If we are right in expecting the US Fed funds rate to rise above the official interest rate in Australia next year for the first time since 2001 and for only the third time since the early 1980s, then the Australian dollar could fall from .7700 to .7000 in our view:

Source: Capital Economics

The recent soft retail sales and inflation figures in Australia have led the financial markets to pare back their expectations of how far the Reserve Bank of Australia (RBA) will raise interest rates next year, while the stronger news on activity and more hawkish signals from policymakers in the US have led the markets to price in more interest rate hikes from the Fed.

If we are right in expecting subdued GDP growth and below-target inflation to keep the RBA on hold for all of next year, then rate expectations in Australia may fall further at the same time that they rise in the US.

By June next year, the premium of official interest rates in Australia over those in the US may have been completely wiped out.

We believe the Aussie will take a further leg down as the price of Australia’s main commodity export, iron ore, falls.

We suspect that a more sustained weakening in construction activity in China will cause the iron ore price to fall from $63 a tonne to around $50 a tonne by the end of this year.

RBA’s optimism towards the global economy is justified

we agree that the outlook for business investment and infrastructure spending are all improving

highlighted the strength of the labour market

revised down its forecasts so that the unemployment rate is now expected to “decline gradually” from 5.5%

But the RBA is too optimistic on consumption and inflation

It noted that “one uncertainty is the outlook for household consumption” and that underlying inflation “is likely to remain low for some time”. But we don’t think it went far enough given the further slump in retail sales growth in September

the surge in jobs growth has not offset the downward pressure on household income from record low wage growth, rapidly rising utility prices and the burden of high debt

And the new spending weights that the ABS will use to calculate CPI inflation from the fourth quarter make the

RBA’s forecast that underlying inflation will rise above 2.0% next year even more challenging

it’s significant if it means that underlying inflation stays below the 2-3% target range until 2020 as we expect

We don’t think conditions will warrant higher interest rates until late in 2019

Of course, the RBA is willing to accept low inflation if it helps reduce the threat to the financial system from high household debt and housing

That’s why further rate cuts are unlikely

But equally, the comments that “credit standards have been tightened in a way that has reduced the risk profile of borrowers” and that “housing conditions have eased further in Sydney” mean that the need to raise rates to take heat out of housing has diminished

And high debt means the RBA is concerned that raising rates would push some households over the edge

Overall, subdued GDP growth and below-target inflation will probably mean the RBA bucks the recent global trend of a shift towards tighter policy

This divergence in monetary policy could contribute to the Australian dollar weakening from US$0.77 now to around US$0.70 next year.

Down, down, currency is down.

—————————————–

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities so he is definitely talking his book. The MB Fund offers one way to profit from a falling dollar:

Source: Linear, Factset

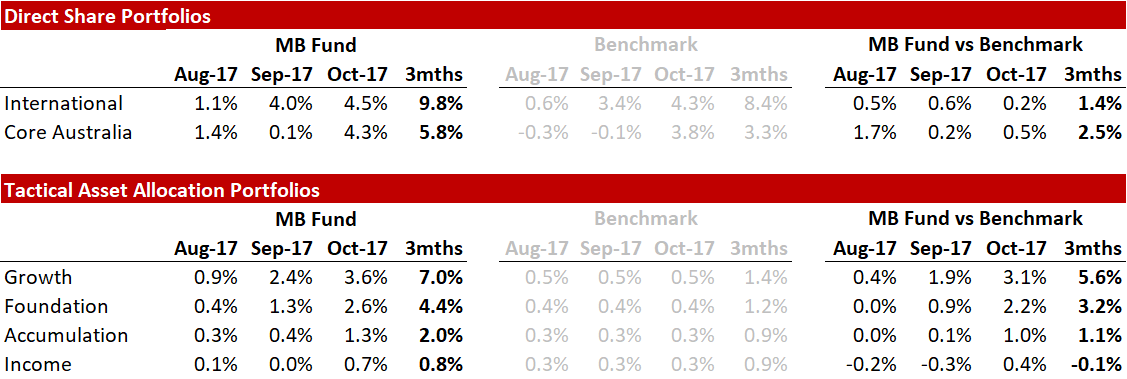

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If these themes and the fund interest you then register below and we’ll be in touch: The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Source: Capital Economics