CBA is the great AUD bull:

While we see further near-term downside in AUD/USD, and believe AUD/USD could decline and test the technical support around 0.7473, we are not yet getting bearish AUD. and we don’t believe it is headed significantly lower for five main reasons:

- Australia’s terms of trade is 54% higher today than it was in March 2001

- The world economy is accelerating with broad-based growth of around 3.4%, rather than decelerating as it was in 2001, as the global effects of the dot corn U.S. recession persisted, generating downward revisions to global GDP growth, and lowering commodity prices

- Asia’s economy is not recovering from the 1997-98 Asia crisis as well as running a regional current account deficit, like it was in 2001. And the widely-observed index of Asian currencies (ADXY index) is today 15% higher today compared to 2001. Furthermore, Asia’s regional economy is currently running a current account surplus

- Australia’s current account deficit is today relatively small at only 2.1% of GDP, as opposed to an average of 4.3% over the two-years leading up to March 2001. Which means AUD/USD is somewhat less sensitive to interest rate differentials, and AUD retains a higher valuation than in 2001

- Australia’s economy is growing well, and on-track to expand at around 3.0% over the next year, with the unemployment rate remaining on a downward trend. Later today, we get an update of the Australian labour market with the release of the October numbers.

We see downside risks to our recently-released currency forecasts as the USD retains strength on the prospect of a cut in the U.S. corporate tax rate passing Congress before year-end, upside U.S. inflation pressures that may cause the Fed to lift interest rates more than the market is currently anticipating. At the same time. lower than expected Australian wage growth risks generating lower-for-longer Australian inflation, and delaying the RBA from raising interest rates well into 2019. Furthermore, the current financial market indicators of a flattening U.S. yield curve and downturn in high yield credit spreads are generating some nervousness in global equity markets, and are likely to weigh on AUD/USD in the near-term. AUD/USD remains vulnerable to more near-term downside.

CBA recently said we are going to 85 cents. And that the high AUD was structural.

It’s five points today are no better:

- Yeh, today, but not tomorrow as China slows. New terms of trade lows are coming in 2018.

- Yeh, today, but not tomorrow as China slows and Fed tightening eventually slows the US as well, later next year or 2019.

- Fair enough but EM forex will get caned as China slows, CAS or not.

- True, but the CAD was above 5% before the 2016/17 terms of trade bounce. And it’ll be back there as it falls.

- Blah. 3% my butt. 2.5% at best with risks to the downside for 2018 as housing stalls and falls and takes the consumer to the woodshed.

CBA was wrong before. It’s still wrong. Except on near term downside!

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities so he is definitely talking his book.

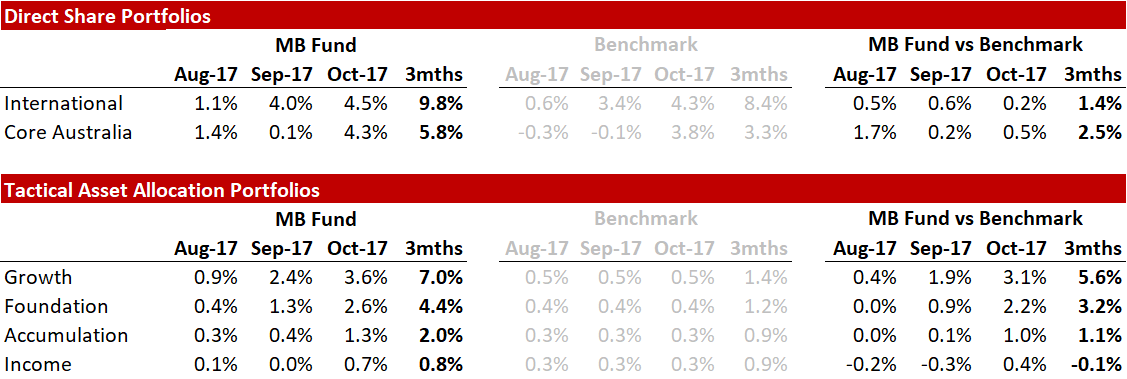

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If these themes and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.