Industry Super has released a discussion paper entitled Assisting Housing Affordability, which examines the drivers of, and solutions to, Australia’s housing affordability crisis.

Below are the key points from the Executive Summary:

The key findings of the paper are as follows:

Australia’s housing afford ability problem has developed over several decades and will require a long-term commitment by all levels of government to resolve.

Destabilising wealth effects and the continuing expansion of household debt are feeding a cycle of property price inflation which looks unsustainable.

Policy responses that increase the buying power of households (for example, through grants, or reduced taxes) will only increase demand, and therefore prices.

Ignoring the emerging crisis in assisted housing (affordable, public and community) now risks major future social and productivity costs.

Simply increasing overall housing stock will not ensure that more assisted housing becomes available. Instead, increasing the supply of assisted housing specifically is required.

Waitlists for social housing remain intractable and this system no longer serves as a safety net.

Achieving the necessary growth in assisted supply is beyond the capacity of Australian governments, and private investment is required.

To resolve the issues in assisted housing, Federal, state and local governments need to coordinate their activity without duplication or political interference. The core elements of any strategy will require:

A central body to provide rigorous housing supply forecasting, which will assist with planning.

Developing appropriate incentives (for example, tax policy) to encourage institutional investment in a new assisted housing asset class.

Expanding the capacity and professionalism of the community housing sector to deal with larger scale developments and tenant administration.

Additionally, some general policy suggestions to address broader housing affordability issues are as follows:

Explicitly linking state and local government planning and housing approvals to estimates of regional housing supply gaps.

Encouraging more work and student visa holders to reside outside of property market hot-spots.

Directing all foreign investment in residential property to new buildings.

Streamlining town planning procedures by mandating the removal of unreasonable height restrictions within urban infill development zones (including ‘inner’ and ‘middle-ring’ suburbs).

Discouraging land hoarding by identifying underutilised assets for redevelopment (including assisted housing), and providing recycling bonuses to incentivise the release of public and private sites.

Reorienting some current tax concessions for existing property towards investment in new housing and institutional investment in new assisted housing.

Reforming land taxes in Australia via the abolition of stamp duties and replacing them with a mix of land and betterment taxes.

Promoting stability around property –the largest asset class held by ordinary Australians.

Unlike many reports of its nature, Industry Super explicitly targets the federal government’s mass immigration program as well as foreign buyers as key causes of the housing problems in Sydney and Melbourne:

Advertisement

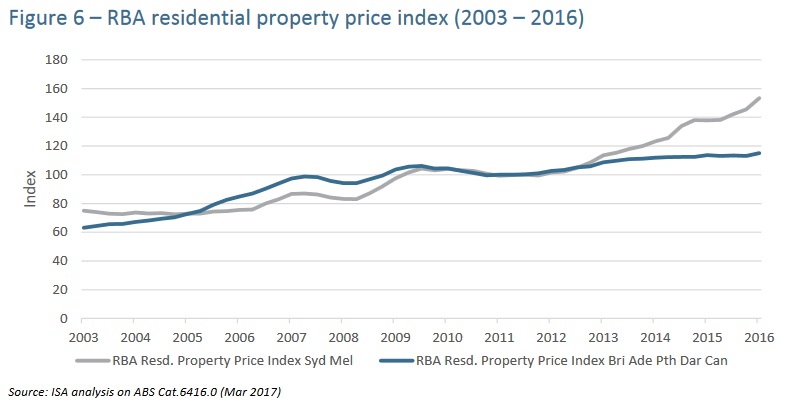

House prices in Sydney and Melbourne have experienced significant growth since 2013 and consecutive years of double-digit growth from 2014 to 2016, with Canberra close behind…

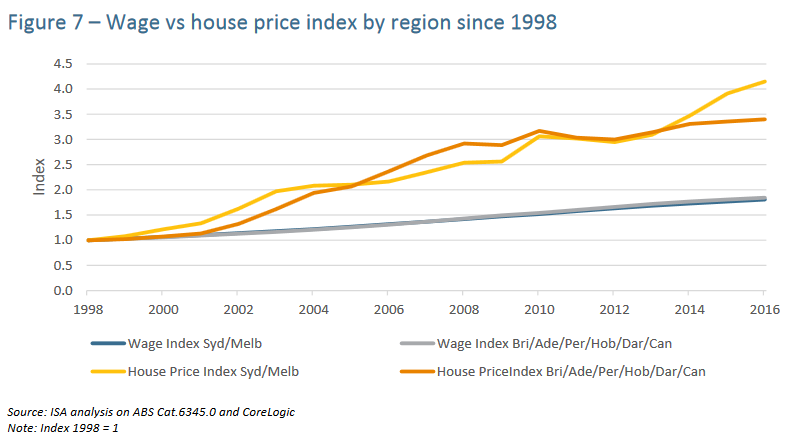

Growth in national average house prices has far outpaced growth in wages over time. This is especially true in suburban Sydney and Melbourne where house prices have experienced double-digit growth since 2013. On the other hand, wage growth has averaged about 2.6 per cent. The greater lack of affordability in Sydney and Melbourne are seen in Figure 7 where price growth in south-east coast capital cities has outstripped the rest of the country since 2013…

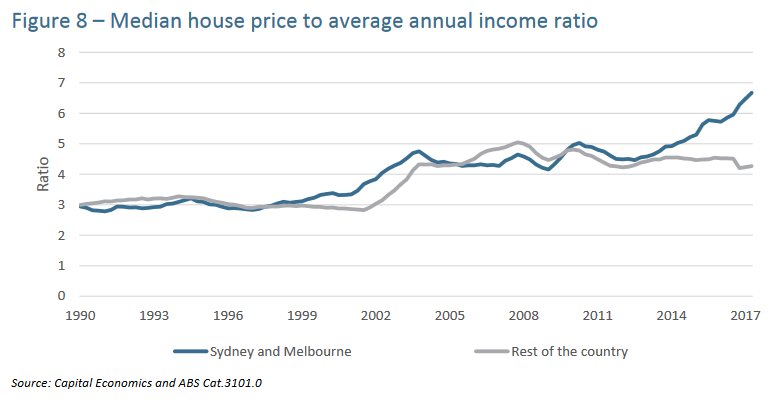

As seen in Figure 8, the house price to income ratio for Sydney and Melbourne on average, now exceeds 6.5 times gross annual personal income. The high ratio is also making home ownership significantly more difficult for low-income earners and young buyers as they need to save a greater share of their income to save for a deposit…

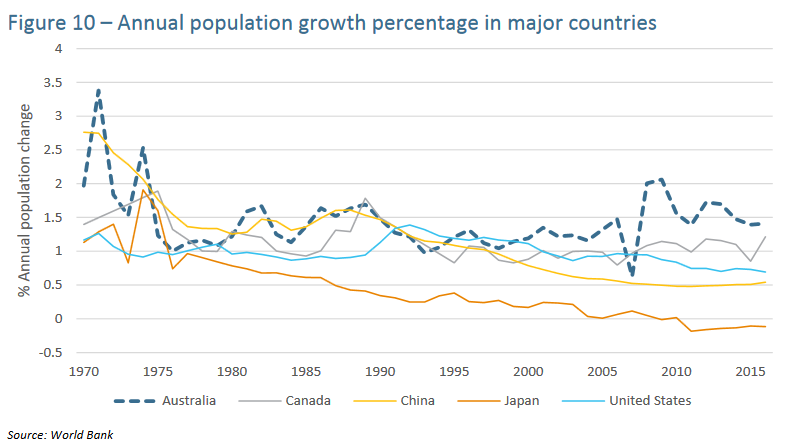

Over recent years Australia’s natural population growth rate and the level of immigration into Australia has far exceeded that of other advanced OECD countries. While a significant immigration program is a big positive for raising living standards over time (via deepening economies of size, access to a skilled workforce, capturing the desire of arrivals for success, adding cultural depth, and offsetting ageing populations) the path to higher population needs to be managed with skill.

A sharp uptick in population growth can send “false” signals of economic success, while driving up asset prices and straining existing capacity. For example, driving up the cost of housing and infrastructure services. All this can focus entrepreneurs on pursuit of “rents” via property development rather than more truly entrepreneurial pursuits such as technology start-ups. The battle for resources also causes competition between the existing and new labour force driving down living standards for low and middle income earners on average. Latest population projections by the Australian Bureau of Statistics (ABS) indicate the Australian population will increase by between 70 per cent and 120 per cent by 2050.

Another potential risk associated with a high population growth strategy is when most arrivals settle in a limited number of regions. This has been true in Australia. New student and work visa card holders have settled in affordability hotspots of suburban Melbourne and Sydney. Around 62 per cent of migrants are now residing in New South Wales or Victoria.

A significant portion of loan activity and sales of existing houses in Sydney and Melbourne have been made to foreigners and tied to education. Nationally, 343,000 student visas were issued in 2016-17.

Latest estimates for the June quarter 2017 from National Australia Bank indicate 17 per cent of new apartment buyers and 11 per cent of new house buyers are foreigners.

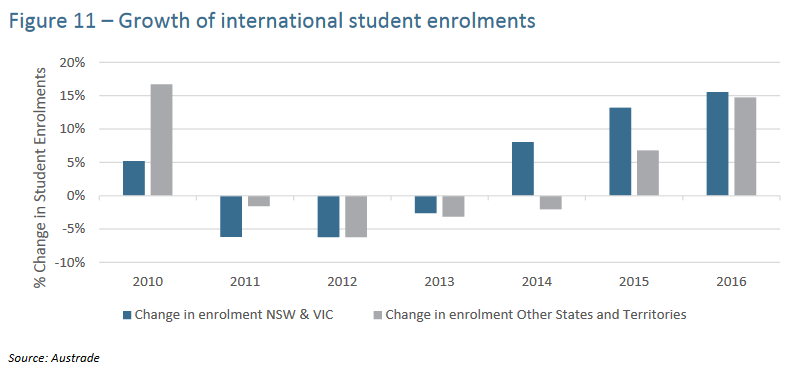

Figure 11 shows that foreign student enrolments have increased since 2013, with enrolments in New South Wales and Victoria accounting for the vast majority.

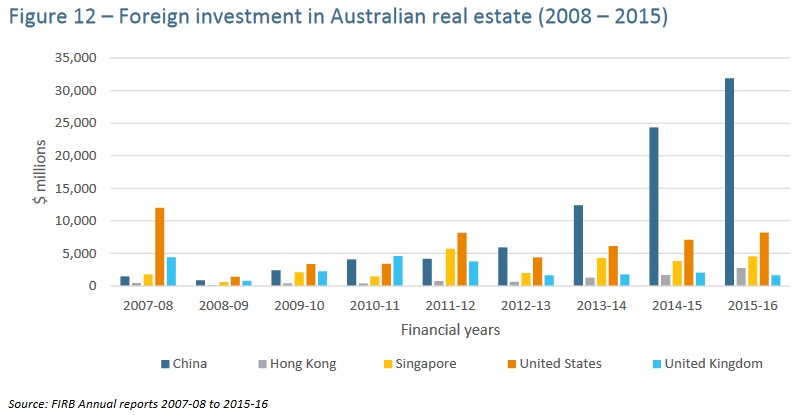

The significant uptick in growth in student numbers has coincided with significant inbound investment by Chinese in Australian real estate dedicated both to new and existing property and the purchase of residential development sites.

Figure 12 shows investment inflows from China rising from around $1 billion in 2008-09 to almost $32 billion in 2015-16 (the latest data point)…

It does seem likely that there was significant rorting by non-residents purchasing existing real estate prior to 2016, with the tacit assistance of real estate agents, mortgage brokers and banks.

Until very recently, non-residents have had a very easy time obtaining funds from Australian or offshore lenders to purchase of both new and existing dwellings in Australia.

The significant uptick in Chinese ‘family’ purchases of established property, funded from offshore, driven by safe haven motives, perhaps explains a significant portion of housing demand near centres of secondary and tertiary education from 2015 perhaps to the first quarter of 2017.

While I strongly disagree with Industry Super’s claim that “a significant immigration program is a big positive for raising living standards over time”, since the empirical evidence is conflicting, the report has done a good job identifying the major issues, especially around the role played by mass immigration and foreign buyers in forcing up housing costs in Sydney and Melbourne.

The report’s solutions are also mostly reasonable; although Industry Super is clearly talking its own book when it calls for government subsidies “to encourage institutional investment in a new assisted housing asset class”. Industry Super also fails to recommend cutting Australia’s immigration intake to the historical average (around 70,000 people per annum) as a solution, instead focusing on the decentralisation pipe dream.

Advertisement

Ultimately, the ‘solution’ to Australia’s housing affordability woes requires policies to both reduce demand and boost supply, including:

Tax reforms like unwinding negative gearing and the CGT discount [reduces speculative demand];

Lower immigration to the historical average [reduces demand];

Tighten rules and enforcement on foreign ownership [reduces foreign demand];

Extend anti-money laundering rules to real estate gatekeepers [reduces foreign demand]; and

Federal Government provide the states with incentive payments to:

undertake land-use and planning reforms [boosts supply];

swap stamp duties for land taxes [boosts effective supply]; and

reform rental tenancy laws to give greater security of tenure [reduces demand for home ownership].

To Industry Super’s credit, it has acknowledged that both demand and supply-side factors have destroyed housing affordability in Sydney and Melbourne, which puts it well ahead of its peers, who typically blame restrictive planning and rigid supply, while completely ignoring the role played by excessive immigration-fueled demand.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.