Jess Irvine wants a home but you can go to Hell

It’s a truly ridiculous editorial tightrope that Jess Irvine has decided to walk. Recently she declared:

Somewhere deep inside me, a switch has flicked.

I feel different; changed somehow.

I never thought it would happen to me.

And, diary, I’m embarrassed by this new feeling. But I’m ready to confess.

First, a little background. As you know, I’ve been writing about the economy and the property market for well over a decade now.

I’ve interviewed property spruikers and property naysayers alike. I’ve always been acutely conscious I draw a salary from a business whose revenues are quite reliant on a buoyant property market.

So, perhaps from some deep contrarian journalistic impulse, I have always felt compelled to reject the Australian obsession with home ownership and point out the virtues of renting, such as the freedom from crippling debt and the flexibility to move.

But, dear diary, that greatest of Australian dreams has finally come to visit me in my slumber.

So here it is, an embarrassing confession from a long-time advocate of renting: I want to own a home.

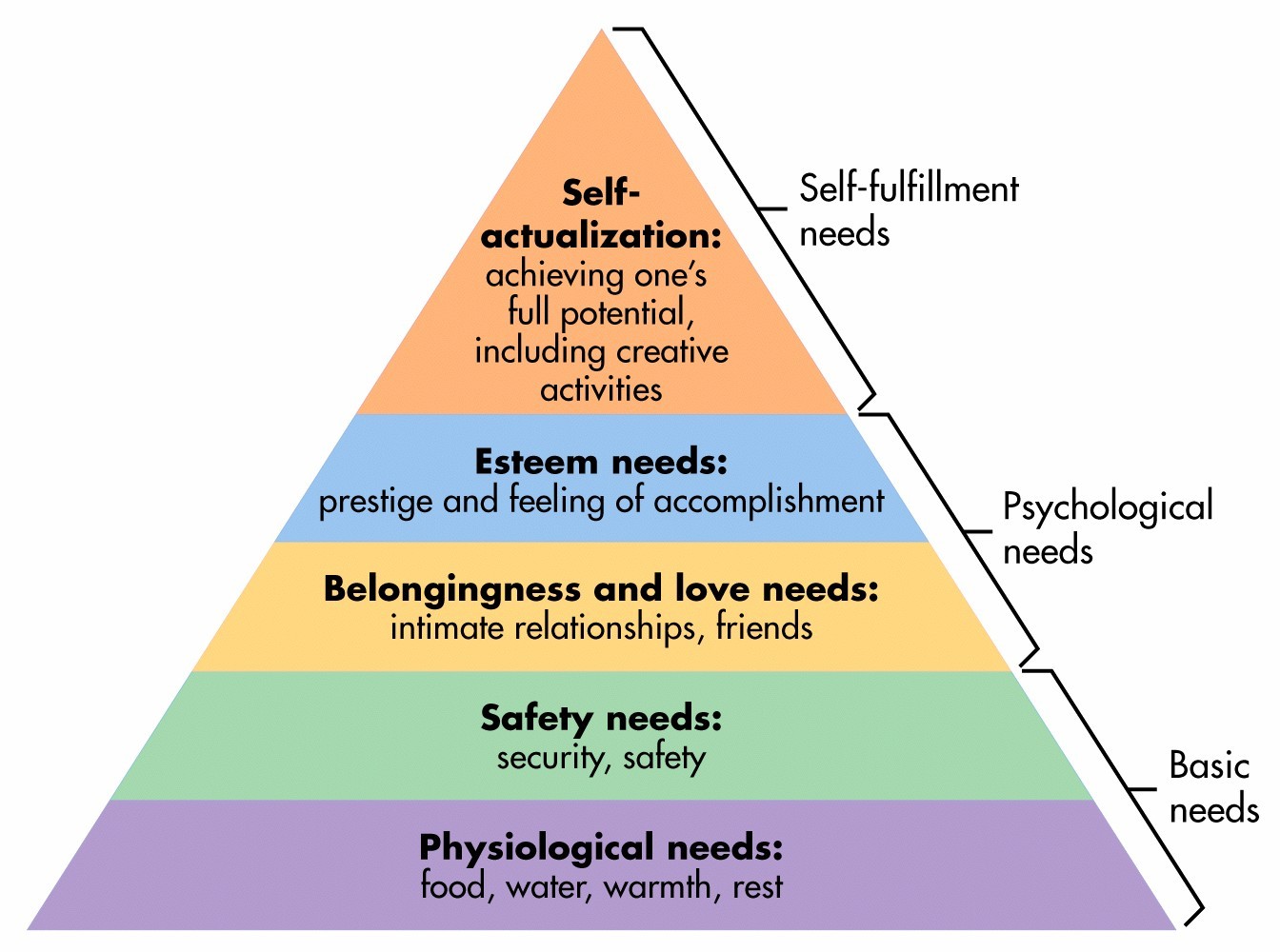

As a home owner myself let me tell you that you are right to so aspire, Jessica. It delivers a surprisingly powerful sense of belonging and security. Perhaps not so surprising, actually, when one considers Maslow’s hierarchy of needs:

There it is, right at the base of the pyramid, food, water, warmth and rest. A home. As a mother, Jess, you’ll appreciate it all the more.

Which is why I have to wonder at your constant boosting of house prices? Your love of population growth, ceaseless reproduction of RBA (bubble central planning) propaganda, foolish boosterishness around a clearly failing economy, harassment of “doomsayers” and today it’s enormous and corrupt mortgages that she loves:

Another day, another dire warning that Australian households are about to crumple under the crushing weight of debt.

The Chicken Littles of this world were set chirping last week by a special report by the International Monetary Fund, which today kicks off its annual meetings.

…Scared? Don’t be. At least, be alert, not alarmed.

Now, it’s absolutely true that Australia’s household debt to income ratio is one of the highest in the world. It’s also true, and observed by the IMF in its paper, that richer countries are more able to service large household debts. To a large extent, high debt is more a marker of our wealth, not a portent of its doom.

…Again, there’s no shortage of scary headlines, perhaps the most sensational of which in recent times come from the investment bank UBS and two reports on Australia’s so-called “Liar Loans”.

A survey by UBS of 907 recent mortgage recipients found firstly, that “in 2017 one-third of mortgage applications were not factual and accurate” and secondly, that “around one-third of interest only customers do not know or understand that they have taken out an interest only mortgage”.

Bad news comes in thirds, it would seem.

But it seems the headline writers at UBS have got ahead of their own findings, somewhat.

On the first headline, what UBS’ survey actually found was that 67 per cent of mortgage holders surveyed stated that their application was “completely factual and accurate”. A further 25 per cent said it was “mostly factual and accurate”, 8 per cent said “partially factual and accurate”.

What tripe, Jess. It’s obvious that Australian households will need to deleverage and soon, and when they do, houses will be much easier to buy for your generation. Sure, banks will not lend as much after the price falls and will knock some borrowers out. And unemployment will be higher too.

But as a group, FHBs will still be far better off with lower prices and a deposit that is within reach with hard work, rather than skipping away every five minutes as the bubble inflates. It will be a lot more meritocratic as well as those with the skills and a work ethic will win through, rather than the gamblers winning at every turn.

What this boils down to for Ms Irvine is that she wants a home but has gotten herself a highly-paid job with a giant real estate agent who’s interests are best served by ensuring that she doesn’t get one. She’ll get there, no doubt, but her cash-for-comment campaigning for higher house prices will guarantee many of her generation won’t.

The reverse is also true. When prices fall and her business goes under, many more of her generation will be able to buy homes, but she may not as Domainfax hits the skids.

In short, poor Jess Irvine’s career path has turned her into a professional hypocrite.