ABC 7.30 Report does ‘liar loans’ and the interest-only time bomb

ABC’s 7.30 Report last night tackled irresponsible lending by the banks, which is expected to be under the spotlight of the Banking Royal Commission today.

The segment features a middle-aged nurse, Linda Schmidt, who borrowed millions of dollars interest-only to purchase investment properties around Perth and is now facing financial ruin.

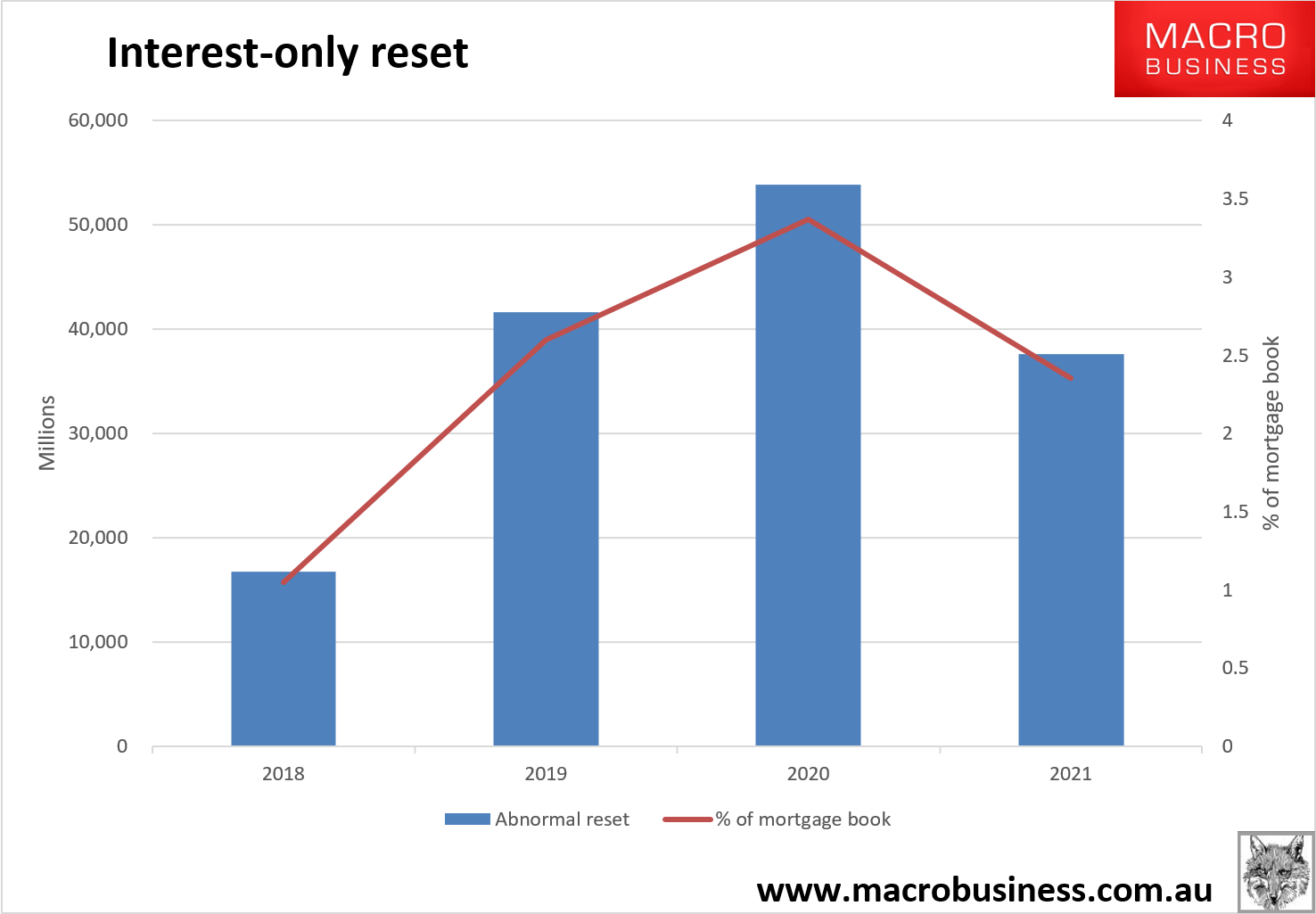

The segment also features Digital Finance Analytics’ Martin North, who discusses the interest-only reset time bomb (chart below). North expects a 10% to 15% drop in property prices over coming years as a result of some $150 billion in interest-only mortgages having to reset to a higher interest rate, causing forced sales.

North says the situation facing Australia is similar to the US sub-prime reset experience:

Pass the popcorn!