The BCA is promising the earth:

Ten of the nation’s biggest companies have committed to boost job creation and wages if Malcolm Turnbull’s corporate tax cuts pass the Senate.

The commitment to invest more in Australia was made in a letter to Senators as the government edges closer to winning over key crossbenchers.

“We believe that a reduction in the corporate tax rate, as proposed through the Government’s enterprise tax plan, is urgent and vital to keep Australia competitive,” said the letter, from the Business Council of Australia.

“If the Senate passes this important legislation we, as some of the nation’s largest employers, commit to invest more in Australia which will lead to employing more Australians and therefore stronger wage growth as the tax cut takes effect.”

Signatories included BHP’s Andrew Mackenzie, EnergyAustralia managing director Catherine Tanna, Fortescue Metals chairman Andrew Forrest, Wesfarmers managing director Rob Scott and Woolworths chief Brad Banducci.

Others to put their name to the letter included MYOB chief executive Tim Reed, Qantas CEO Alan Joyce, Origin Energy managing director Frank Calabria, JBS Australia chief Brent Eastwood, and Woodside managing director Peter Coleman.

If the senate cross-bench falls for this then I’ve got a bridge I can sell them. This will just be earmarked investment rebranded or no investment at all. Not that that is the worst point about this Budget vandalism anyway.

Anyone with a half-a-brain knows that the tax cut will be a sugar hit. It will provide a roughly 5% uplift to earnings per share as a one-off. It’s probably worth 300 points on the ASX. Then it’s gone.

But what’s left behind is the $8bn Budget black hole. And this is where it turns from stupid to crazy.

A corporate tax cut is a structural deficit. It was only two years ago that Australia’s term of trade were in free-fall confronting the Budget with sovereign downgrades. Today China is slowing, bulk commodities have astronomical inventories, prices are falling and are going much lower in the next few quarters. We all know what follows. Nominal growth will crater, Budget revenues tumble, and deficits mushroom.

A corporate tax cut into the teeth of this is like waving a red rag in front of the rating agency bull. Which is why the politics of a corporate tax cut now are a mad Hail Mary as well. The terms of trade are going to crash this year, well before the election, and the Coalition could well cut corporate taxes directly into a stripping of the the AAA rating.

The policy calculus is no better. It must be remembered that Australia is not the US. US deficits don’t really matter. But ours do. The Budget guarantees the banks so any downgrade will hike borrowing costs for them just as they are already rising on US tightening. If the deficit blows out, and it will, then those borrowing costs will rise even more quickly and we’ll see prompt out-of-cycle rate hikes.

Before long the cycle will collapse and the lost revenue will have to reclaimed quick smart. It will come not from the companies that have given it to shareholders. It will come from you at the worst possible moment.

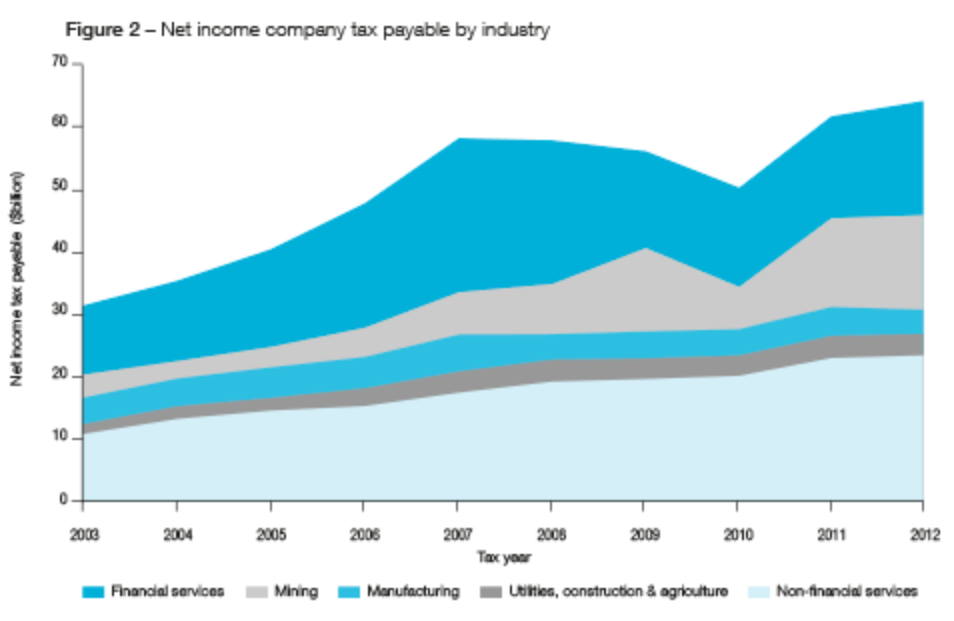

At this stage in the cycle we should be raising taxes to put away the acorns for the looming bust. Especially from mining which is printing money on fantastic margins. It’ll walk away with roughly a third of the total tax cut and won’t invest at all given crashing prices:

The big bulk commodities producers are already radically under-taxed. LNG pays no tax at all. And neither can go anywhere else anyway. The dirt is here! Their one third windfall will tip down the bottomless mine shaft directly to foreign shareholders never to be seen again.

Another quarter will go to the banks. Is anyone watching the Royal Commission? Are we really going to reward a rogue sector with no regard for its home nation with tax cuts? They are already obscenely profitable and are non-tradable anyway.

Sure, other sectors will benefit from a marginal increase in competitiveness. But they, too, are in oversupply and will not invest any more than already planned. A much better way would be Labor’s accelerated write-offs or Pauline Hanson’s payroll tax breaks. For that matter, personal tax cuts would make more sense to fill the demand deficit.

That points to the final issue here which is that the corporate tax cut is a just another fake reform making it even harder to do the real hard work driven by the same ignored principles of centrist mutual sacrifice that MB has pushed for seven weary years:

- deflate wages (including executive) while protecting the vulnerable;

- cut immigration to reduce congestion, the housing obsession and lift low-end wages;

- boost competition;

- unleash innovation;

- improve infrastructure;

- launch mass productivity and tax reform;

- push for a lower currency.

In other words pursue a real exchange rate adjustment until Australian competitiveness and total factor productivity rises enough that external demand and income take off.

Honestly, I can’t believe it has come to this. The Coalition is completely unhinged philosophically, in policy terms and rhetorically. This is the party of Budget conservatism careening off the rails. The tax cut began as an 11th hour brain fart to cover policy emptiness at the last election and now it’s moved front and centre to national interest destruction.

It’s beyond maddening. It’s mad.