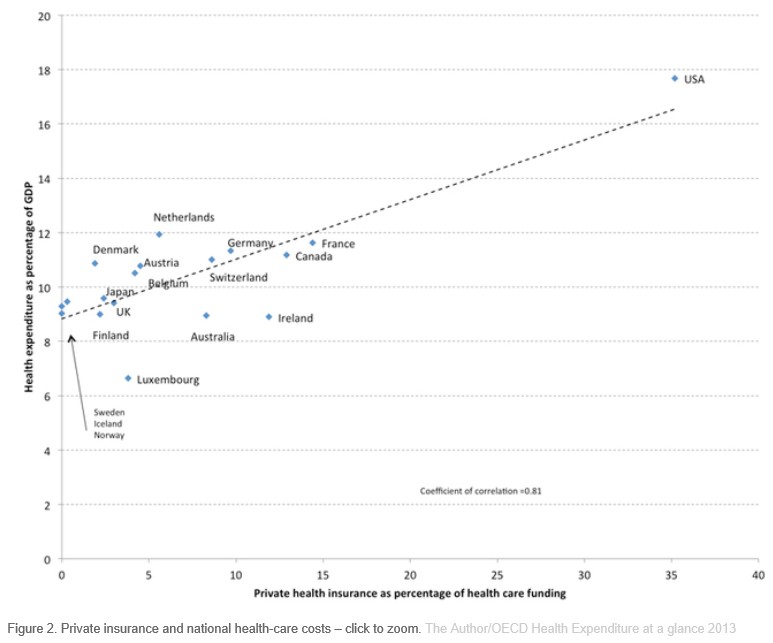

Private health insurance ‘death spiral’ raises tricky questions

I have previously claimed that Australia’s private health insurance system is facing forces similar to the electricity “death spiral”, which arises when demand for power declines, due in part to customers taking up solar, leading to higher prices to cover fixed network costs. That is, the more people that take-up solar power, the faster decline in electricity demand, and the more fixed costs must be spread over a smaller volume of electricity, raising costs for everyone else.

Recently, actuary Jamie Reid claimed that many Australians would soon find it cheaper to pay the Medicare Levy Surcharge than to have private health insurance.

The surcharge is meant to penalise high-income earners who do not have health insurance, but Reid noted that the combination of higher insurance premiums and a reduction in the impact of the health insurance rebate is making paying the surcharge an increasingly attractive alternative. As a result, more people may opt out of health insurance, placing more pressure on the public health system.

In an attempt to avert the ‘death spiral’, the federal government recently announced that young Australians would be targeted with premium discounts in a bid to arrest falling memberships and ensure the overall financial viability of the system.

Today, The Australian reports that the rate of private hospital cover continues to fall ahead of the new measures:

The latest figures from the Australian Prudential Regulation Authority, released yesterday, put hospital cover at 45.8 per cent of the population in the September quarter, down from 46.1 per cent in June. That is the lowest rate of coverage since early 2012, a downward trend blamed largely on the cost of premiums and erosion of the government rebate.

In response, the government is making a second round of cuts to prostheses prices and in March plans to introduce legislation to support discounts for young people, larger excess payments, regional and rural travel and accommodation benefits.

Insurers have already made applications for premium increases to come into effect in April and there has been speculation Mr Hunt wants a weighted industry average of less than four per cent, after the 4.84 per cent increase this year.

Mr Hunt has declined to speculate on an acceptable rate of premium increase but will push insurers to honour their commitment to pass on every dollar of likely savings from the reforms.

Policies have been laden with restrictions and exclusions to lower premiums, leading to an increase in complaints, however there is no available evidence to show that the exodus of members has put further pressure on public hospitals.

Mr Hunt is also calling on State governments to restrict the practice of public hospitals billing patients’ insurers for treatment they are entitled to have without charge, saying has also contributed to high premiums.

The inherent issue with all universal private healthcare systems (including Australia’s) is that they can only remain solvent if enough young and healthy people (the so-called “invincibles”) agree to sign-up. They are the ones who are likely to pay more into the system than they take out. And in the absence of risk-based pricing, the only incentive for the invincibles to sign up is to avoid penalty (i.e. the medicare levy and the lifetime health cover surcharges).

The risk is that healthy invincibles may perceive that it is cheaper to simply pay the penalties than hold private health insurance, which could see an exodus from the system. Thus, the private health system would be left with a larger proportional of unhealthier, older, expensive users of the system, forcing premiums up and leading to a further exodus of the invicibles, and so on.

That said, the overarching question of whether the private health system is worth supporting needs to be examined.

Since 1999 a raft of government initiatives – essentially financial carrots and sticks – have forced Australians into purchasing private health insurance:

Yet, every year, the Australian Competition and Consumer Commission (ACCC) releases its report to the Australian Senate on competition and consumer issues in the private health insurance industry. And every year, the ACCC finds that Australia’s private health insurance industry is characterised by market failures due to asymmetric and imperfect information, as well as significant complexity.

Premiums continue to rise every year, which comes at a direct cost to the federal budget of some $6.5 billion. At the same time, consumers continue to view private health insurance as poor value for money.

Still, successive governments – both Coalition and Labor – fail to articulate why Australians need a duplicate health care system, or why the federal government subsidies to private health insurance should be so substantial.

There is no evidence that private health insurance buys patients extra quality and safety. The Productivity Commission (PC) found that the larger, most comparable public and private hospitals had similar adjusted premature death ratios. Further, the PC found that the team-based care in large public hospitals also leads itself to better coordination of care.

In fact, in Australia’s case, private health insurance is likely raising overall health costs. This is because the high financial overhead of private insurance means that only 84 cents in every dollar collected by private insurers is returned as benefits, with the rest going to administrative costs and corporate profits. By contrast Medicare returns 94 cents in the dollar, even after the cost of tax collection is taken into account.

A single national insurer, like Medicare, also has the monopsony buying power to control prices demanded by powerful service providers.

So, where is the evidence to show that spending taxpayer money to subsidise private health insurance is superior to expanding funding to the public system?

Australia desperately needs to have a national debate about the efficacy of the private health insurance system and whether we should shift towards a single national insurer.