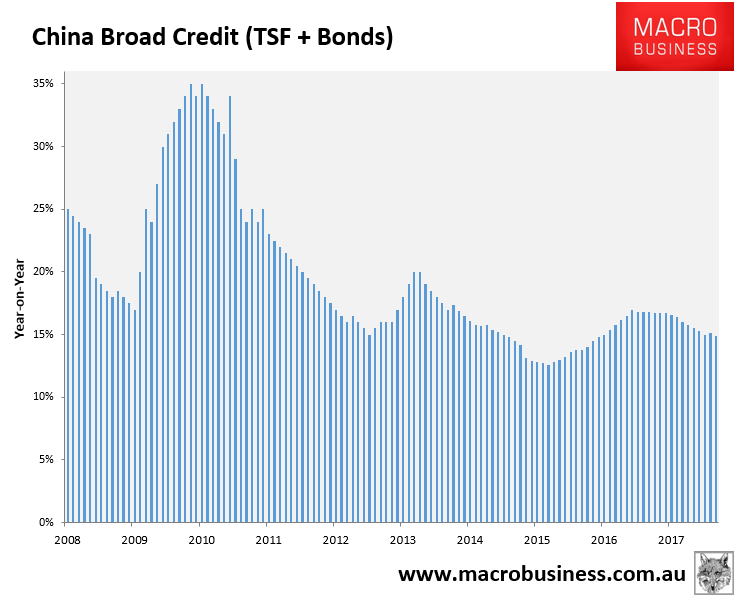

Leading to a clear slowdown in broad credit across the economy:

The most credit-intensive sectors of the Chinese economy are the construction industries that underpin bulk commodity prices and they are slowing.

Advertisement

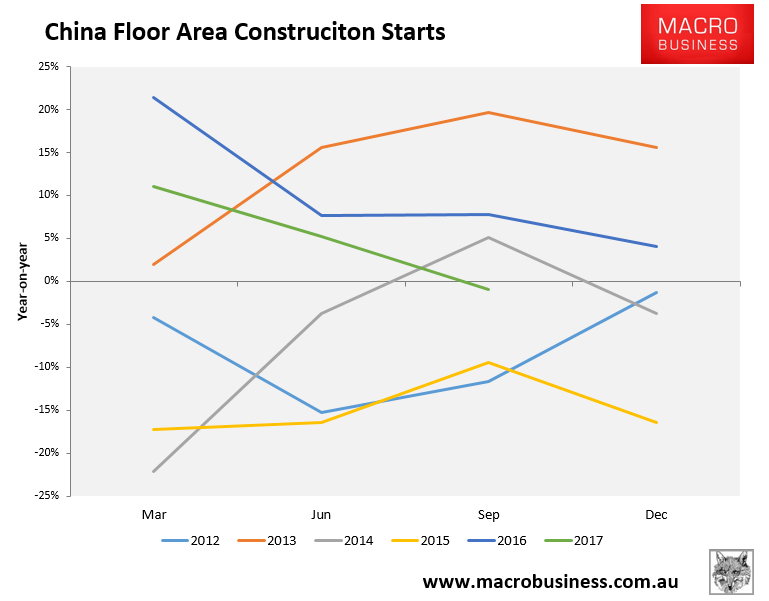

Housing sales are already falling year-on-year and starts recently turned negative as well:

China has used macroprudential policies, not higher interest rates, to slow its housing market in 2017. We expect that to continue in 2018. And the implications are material for bulk commodities.

Advertisement

Iron ore and Coking coal:

We expect iron ore to average $50 in 2018 and coking coal to average $140. But that masks a year of two halves. The first half of the year sees a number of forces combine to support commodity despite the slowing Chinese macro economy:

Winter steel mill shutdowns to combat pollution are limiting output and creating some shortages that will need to be rebuilt;

the first quarter is usually a strong one for rebuilding stockpiles of steel;

global growth is still firm offering external support to China and commodities; and

a La Nina weather event has been declared that raises the risk of weather-related supply events in the Pilbara and Northern QLD.

Advertisement

However, as the year deepens, China’s macro economy will slow and underlying demand for steel will wane, meaning bulk commodities will be very exposed after stocks build in H1. At current prices, most of the global cost curve for iron ore is in the money and all of it is for coking coal. Both still have supply gluts, for iron ore especially, expressed already through unprecedented discounting spreads for lower grade ores.

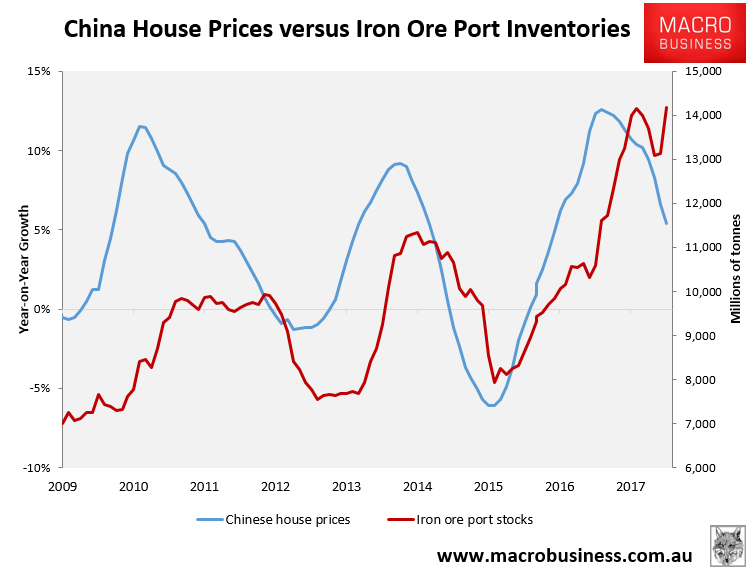

Moreover, Chinese stockpiles of iron ore are very high. In the past when construction cycles have turned down, that has triggered a de-stocking cycle in iron ore. We can see this in port inventories:

Advertisement

In short, once the air clears (literally) around Chinese demand, both bulks will need further supply rationalisation. We expect iron ore to average $40 in the second half and coking coal to average $120. The risk is that both will need to spike lower to cut supply and/or during any destocking pulse.

These forces will do major damage to Australia’s terms-of-trade, pushing it back towards the lows of late-2015, well below official forecasts and dramatically intensifying the income squeeze across the economy. It is, in fact, a potential trigger for further interest rate cuts. Not to mention political chaos as tax cuts are greeted with collapsing revenue forecasts, risking the sovereign rating all over again by year end.

China double-shock:

Advertisement

That is not the end of the difficulties that China presents to Australia in 2018. As it slows, China itself will face a renewed monetary dilemma that first played out in 2015.

Its choice will be whether or not to cut interest rates again. That will boost capital outflows and threaten a resumption of falls in the yuan. This phenomenon will be intensified by booming US markets as tax cuts kick in, sucking in capital flows. We do not see China cutting rates but nor does this situation enable it to relax the tough capital controls it has had to apply to control its currency.

This means that for the first time, Australia will face the simultaneous pressure of receding Chinese capital from its housing market and receding demand from commodity markets, weakening the two central pillars of the economy – mining and households – simultaneously.

Advertisement

As already said, we do not foresee a repeat of China’s sharp slowing of 2015. In part that is because China’s external environment will remain firm as the US is strong and the European recovery broadens.

But Australia has benefited very disproportionately from the recent Chinese stimulus and the same will happen in reverse as it comes off.

The Great Australian Housing Reckoning:

Advertisement

In summary then, we expect 2018 to be difficult for Australia. That is nothing new. Things have been tough since 2011. We do not expect an outright recession but as the year wears on we do expect to see an intensification of the per capita income recession that is the essence of the nation’s budding lost decade.

Indeed, with house prices falling in most cities, this income hit will form a pincer for households that will eventually also dent strangely ebullient business sentiment.

House prices are still not likely to crash. Monetary easing can go another round if and when it needs to. But when it does, that’s the end of it. There is only 150bps of cuts (maximum) left and the banks will keep half of that to boost their margins.

Advertisement

Finally, the global business cycle is now very long in the tooth, global asset prices are very high, central banks are restive, and crazy inflationary manifestations like Bitcoin are emerging from the shadows. The odds are rising that within a year or two the global cycle will falter in a shock.

With Australia almost out of ammunition for monetary and fiscal stimulus, 2018’s struggling economy and slow melt of house prices will be sliding straight towards a steepening cliff.