Those of us who have looked to the self-interest of lending institutions to protect shareholders’ equity, myself included, are in a state of shocked disbelief…. The whole intellectual edifice [of risk-management in derivative markets]…collapsed last summer.” Asked whether his ideological bias led him to faulty judgments, he answered: “Yes, I’ve found a flaw. I don’t know how significant or permanent it is. But I’ve been very distressed by that fact.”

Australian bank corruption is being exposed by the Royal Commission as equally systemic, across all kinds of business lines and products.

We already know that NAB has outsourced mortgage issuance to gym mangers, the ANZ doesn’t bother assessing the credit-worthiness of borrowers, mortgage brokers are a running joke as risk arbiters and, now, we get this on the CBA:

Advertisement

Special counsel assisting the commission, Rowena Orr, QC, (whose masterful performance at these hearings surely makes her worthy of the nickname “Shock And”) revealed that between 2011 and 2015, CBA sold credit card insurance to 64,000 customers who it knew had no chance of claiming benefits.

Why was this insurance worthless for these customers? Because they were unemployed, on disability benefits, pensioners and students – not working more than 15 hours a week made you ineligible to make a claim.

But, incredibly, CBA’s salespeople never directly informed the customers of this problem in the vast majority of cases.

Jeez, what kind of culture extols the abuse of the most vulnerable? And, moreover, it’s still trying to hide it:

The internal audit conducted by Group Audit and Assurance revealed the bank had serious concerns about wide mis-selling of CCP going back almost three years. The report dated April 9, 2015 found 64,000 customers had been sold insurance policies while un-employed rendering them ineligible to make a claim.

One month later the bank would write to ASIC saying that only 27,800 customers were affected.

“Is it open to me to conclude that it was telling its board one thing and telling ASIC something radically different?” Commissioner Hayne asked.

Advertisement

The products were still being sold up to March 7, 2018.

These are rogue banks. Run by individuals who are arbitraging their own institutions for personal gain. It’s a giant control fraud and the only reason that the rubber has not yet hit the road for the perpetrators is that we guarantee them. Yet we are repaid with corruption twofold, as one would expect when moral hazard enters the equation. John Hempton asks the billion dollar question:

“Property looks expensive and there’s a fair bit of bad lending, but we don’t know if that lending is 2 per cent [of the banks mortgage books] – in which case I don’t care because the banks are so profitable they make that up in no time – or it’s 30 per cent of the book in which case the next five years are going to be fun.”

Advertisement

Obviously the odds heavily favour the latter. As UBS has shown:

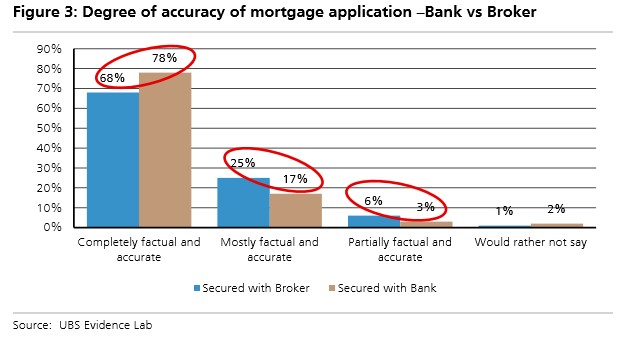

The most significant findings of the survey were (1) Only 72% of respondents stated their application was “completely factual and accurate”. 21% stated they were “mostly factual and accurate”, 5% stated they were “partially factual and accurate” while 2% “would rather not say”; (2) 32% of respondents who secured a mortgage via a broker stated they misrepresented some element of their application, compared to 22% who secured a mortgage via bank distribution; (3) More concerning, 41% of respondents who used a broker in 2016 and misrepresented elements of their application stated they did so based on their broker’s suggestion (vs 13% for bank channel equivalent)…

Of the 344 respondents who stated they misrepresented parts of their application: 14% over-represented household income (18% of those who used brokers and 5% who used bank networks); 13% overstated other assets; 17% under-represented other financial liabilities; 26% under-represented living costs; 11% “other”; 31% “would rather not say”. 12% stated they misrepresented multiple factors.

Unfortunately survey results suggest misrepresentation is systemic with findings similar across the 2015 and 2016 Vintages, price to income levels, LVR, owner occupiers and investors. However, there was a correlation between borrowers who misrepresented their application and: those whose expenditure was broadly equal to their income; stated they are under financial stress; or have missed a debt payment…

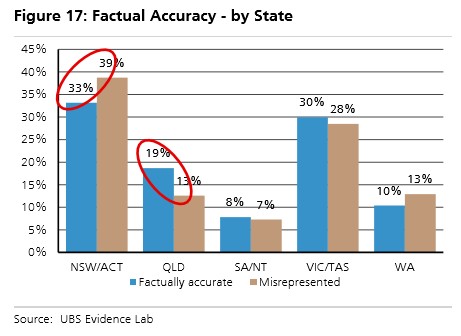

Interestingly customers who come from NSW were more likely to misrepresent their mortgage applications. Notably this continues to be the most buoyant housing market in Australia. Customers from Queensland are more likely to be factually accurate.

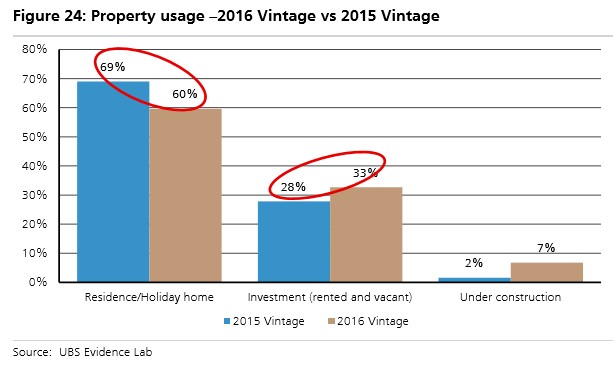

Finally, the use of mortgages for investment purposes accelerated in 2016 contrary to the banks’, RBA and APRA’s data…

We believe this ties in with the ‘areas of less factual accuracy’ section above. This may suggest some customers were not factually accurate when stating the purpose of the loan, especially given the higher interest rate which has now been introduced on Investment Property compared to Owner Occupied mortgages.

What does this mean?

We believe these results are disturbing given: the recent housing market reacceleration; elevated household leverage (186% debt to income); and mortgages accounting for 62% of bank loans.

While banks have tightened underwriting following APRA’s ‘sound lending’ guidance, it does not appear to have prevented applicants ‘stretching the truth’. While low unemployment and rising house prices may help prevent losses near term, more rigorous auditing of applications appears essential, especially via brokers…

We believe it is more important than ever that the banks tighten their mortgage underwriting standards and ensure applications are factually accurate. We continue to see the mortgage broker network as a potential area of weakness in this process.

The only thing holding up the control fraud now your guarantee of it. That’s why I am of the view that it is approaching its end. With RBA all but out of ammunition and the Budget headed for all kinds of pain as China goes ex-growth the guarantee is next to worthless.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.