Via News:

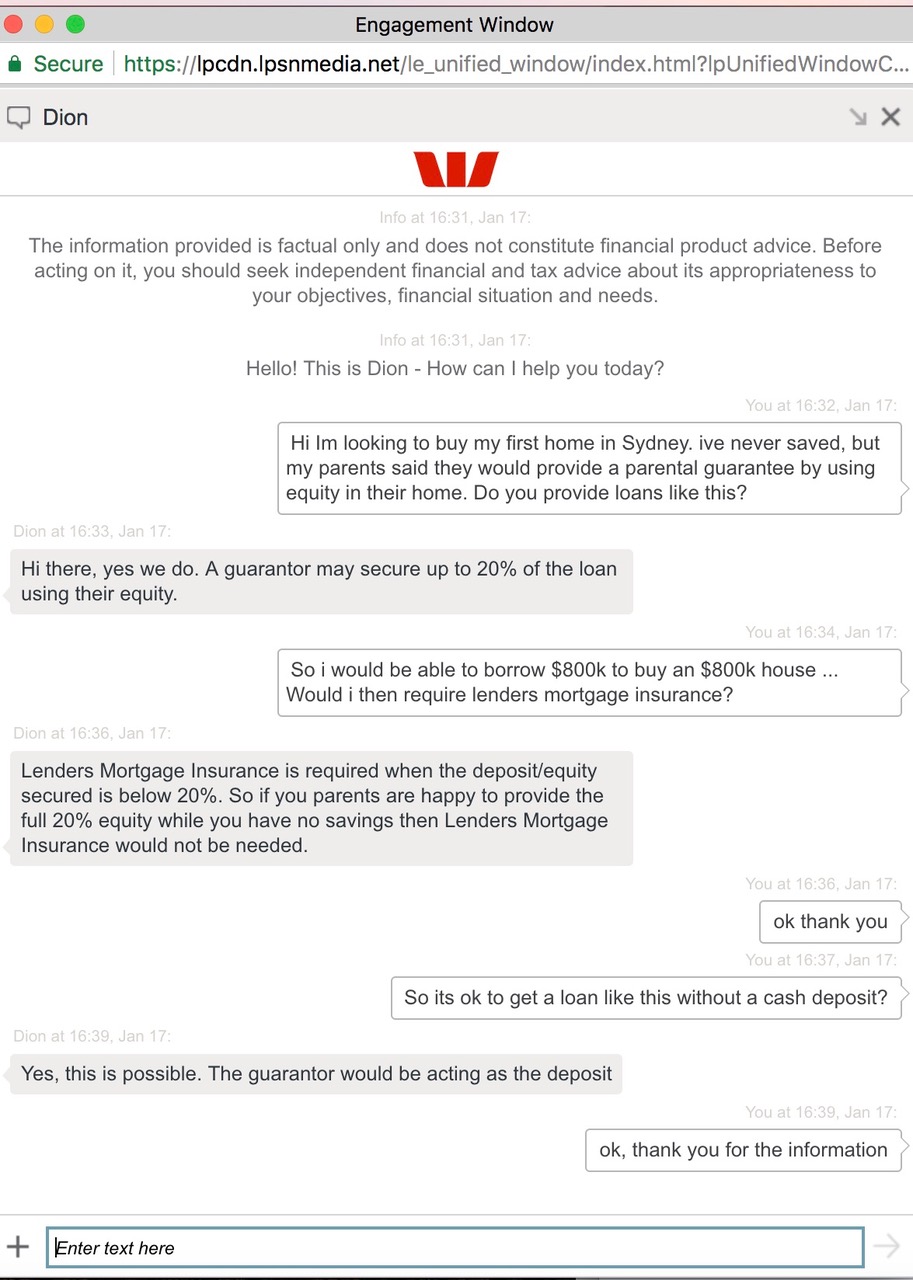

COMMONWEALTH Bank is encouraging struggling first home buyers to borrow 100 per cent of the value of a property using their parents’ home as security, describing the highly risky strategy as a “great option”.

…The LF Economics founder, who described the undercover chat as “cheeky”, said all the banks did the same thing but singled out CommBank and Westpac as the “cowboys”. He provided a similar chat log involving a Westpac sales agent.

“The reality is it’s possible in Sydney to eat your smashed avo and still get into the housing market because you don’t need to save,” he said.

“When people wonder why there are so many first home buyers out there who can afford to buy a property in Sydney, look no further. People are just using equity instead of cash. No one appears to have the cash to buy these places, they’re using equity because everyone’s house prices keep going up.”

On Wednesday, official data showed the share of housing loans issued to first home buyers hit a five-year high, rising to 18 per cent in November 2017, following stamp duty discounts in NSW and Victoria introduced in July.

Mr David said the housing market “keeps on using the unrealised capital gains of existing homes to leverage against buying another property”. “I’ll leave that to people’s opinion on whether they think that’s Ponzi-like or not,” he said.It comes amid growing warning signs for Australia’s housing market, with the country’s household debt-to-income ratio hitting 200 per cent for the first time after the Australian Bureau of Statistics revised its official figures.

The change, which required the accurate measurement of property investment by self-managed superannuation funds, brought the figure up from 194 per cent, The Australian reported. Total household debt now sits at nearly $2.5 trillion.

Mr David said the worst-case scenario would be losing two houses instead of one if the borrower found themselves unable to meet repayments, either through rising interest rates or the sudden loss of a job.

Witness the smiling face of ponzification: