Interesting stuff as the Real Estate Treasurer continues his bubble-defence world tour:

When Treasurer Scott Morrison met Goldman Sachs chief executive Lloyd Blankfein in New York late last week, the Wall Street banker was baffled.

Blankfein was searching for answers. Why, at a time when most economies were generally performing reasonably, had politics become so difficult in many countries?

“He does find that perplexing because their view is [economic] things are a lot better than the politics reflect,” Morrison told The Australian Financial Review in Washington on Friday.

“I made this point: so long as we’ve got wages growth in the space it’s in then it’s understandable that we’ll continue to have those political frustrations.”

…”I’ve better talking about better days ahead in the budget and beyond, and I think there’s a very similar sentiment among the finance ministers and central bank governors,” Morrison said.

“In the many one-on-one discussions I’ve had with everybody from Fed board members [Yellen and Dudley] to other finance ministers it’s been a pretty consistent trend.”

“That’s only going to change through greater investment and improved productivity,” Morrison said.

“It’s the coupling of cutting business taxes and lifting investment in infrastructure in a low rate environment, and using the government’s balance sheet to achieve that,” Morrison said.

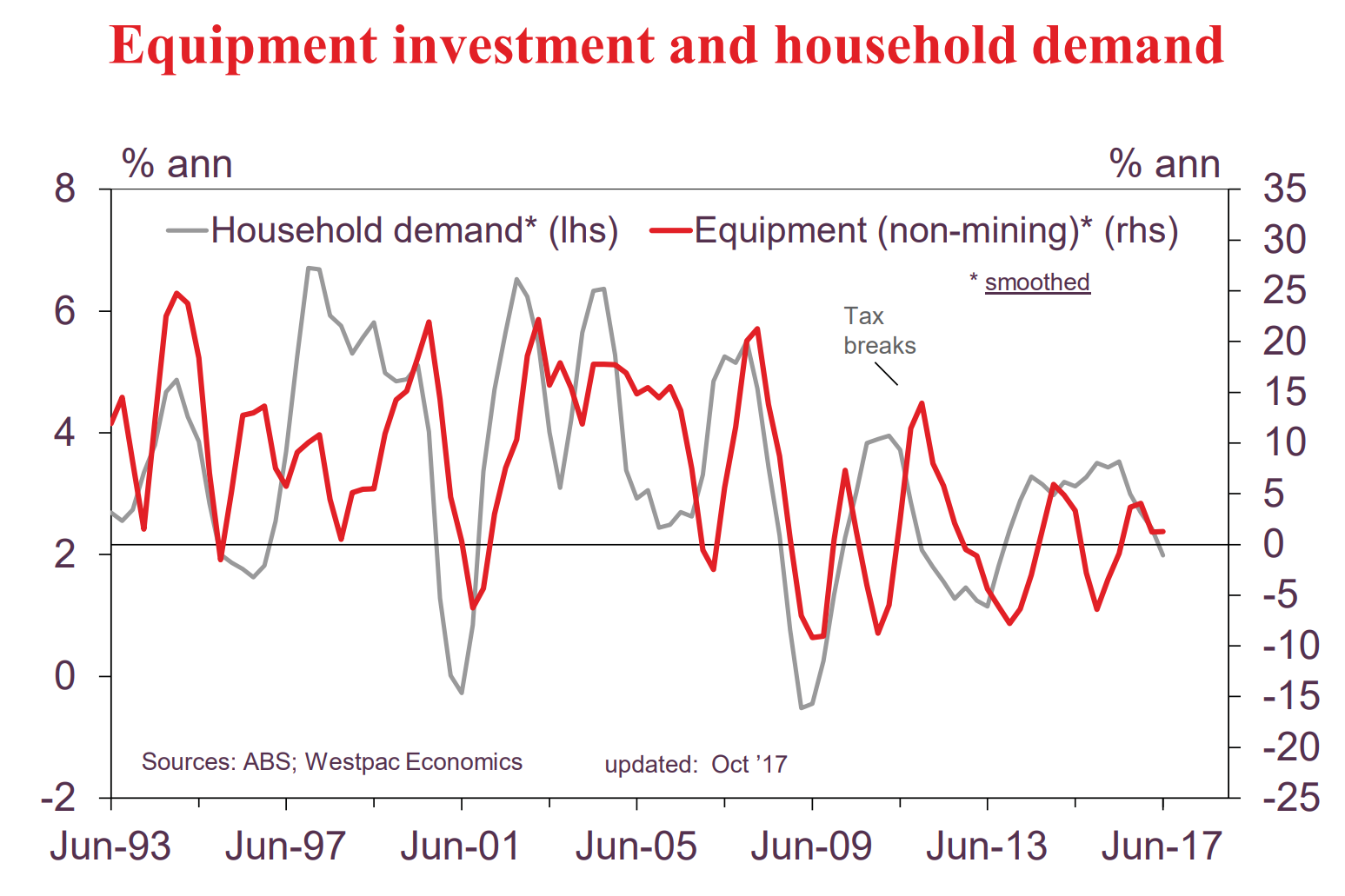

There are a few productivity hopefuls on the horizon. A little bit of business investment and infrastructure will help but it’s nearly all in building not equipment and the infrastructure is mostly crush-loaded before it even arrives so I wouldn’t be getting my hopes up:

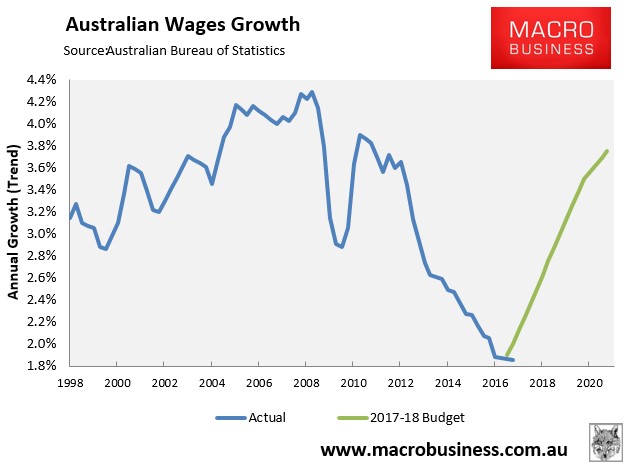

As for a wages rebound, we all know what the Realty Treasurer is hoping for:

It would be amusing if the sovereign rating did not hang on it!

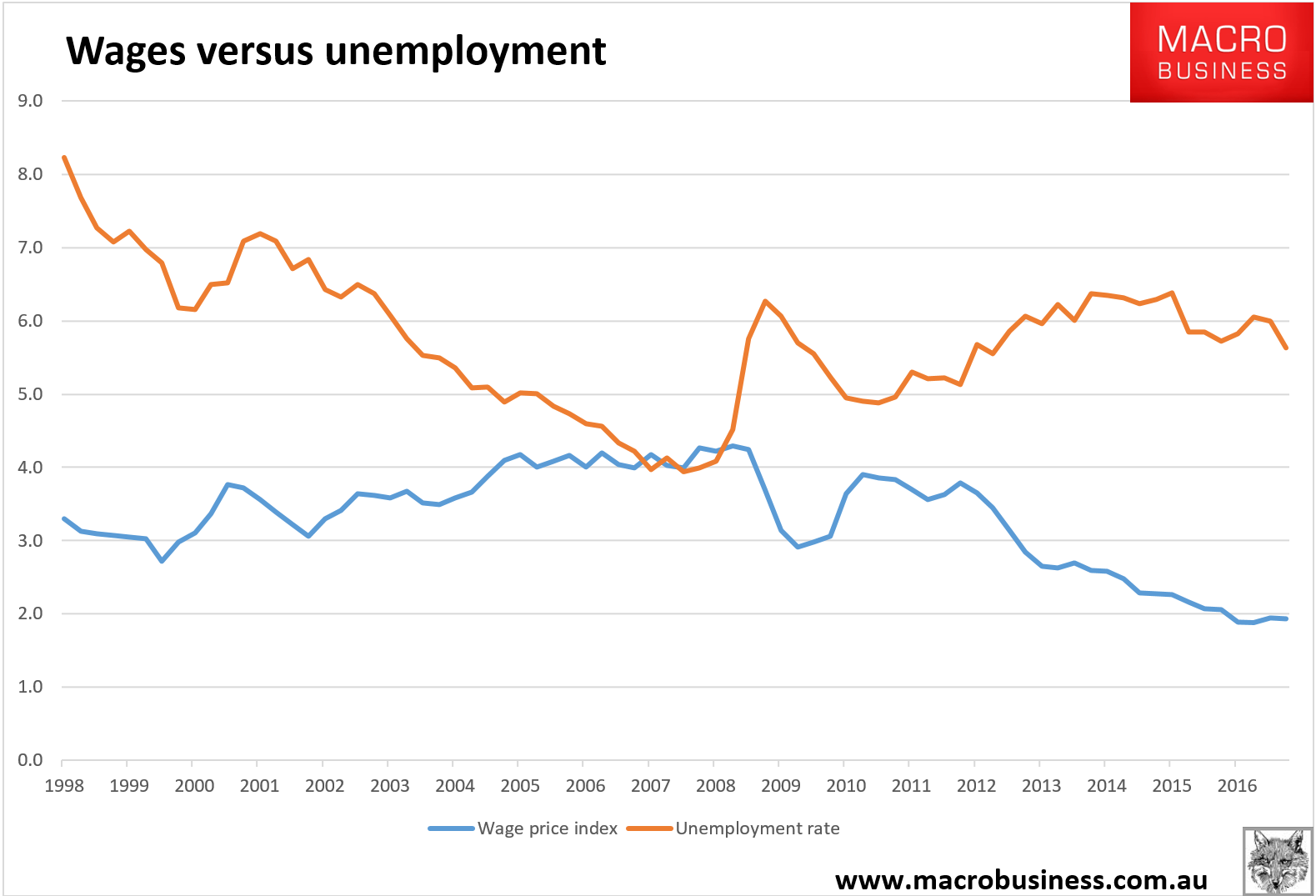

And, frankly, there’s not a lot of understanding about the labour market coming from the Realty Treasurer. Unemployment has already fallen to levels that should see wage growth. It ain’t that:

The last time unemployment was at 5.6% the wages index was at 3%. Today it is 1.9%.

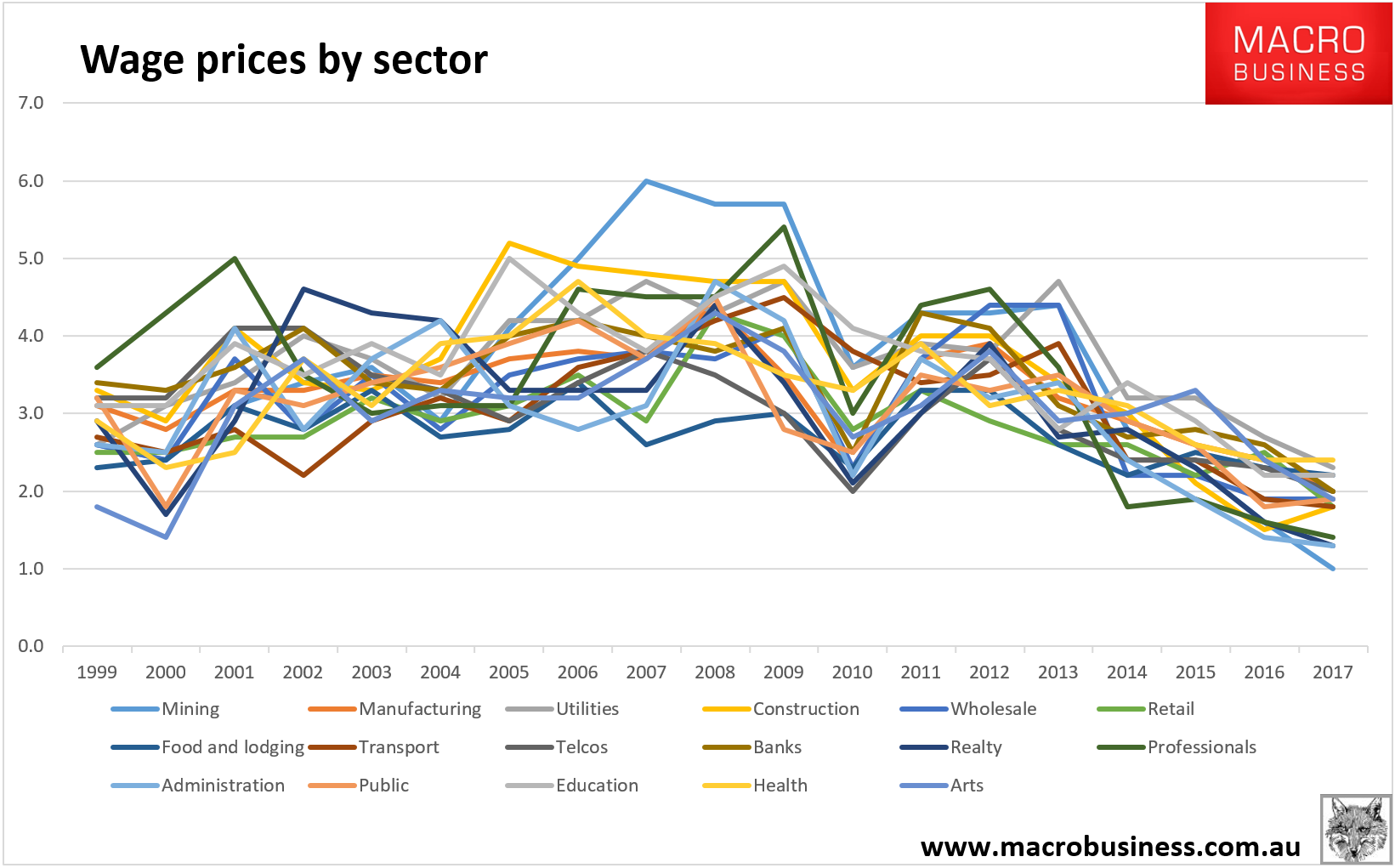

Just as interesting, the great wages deflation is universal:

Mining has led the decline but it is in every single sector including such booms as health, education and the public sector. It is actually even worse than this because there is also large sectoral rotation from high paying jobs such as mining to low paid such as barristing.

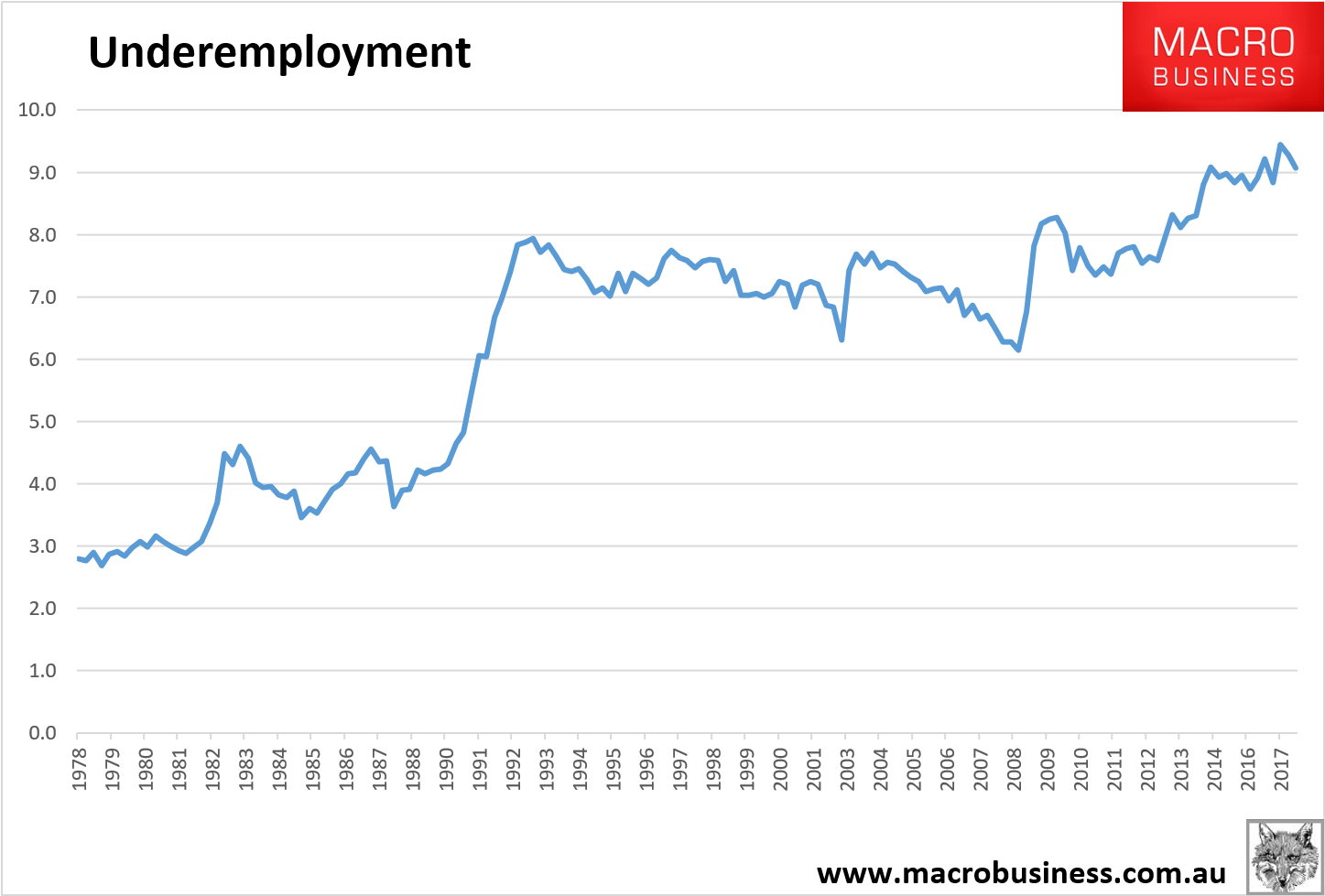

This reeks of labour market oversupply. And, as we know, there is an abundance of it once we look past the headline number. Underemployment is rife:

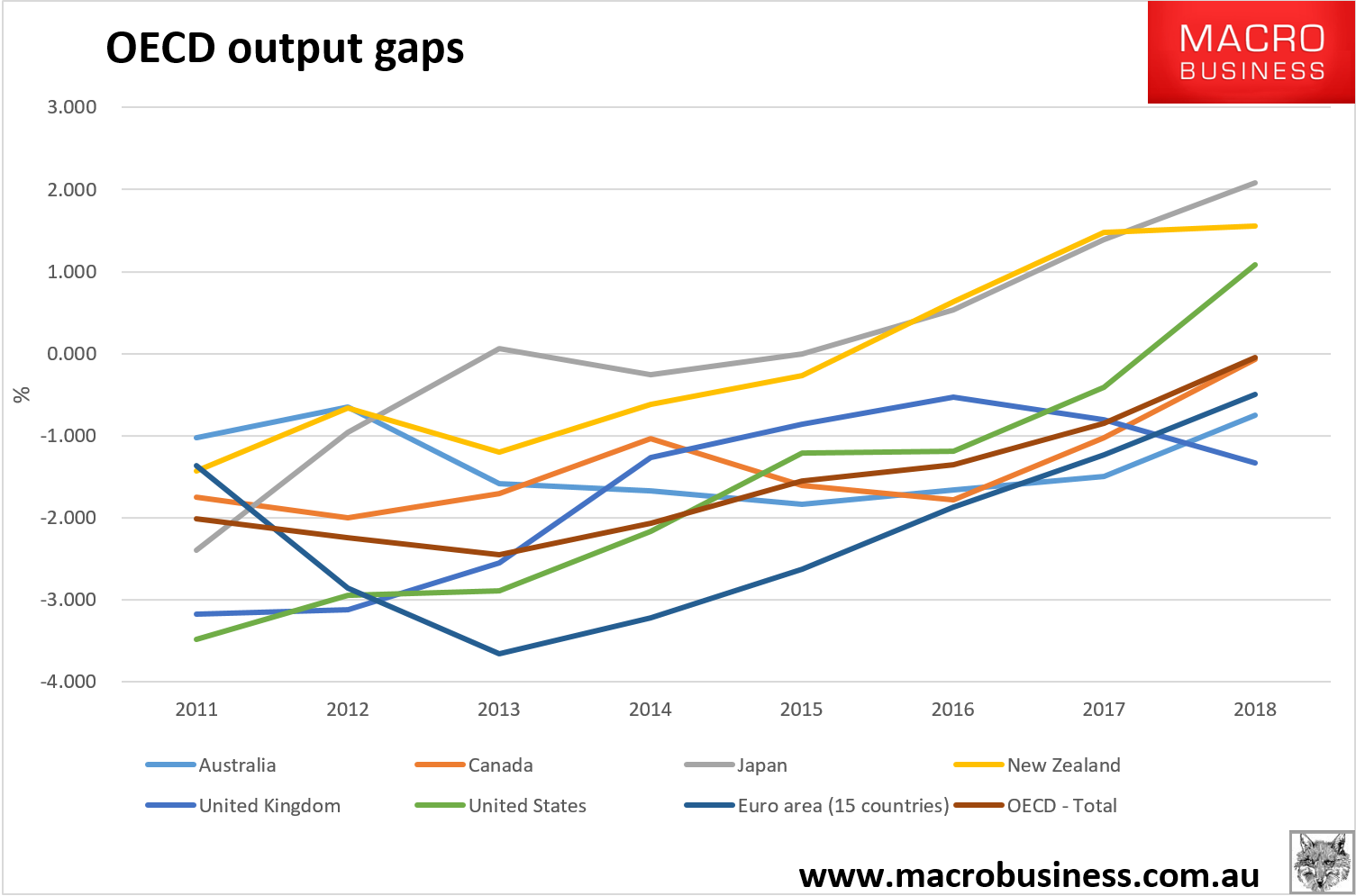

And it all appears very nicely in the OECD measures of output gaps, in which Australia’s is the largest:

Good luck with that forecast closure next year!

What we have here is structural change. The Australian economy is brimming with labour market slack as we rotate from full time to part time jobs, from high paying tradable jobs to lower paid menial roles and from a regulated and closed industrial relations system to an open and flexible market exposed to global inflows.

As a backdrop to this we can add that this was all very predictable. As the terms of trade crash that ended the mining boom works its way through the economy, wages were always going to have to adjust to lower growth. The nation is in the process of taking a massive pay cut for the same amount of work so slack was bound to expand.

We can add that we’re also going through a second and so far roundly ignored structural adjustment: reductions in the pace of growth of household debt which is about to turn much slower again, so more slack is guaranteed.

The question is, how does one best manage these structural adjustments? Both booms leave your economy very inflated and its cost structure uncompetitive. So the way to fix it is to engineer a real exchange adjustment so that you can once again grow the export and import competing businesses which comprise 40% of the economy.

To do that you do is this:

- explain it the people so that the burden of adjustment can be shared appropriately to stabilise the political economy;

- support the vulnerable;

- boost productivity reform so that as much of the adjustment as possible can be absorbed by efficiency gains;

- contain asset prices to improve competitiveness;

- contain other input prices like energy;

- pursue weak dollar policies to ensure that as much of the deflation is absorbed externally as possible;

- use fiscal stimulus to absorb labour market slack as the private sector deflates and deleverages, and

- ensure industrial relations fairness so that capital doesn’t force the entire adjustment onto labour.

What have we done?

- raised expectations with parlour tricks and cheap excuses that of course failed, destabilsing the political economy and throwing out multiple governments;

- blamed the vulnerable;

- zero productivity reform;

- deliberately juiced asset prices with failed credit containment and mass immigration;

- blown energy prices sky high;

- pursued strong dollar policies at every quarter;

- deployed fiscal austerity (until recently);

- trashed the industrial relations structure via mass visa rorting.

In fact, pretty much the only input cost in the economy that we’ve let deflate is wages and by doing so have launched a massive class war on labour to take the full brunt of the structural adjustments emanating from the end of the mining and household credit booms.

But then that’s all to the good. We all know what he’s really doing over there in New York, don’t we? The Real Estate Treasurer is following a well-trodden path, sticking his head in the optimist’s noose to support confidence in lending to Aussie banks for mortgages at home, rather than addressing the failing structure of the economy.