Just weeks after Moody’s warned that Canada’s (as well as Australia’s) housing market (and banks) were at risk, Teranet has reported its results for November, which recorded its third consecutive fall in Canadian home values, let by Canada’s biggest city Toronto:

In November the Teranet–National Bank National Composite House Price Index™ was down 0.5% from the previous month, the third consecutive monthly decline and the largest for a month of November outside of a recession. Indexes were down for four of the 11 metropolitan areas surveyed: Toronto (−1.4%), Hamilton (−1.6%), Ottawa-Gatineau (−0.8%) and Edmonton (−0.7%). Indexes for the two West Coast markets, Vancouver and Victoria, were flat. Indexes were up for Montreal (1.0%), Quebec City (0.9%), Halifax (0.8%), (Calgary 0.7%) and Winnipeg (0.5%). For Toronto it was the fourth straight monthly decline, for a total drop of 7.1%. For Hamilton it was the third straight decline, for Ottawa-Gatineau and Edmonton the second.

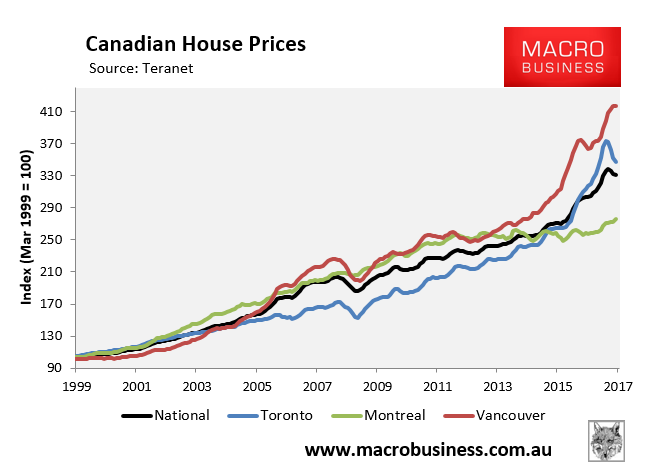

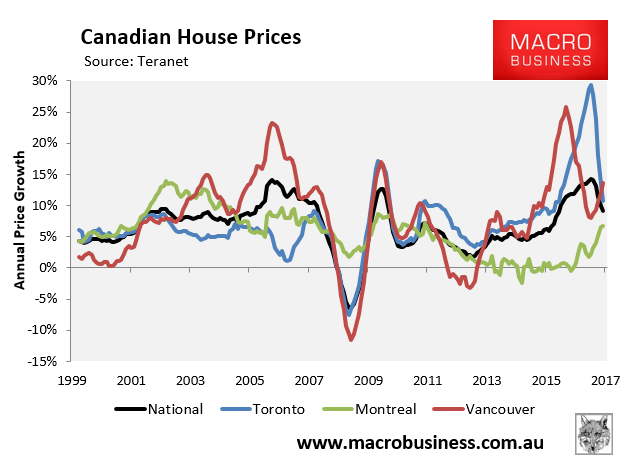

The below charts paint the picture.

First, here’s the house price index nationally and across the major markets:

And here’s the year-on-year changes:

Sydney, Auckland, Toronto. It seems Australia, New Zealand and Canada are all experiencing synchronised housing down turns in their biggest cities.