The Australian dollar took out its September ’17 peak on Friday night with a new intra-day and closing high:

How much higher will it go? MB’s five drivers model for fair value is:

- global and Australian growth (or, more recently, Chinese growth and Australia’s terms of trade);

- interest rate differentials;

- investor sentiment and technicals; and

- the relative strength of the US dollar.

On the first, after a run of positive data markets have embraced a better outlook for Australian growth in line with accelerating global growth. However, the MB view is unchanged that another year of muddle through is more likely. Household are struggling into the combined headwinds of falling house prices and stagnant wages. Bulk commodity prices are set to fall as China slows despite rising base metals on the falling USD recently. Oil has been strong and will be supportive of the LNG cartel but not Australian income or tax receipts. The only clear growth driver is fiscal spending and it begins to plateau through 2018.

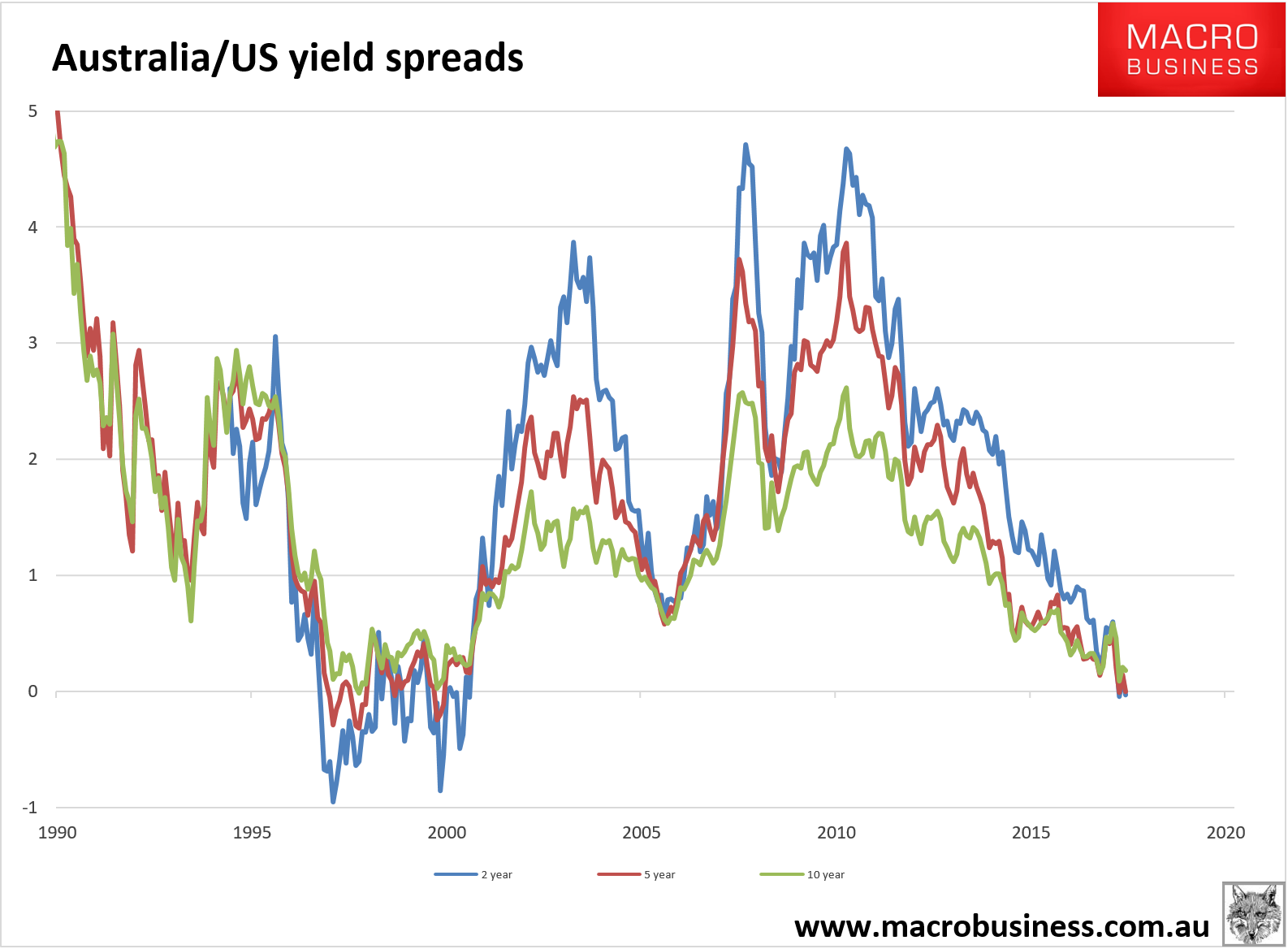

On the second driver, Australian interest rates are slipping inexorably behind those of the US. Cash rates are at parity. For the year ahead, markets are pricing two rates hikes in the US and only one in Australia. But the lower the USD goes the more the Fed will have to tighten with the converse pressures in Australia. We’re going to see at least three US hikes now and, if oil remains high, probably four as shale joins the US activity party. The base case for Australia is none.

Thus the interest rate differential is poised to dive deeply negative in an ongoing trend:

My guess is the gap will widen materially soon. The base case is a -50bps spread by year end but it is easy to envisage wider. The last time spreads were this negative the AUD was sub-50 cents.

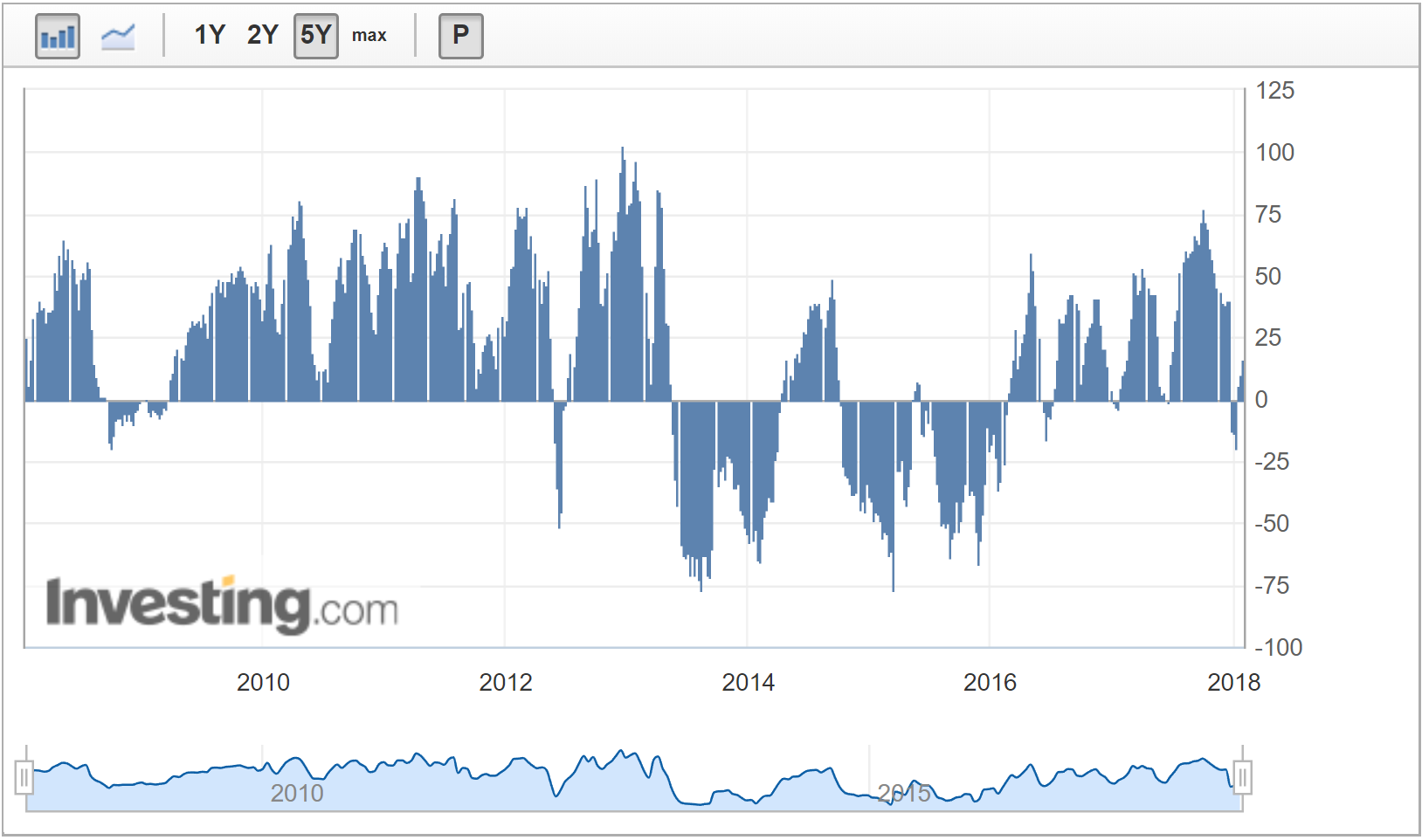

Investor sentiment is mildly bullish according to the CFTC positioning:

That could get much longer if it wanted to. Or much shorter.

Technicals are also bullish with a very neat and broken ascending triangle pattern:

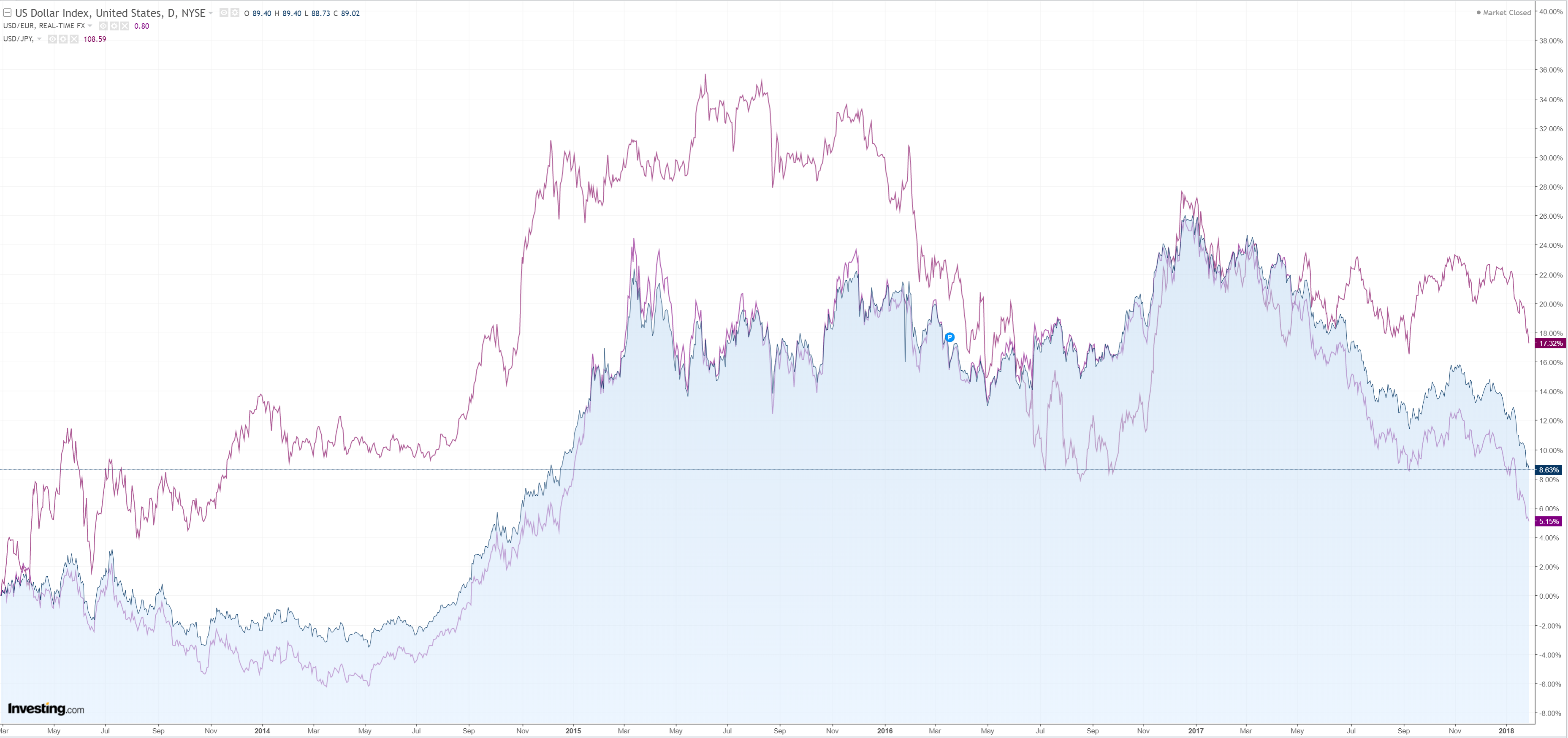

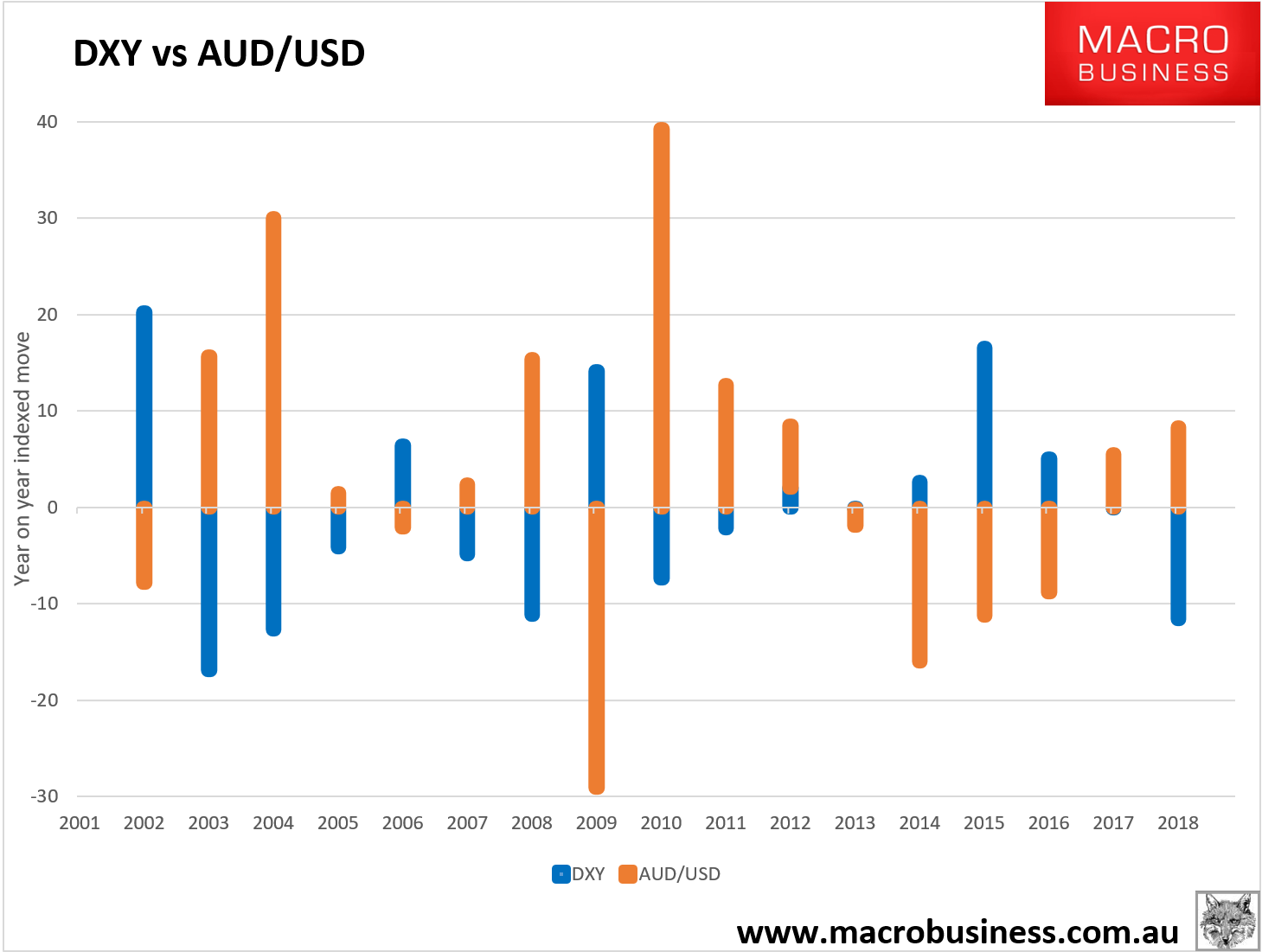

Finally, the key driver of recent times, the relative strength (or weakness) of the USD is very AUD bullish. The Dollar Index (DXY) has been plunging as EUR and JPY rally:

Both Europe and Japan have printed strengthening data over 2017 and markets are beginning to price monetary tightening ahead. But neither is happy about a rising currency. EUR is already at its long term average against USD with a problematic anti-EUR Italian election looming and the Bank of Japan is the master of currency wars. Nonetheless, while these two rise (especially EUR) it will pressure DXY lower and AUD higher.

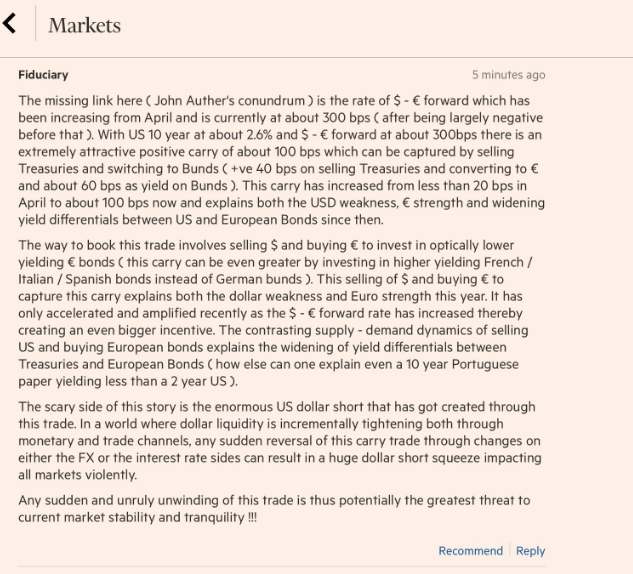

The USD may well fall further yet as the “global synchronised growth” trade continues. But as it does so it sows a boom into the US economy and a forex reversal. There is also this via FT:

These kinds of riskless arbitrages are not the norm. They hint at either a massive investor punt expressing a view on the other side of the trade, corporates wanting to move large amounts of money one way or another or governments hedging out long term forex exposure. The arbitrage will close and momentum in the trade evaporate (accelerated by the FT story!) before long. That will indeed leave the US dollar exposed to a big short squeeze. Though there is no saying when it will come.

In the meantime, there are signs that the AUD is slipping in relative terms. The Dollar Index (DXY) is falling faster than the AUD/USD cross is rising:

This suggests that the AUD is resisting its rise on the still weaker growth case. Expect this to continue as China slows through this year taking down bulk commodities.

In summary, sentiment, technicals and the weak USD for now favour more AUD strength while the underpinning divers of relative growth, the terms of trade and interest rate spreads are still likely to deteriorate as the year progresses (the key risk to this is China letting credit growth re-accelerate). Finally, there is the simple fact that the more the bullish three factors predominate, the more the bearish three come into focus.

Markets do love to offer second chances!

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that will benefit when the Australian dollar falls so he is definitely talking his book.

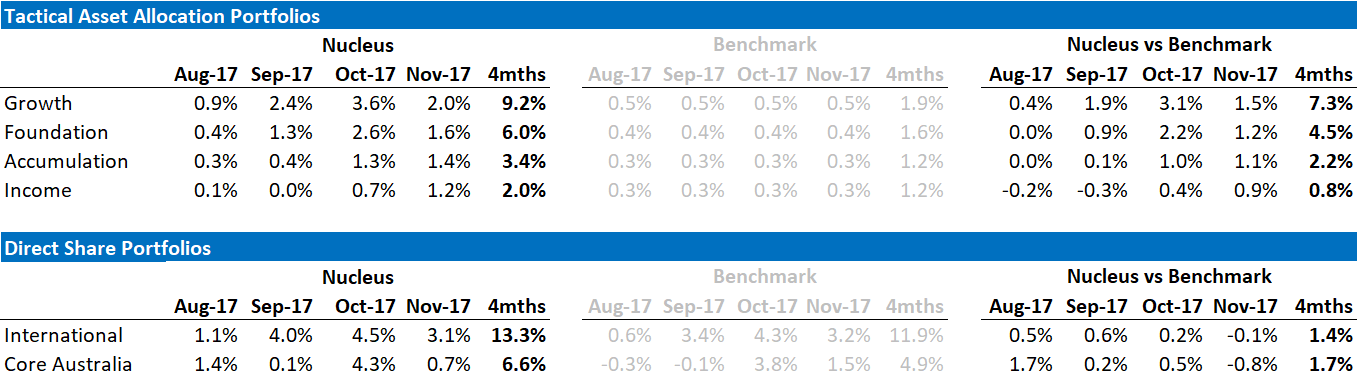

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.