More on looming out-of-cycle rate hikes today from Deutsche:

Over the past 3 weeks the bills-OIS spread has widened materially, rising by around 20 basis points to reach 48 basis points.

On our estimates a 25 basis point increase in the bills-OIS spread could reduce net interest margins by 2 to 5 basis points on an annualised basis, and impact net profit after tax by between 2 and 4 per cent.

These estimates are prior to any mitigating actions by the banks, such as repricing of business loans and/or mortgages.

A higher BBSW rate is likely to increase the asset yield on certain business loans. We assume one third of corporate/commercial loans and all institutional loans are influenced by BBSW.

Based on several simplifying assumptions, we believe NAB could be most impacted among the majors. This is driven by its higher reliance on wholesale funding versus peers, combined with a higher exposure to SME lending rather than institutional. ANZ would be least impacted due to its overweight exposure to institutional.

Whoever it impacts most is irrelevant. If one hikes they’ll all hike.

Banks are already operating on razor thin profit growth expectations. This wipes them out so loans will have to be repriced. It’s not imminent but if spreads remain where they are then it isn’t far off either, as CS said yesterday:

In our recent article “Credit market tightening could overshadow macro-prudential loosening” dated 23 March 2018 (attached), we argue that:

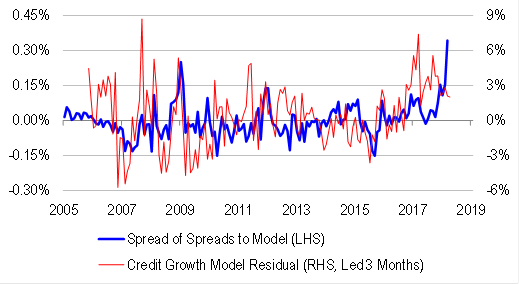

AUD interbank credit spreads have widened very aggressively, and this widening cannot be explained by conventional macro factors. But we have looked at something unconventional – the excess of credit growth relative to banks’ reported lending standards. We find that when credit growth is excessive, interbank spreads tend to rise, presumably because excessive credit growth brings about default risks. And over the past few years, credit growth has been well ahead of our proprietary credit conditions index. Widening USD LIBOR-OIS spreads may not be systemic – but it is an open question as to whether widening AUD spreads might be.

Regardless of why credit spreads are widening, they are likely to have a negative impact on Australian growth via the cost, and availability of credit.

…This sort of macro environment carries with it de-leveraging risks. And de-leveraging risk undermines the efficacy of naïve value factors. Earnings, dividends and book values stop anchoring asset prices during de-leveraging episodes. Rather, asset prices drive fundamentals. Perversely, higher multiple stocks may actually do well to the extent that they carry strong quality, or defensive characteristics.

Advertisement

Given the Royal Commission is the likely driver of the widening spreads, it has the banks caught in a pincer with rising funding costs but political blow back if they hike rates as an offset.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.