Domainfax’s Peter Martin and Michael Koziol have penned a misleading article claiming, entitled “An inconvenient truth: you’re paying less for your mortgage now than a decade ago”, that tries to argue that housing affordability for those wishing to own their home (as opposed to renting) has improved, according to the ABS’ biennial Housing Occupancy and Costs survey for 2015-16, which was released Friday:

Record-low mortgage rates have made it easier to meet the payments on home loans than it has been in decades, despite record-high house prices, new figures show.

Confounding talk of unaffordability, the Bureau of Statistics calculations show that as recently as 2005-06 it took an average household 19 per cent of its gross income to meet ongoing housing costs. By 2015-16, it had fallen to 16 per cent, the least in records going more than 20 years.

The average mortgaged household now spends less of its income on housing than it does on food, a turnaround from earlier surveys in which it spent more. Housing costs include mortgage payments and water and rate payments.

Adjusted for inflation, the average mortgaged household paid $434 per week in 2015-16, much the same as in 2005-06. But over the same period the average income of mortgaged households climbed from $2272 per week to $2759…

Among home-owning households the proportion that have paid off their mortgages has fallen dramatically, from 42.8 per cent of all households to 31.4 per cent.

The phrase ‘composition bias’ comes to mind when examining this data.

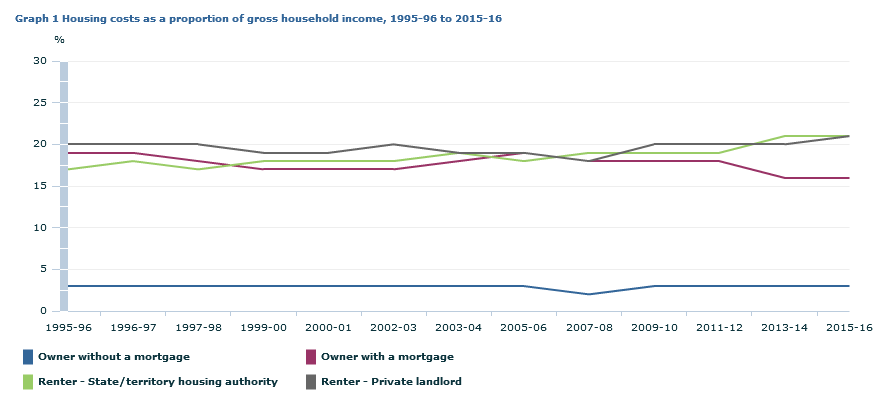

While it is true that housing costs for mortgage holders has declined over the past 20 years – from 19% of income in 1995-96 to 16% of income in 2016-16:

This is misleading as an affordability metric as it does not take into account the huge shift in the composition of mortgage holders from young to old.

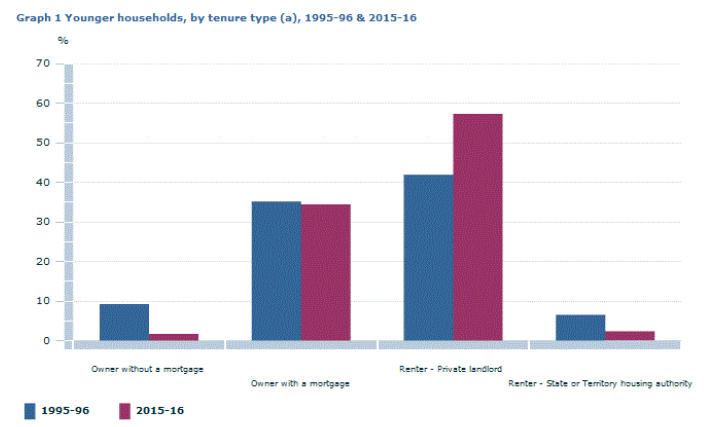

As shown in the next chart from the ABS, the overall home ownership rate has collapsed for households aged under 35, whereas as the share of younger households with a mortgage has also declined from 35.1% in 1995-96 to 34.4% in 2015-16:

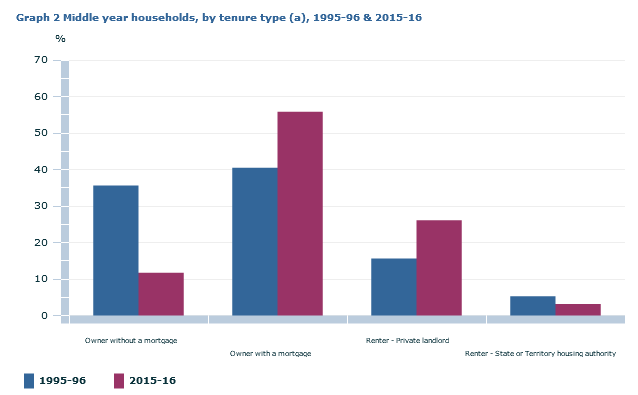

By contrast, the share of households aged 35 to 54 with a mortgage has surged from 40.5% in 1995-96 to 55.8% in 2015-16:

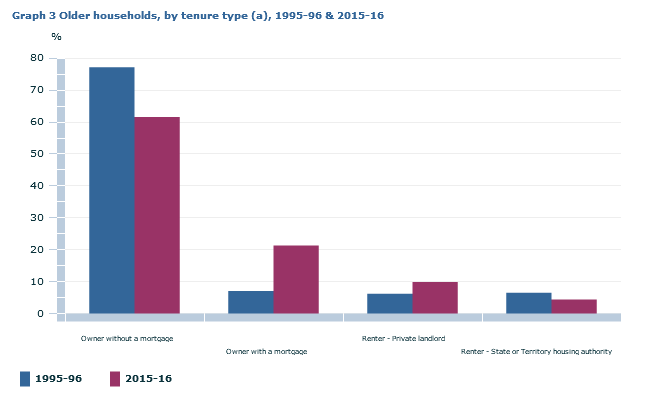

Whereas the share of households aged over 55 with a mortgage has surged from 7.1% in 1995-96 to 21.3% in 2015-16:

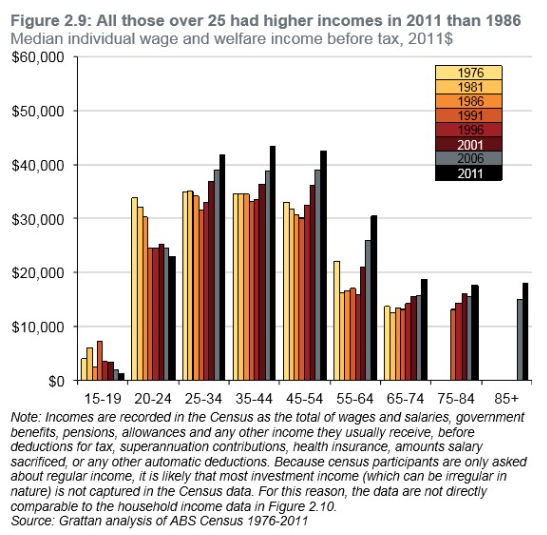

We know that incomes of older generations have risen far more quickly than for younger generations:

Therefore, rather than home ownership affordability improving over the past 20 years, it’s more a case of younger households being locked-out of Australia’s housing market and those holding the mortgages shifting to older cohorts whose incomes have surged.

Peter Martin and Co have also conveniently ignored that it takes much longer nowadays to pay off a mortgage, which is curious given Martin noted this exact phenomenon last year:

You might be thinking that low wage rises aren’t a problem so long as prices are increasing by less. But that ignores a little-recognised phenomena known as “mortgage tilt”.

When you take out a mortgage in a world of high inflation, your payments are “front-end loaded”…

In a world of low inflation the “tilt” becomes much less severe. If repayments consume a large proportion of your wage at the start, they’ll keep doing it for decades…

To the extent that “tilt” is one of the reasons, deeper cuts in interest rates won’t much help.

We’ve a problem, one born of success. Low inflation looks good, until you’re in it.

In any event, when we talk about ‘housing affordability’, we are generally talking about the ability of first home buyers to enter the housing market and pay-off their homes. Their situation has unambiguously gotten worse, as evident by:

- The collapse in home ownership among under 35s;

- The huge deposit required to obtain a mortgage;

- The big rise in the ‘bank of mum & dad’; and

- The casualisation of the work force, rising labour underutilisation, and record low wages growth.

Domainfax: Property always.