Australia’s housing market is set to weaken further this year, with both prices and building activity to fall, according to Morgan Stanley.

The global investment banking giant has constructed a leading index to try and predict the future direction of residential building and home prices in Australia.

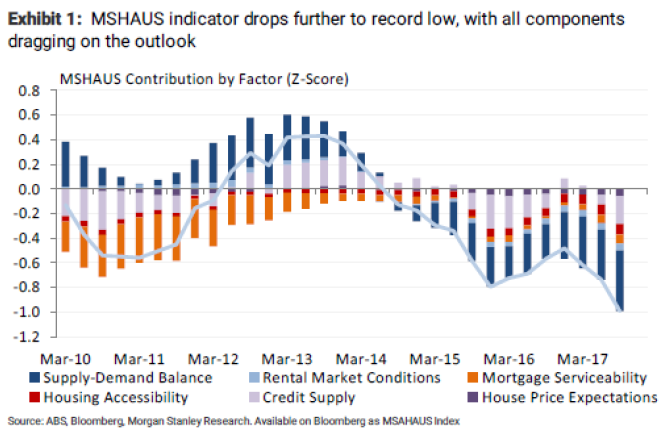

The MSHAUS index is designed to lead activity by three quarters, and looks at a range of factors that influence housing market activity and prices, including the supply-demand balance, housing accessibility, rental market conditions, credit supply, mortgage affordability and house price expectations.

All of these were negative in the third quarter of 2017, leading the index to a record low of -1.

This indicates that the home price falls seen in Sydney in late 2017, and the weakening price gains in Melbourne and many other formely buoyant east coast markets, are likely to continue.

“Given that our model is calibrated to lead activity by three quarters, this quarter’s print suggests that we can expect a further weakening through 2018,” the bank’s analysts noted.

“This is a substantial risk for the economy, given the vulnerable state of the consumer and their exposure to housing.

“In the third quarter of 2017, average household leverage reached 200 per cent of disposable income (138 per cent of which is mortgage debt), with average house prices now 8.2x average incomes”…

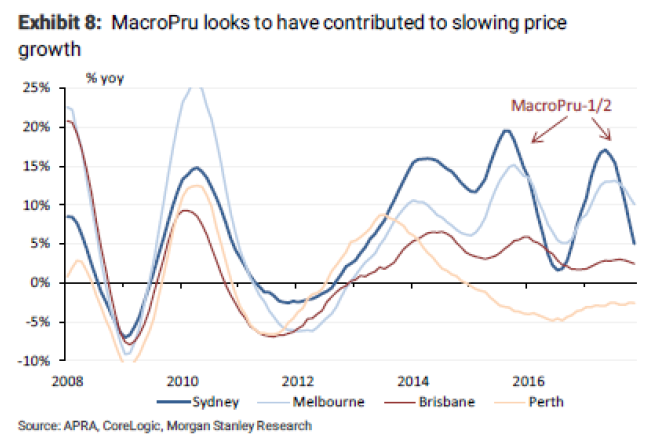

“Since the implementation of the latest round of macroprudential measures in mid-2017, the share of new interest-only (IO) loans has declined sharply from 36 per cent to 16 per cent,” the analysts observed.

“The sharp decline in interest-only lending suggests banks and borrowers are responding quickly to tighter supervision and higher rates on IO loans.

“The move to principal and interest loans incurs a sharp increase in debt-servicing payments, on average reducing disposable income by around 7 per cent.

“Additionally, our Alphawise survey suggests that interest-only borrowers are relatively high risk, as they are more highly leveraged, have fewer savings and are more likely to manage costs through credit cards and consumer finance.”

The particularly striking effect of home lending limits on the Sydney market, and to a lesser extent Melbourne, is likely due to their relative expensiveness, meaning borrowers in those cities need bigger loans to buy property.

If banks cut bank the amount they are willing to lend in response to regulatory restrictions then many prospective buyers are knocked out of the market at current prices…

One factor that Morgan Stanley argues is preventing an even steeper decline for major east coast housing markets is population growth, driven by net migration of 245,000 people over the past financial year.

“This has supported demand for housing, and reduced the surplus created by the rapid increase in supply over the past few years,” the analysts noted.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.