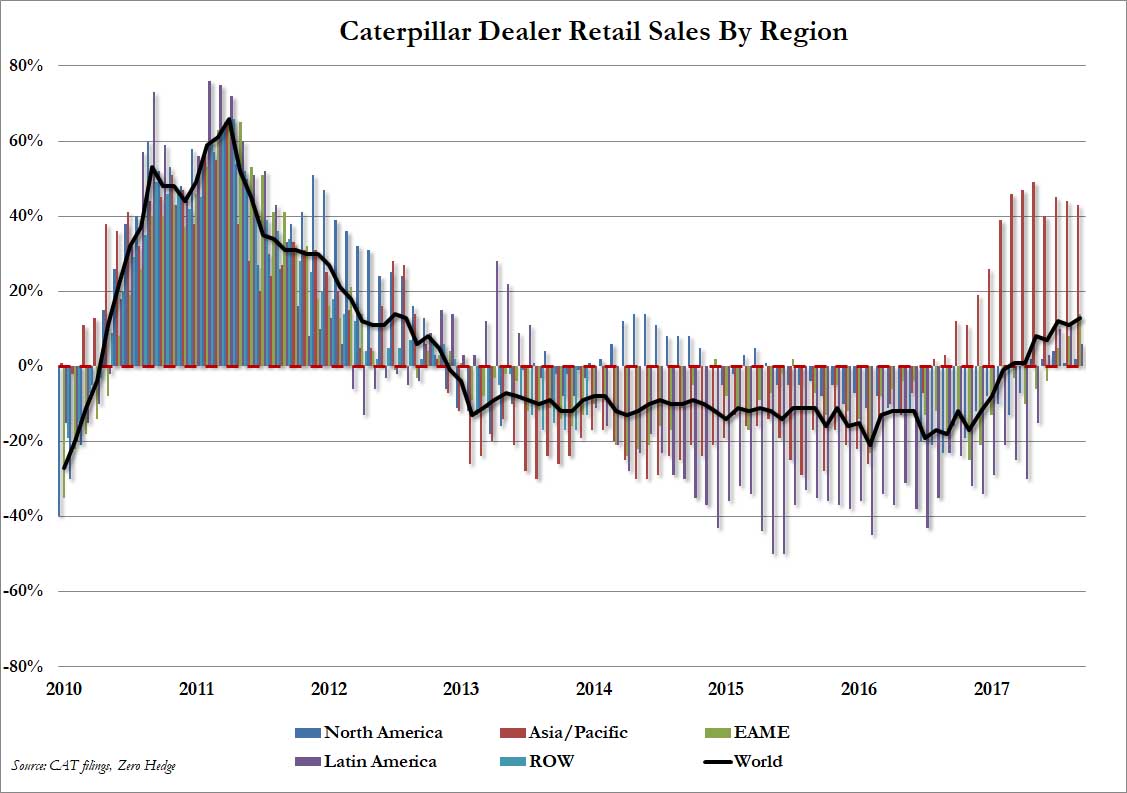

Caterpillar continues to see strength in a number of industries and regions, including construction in China, on-shore oil and gas in North America, and increased capital investments by mining customers. We are working with our supply chain to increase production levels to satisfy customer demand for those markets that have improved.

In July 2017, Caterpillar provided an outlook range for full-year 2017 sales and revenues of $42 billion to $44 billion, with a midpoint of $43 billion. The company now expects full-year 2017 sales and revenues of about $44 billion.

For the full year of 2017, Caterpillar now expects profit per share of about $4.60, or adjusted profit per share of about $6.25. The previous outlook for 2017 profit was about $3.50 per share at the midpoint of the sales and revenues outlook, or adjusted profit per share of about $5.00. The company now expects to incur about $1.3 billion of restructuring costs in 2017, a slight increase from the previous outlook of about $1.2 billion. The outlook does not include potential mark-to-market gains or losses related to pension and other postemployment benefit (OPEB) plans. While the final impact will not be known until year end, the impact would be negative to profit based on information as of the end of the third quarter.

“As a result of our team’s strong performance, we are raising our 2017 profit outlook,” continued Umpleby. “We are executing our new strategy for profitable growth based on operational excellence, expanded offerings and service.

One word for ya: China. As we know, the owner is out:

Long-time China bull Kerry Stokes is selling his biggest investment in the world’s second-largest economy – the Caterpillar heavy machinery franchise he built from scratch 17 years ago.

The surprise $540 million sale of WesTrac China allows Stokes to exit what has been at times a difficult business and deploy capital back to Australia where Seven Group Holdings is looking at a range of deals in the energy and mining sectors.

The sale is not a vote of no-confidence in the outlook for the Chinese economy but does reflect concern about the credit risks of operating in what has virtually become a cashless society where defaults are on the rise.

It was also a matter of good timing for Seven after a neighbouring Caterpillar dealer in China, Lei Shing Hong, approached the Australian company about a possible deal. Kerry Stokes’ son, Seven Group chief executive Ryan Stokes, who oversaw the transaction, was happy to engage.

It was always challenging collecting receivables from customers in China, but over the past 12 to 18 months the WesTrac business experienced an increase in customers, particularly large state-owned enterprises looking to settle their debts with notes issued by Chinese provinces.

The origin of debt in China has become a growing concern for investors.

Advertisement

It’s nicely timed and very sensible vote of no confidence in China.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.