The Business Council of Australia (BCA) and the Turnbull Government continue to argue that Australia’s company tax rate is among the highest in the world and that if we don’t reduce it then Australia will be left behind economically.

“We are kidding ourselves if we think we can impose one of the highest tax rates in the developed world on Australian businesses and expect them to thrive, invest and create jobs”…

“As other countries have slashed their company tax rates to improve their competitiveness, Australia has been left to languish with a rate that has been unchanged for 16 years”…

Advertisement

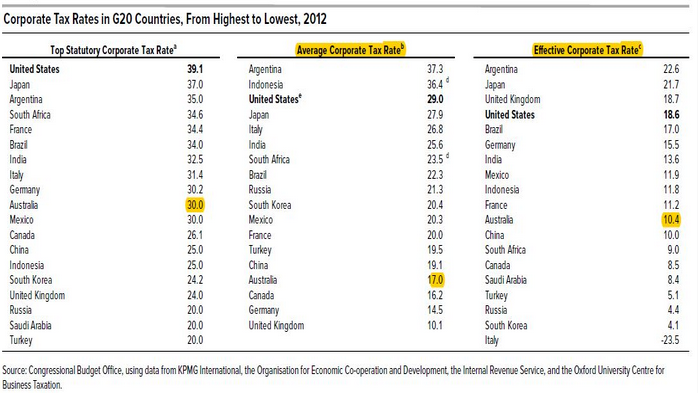

The ABC’s Business Editor, Ian Verrender, has challenged this view, citing analysis from the US Government’s Congressional Budget Office, which shows that Australia’s company tax rate isn’t particularly high after all:

If you believe the spin from some quarters, Australia charges like a wounded bull when it comes to corporate tax.

What it reveals is that Australia is either the global Goldilocks of corporate tax (not too hot, not too cold) or extraordinarily generous to big business, depending on how you measure it.

While the study is current, the numbers have changed in recent years. Both Japan and Germany have lowered their top-line taxes to around the same level as ours…

It may get all the headlines, and it will be the only measure batted out in Parliament this week, but the top-line tax rate is just one way of measuring corporate tax rates.

Because of various tax concessions or imposts in different countries, the average tax rate is often a better measure.

And for companies considering investment decisions, the best way to measure corporate tax is through comparing what’s known as effective tax rates…

Our average corporate tax rate, however, is just 17 per cent, and when it comes to effective corporate taxes, companies in Australia pay just 10.4 per cent.

The discrepancy relates to a range of things, including how quickly firms can write down or depreciate the value of their investments or where they have sourced their finance.

Verrender also notes, as MB has done, that the primary beneficiaries of any company tax cut are likely to be foreign owners/shareholders:

Advertisement

We have a unique — OK, New Zealand has it too — system of corporate tax that drastically lowers the amount of tax Australian investors pay.

It’s known as dividend imputation and it effectively lowers the company tax rate for local investors to almost zero…

For that reason, the benefits of any cut to the Australian corporate tax rate overwhelmingly will flow through to foreigners.

For Australians, it has almost no effect because cutting the company tax rate reduces the amount of franking credits they receive…

Verrender also argues that cutting Australia’s company tax rate would have minimal impact on spurring economic growth:

The theory… goes something like this: Less tax equals greater profits. And bigger profits means more money to invest, which should boost employment and help lift wages.

The trouble with theories is that they tend to not work as envisaged in the real world. And what we’ve seen in the past decade — with global interest rates cut to zero – doesn’t quite fit the model.

The idea behind those rate cuts, to zero and even into negative territory, was that corporations would borrow and invest, boost wages, fuel inflation and pick the global economy up off the mat.

Instead, most of the benefits of the tax cuts were passed directly onto shareholders who demanded bigger dividends in a world where there was no return on cash.

The investment dollars went into assets, such as shares and property, rather than production, as asset bubbles ballooned around the globe.

It’s highly likely the same thing will happen when corporate taxes are cut — the benefits will be distributed to shareholders rather than reinvested.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.