It sure is on a tear again:

Some will put this down to global synchronised growth boosting commodity prices. But how real is that when we know that Chinese credit is slowing and growth will follow in short order? China consumes pretty much half of all commodities.

No. The major driver of commodity prices (and the AUD) right now is the weak USD:

And that, in turn, is being driven by last year’s “policy convergence” trade charging into the EUR, which makes up half of the USD index (DXY):

This is being driven by strong growth on the Continent and hawkish hopes for the ECB. But the EUR/USD is already at its long term average so how much further can this trade run given the relative outlooks for the two underlying economies still heavily favour the US? Respective stock markets are also signaling such. Moreover, the two economies have the same inflation rate but Europe has fewer growth and price drivers given:

- 8.2% unemployment versus 4.2%;

- US fiscal stimulus is more potent;

- a shale oil boom looms for the US not Europe,

- the US is clamping down in immigration more;

- the EZ is more exposed to a slowing China than the US;

- the Fed is much more likely to tighten faster than is the ECB and is less currency sensitive, and

- tax repatriation is underway in the US.

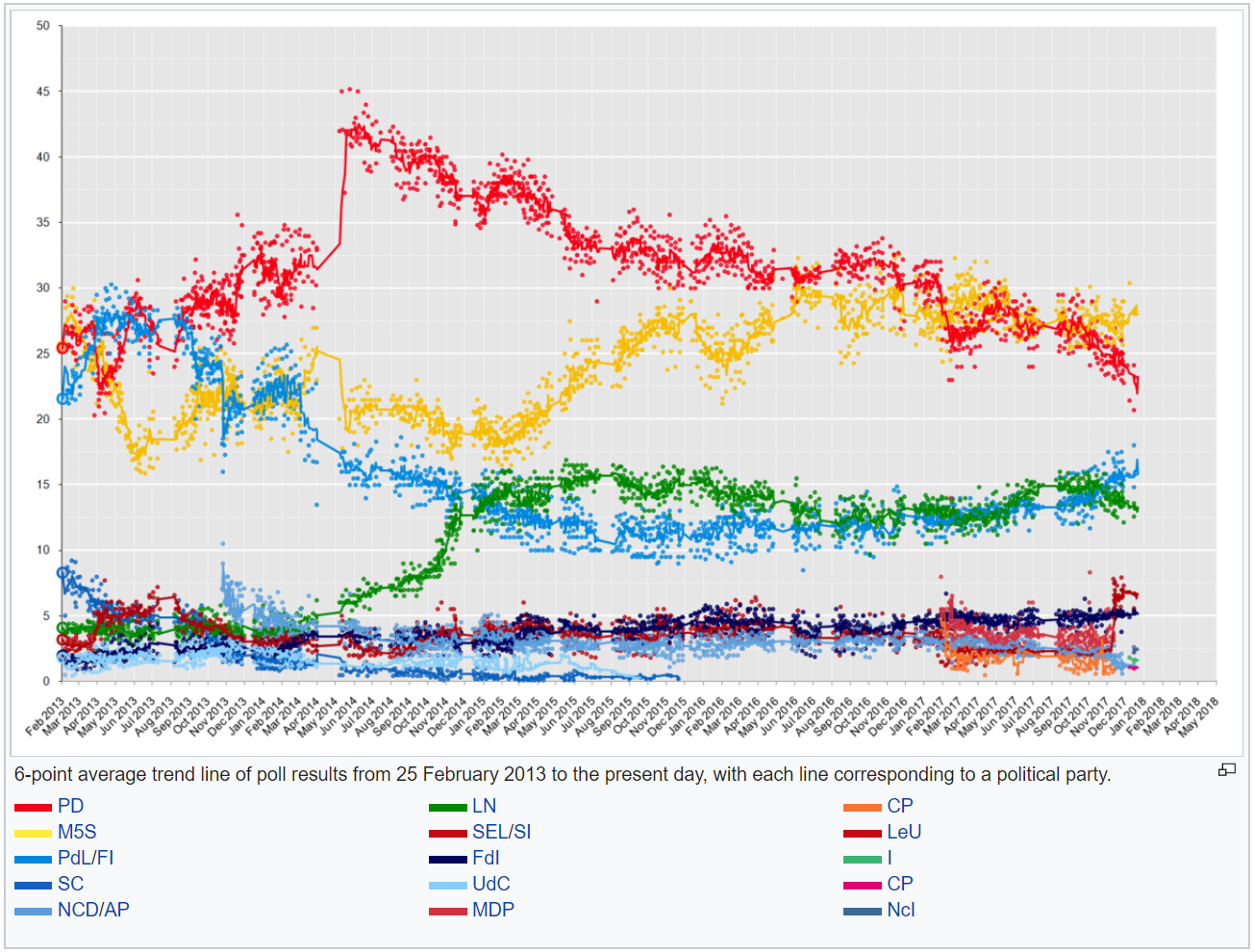

Finally, Italy goes to the polls in March and the anti-EUR MS5 is extending its lead in the polls:

An alternative explanation is that forex markets are already looking through the Trump boom to the bust. The yield curve has been flattening fast in the US and is steeper in Germany though not the overall EZ and rates in the latter are still deeply negative. The prospect for rate differentials still favours the US.

Especially so the more DXY falls.

Rapping up then, EUR strength is taking on the dimensions of some kind of global forex rebalancing rather than just a pain trade but I can’t see it running too much further.

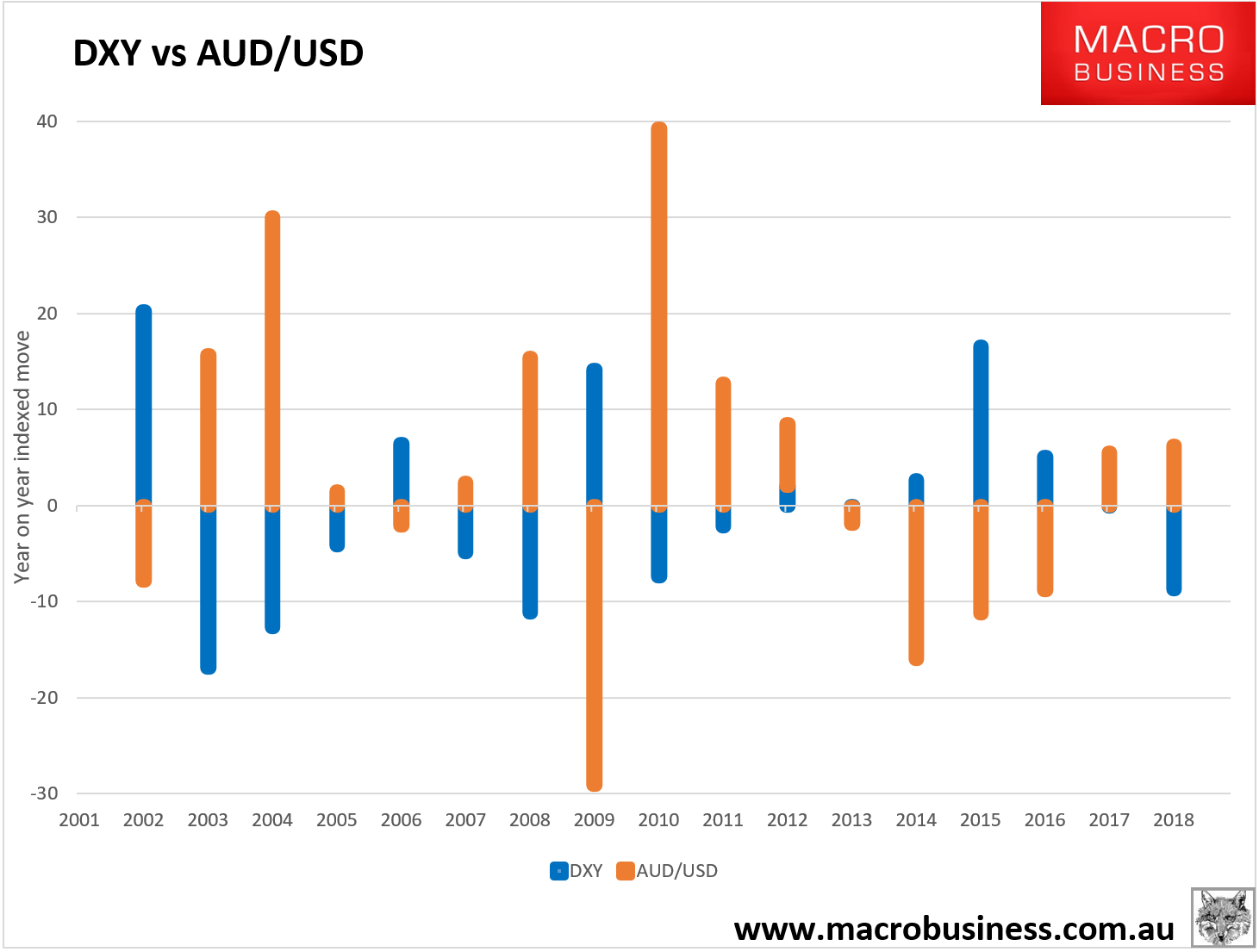

So, how high does the AUD go? If the EUR overshoots to 130 or above then the Aussie could challenge last year’s highs before it sinks again. Aussie dollar fundamentals will keep deteriorating once we pass China Q1 Winter shutdowns. We can see this happening already as DXY weakness outstrips AUD/USD strength:

The last time that DXY was at today’s levels in late September 2017, AUD/USD was 4% higher. As China slows this grind lower in Australian prospects and AUD value should continue.

My best guess is that the EUR is going to push higher yet even though it is massively overbought. I still think the AUD will reverse in due course but it comes with the warning that if we get weather shocks driving bulk commodity prices in the Q1 cyclone season, in this heady environment then the Aussie could also fly to new highs before the Chinese slowing pulls it back down in H2.

Meantime, the falling USD is pouring rocket fuel on US stocks so that international equity gains are waltzing through the AUD headwind in the MB Fund. As we’ll announce in coming days, after a small draw down in December, the international portfolio is up roughly another 2% so far in January while the AUD sits like a circus elephant on the ASX.

—————————————

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that offer superior growth to the crushed local bourse so he is definitely talking his book.

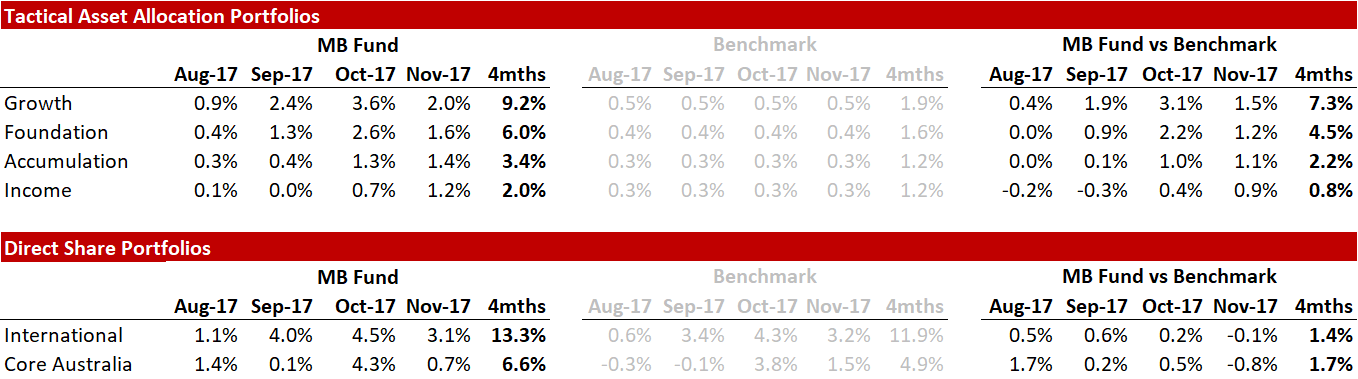

Here’s the recent fund performance:

Source: Linear, Factset

Source: Linear, FactsetThe returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.