East coast gas market dynamics are going through a fundamental shift

The market is resigning itself to the fact that recent actions to restrict LNG exports and divert gas into the domestic market will not have a significant impact on bringing down east coast gas prices. So what will? In our view normal supply/demand dynamics (if allowed to function), will provide a solution. A period of higher gas prices will stimulate new supply and reduce demand, the combination of which should act to eventually bring down prices. This report focusses on the next wave of gas supply: What undeveloped gas can be brought online, by when and at what price?

Declining Vic gas supplies a major issue, but multiple supply options in wings

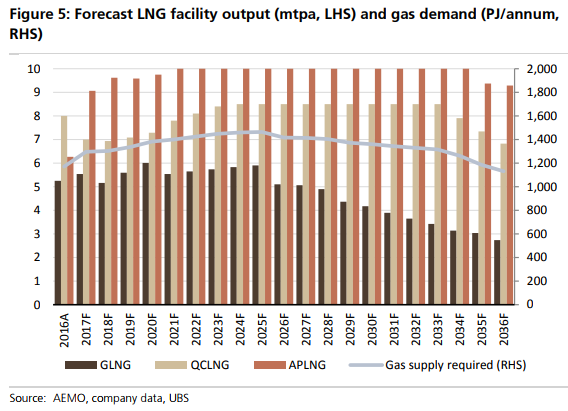

In its most recent gas market analysis, The Australian Energy Market Operator (AEMO) forecast east coast gas demand to decline from 642 PJ in 2018 to 598 PJ in 2019, primarily due to lower gas-powered generation (GPG) demand. But declining Gippsland Basin Joint Venture (GBJV) supplies (from 330 PJ in 2017 to 244 PJ in 2018) means the east coast market finds itself reliant on gas diverted from LNG to balance the market. Only 3 new gas developments are underway at the moment (Sole, Arrow Expansion and Senex Western Surat Gas Project). We identify 16 potential gas supply opportunities for the east coast market. However many of these projects have multiple challenges, including appraisal risk as well as cost, regulatory and timing uncertainty.

Reliance on Qld LNG to continue, LNG imports not cheap but may be needed

Key conclusions: 1) the east coast will remain reliant on diverted Qld LNG supplies for at least the next 5 years (and most likely longer), as alternate gas supplies of any size are still a few years away; 2) development cost & distance of new supply from markets means that development is unlikely to exert material downward pressure on east coast gas prices any time soon; 3) declining Victorian supplies means that SA and NSW will become increasingly reliant on alternate sources; 4) the largest sources of potentially lower cost supplies (NSW, NT shale) face regulatory issues; 5) there is room for LNG imports, but landed price is a key challenge, and; 6) the elephant in the room is GBJV – just how much additional gas is the JV able to bring to the market (and at what price)?

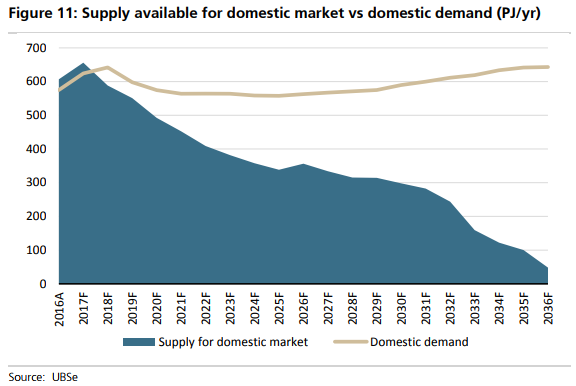

This is how ugly it will get without more supplies:

As the cartel sends it all to Asia:

Advertisement

And here are the options to fill the hole. Importing it:

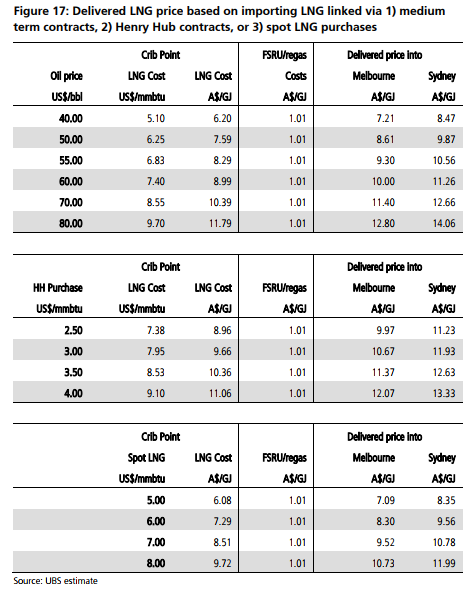

AGL has proposed importing LNG into Crib Point in Victoria. Our analysis of LNG imports concludes that importing gas could land in Melbourne for around $9/GJ, though it will largely depend on the contracting strategy employed by AGL.

We expect AGL to consider 3 contracting options for importing LNG. 1) Enter into medium term contracts, 2) importing LNG from the US, and/or 3) purchase opportunistic cargoes from the spot LNG market. Each option has its own risk/reward profile. Medium term contracts are typically oil linked, so AGL may need to enter into oil hedges to mitigate against any oil price volatility. Importing LNG from the US is seen as a higher cost option given where oil is trading at the moment, and would exposure AGL to Henry Hub pricing risk. Spot LNG prices have been as low as US$5/mmbtu in the past 2 years, however despite most analysts predicting we are heading into an oversupplied LNG market, recent spot prices have spiked to US$8.50/mmbtu. If we assume AGL goes down the path of locking in a medium term supply agreements, it may be able to lock in prices below other recent transactions with its 2nd tranche of imports, given the import period marries well with lower Asian LNG imports.

The increasing seasonality of LNG demand means that AGL could negotiate LNG purchases from one of the larger Asian importers, who may be looking to reduce supply during northern hemisphere summer months. The following table looks at the landed price of LNG into Melbourne and Sydney based on the 3 different options. Medium term contracts are assumed to be at 11.5% slope + $0.50 delivery

Or, developing it:

Advertisement

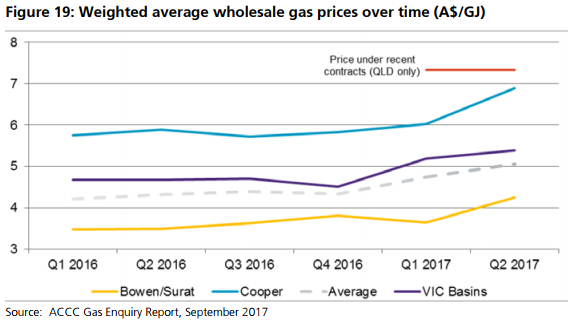

A recent ACCC report included the following chart, which shows the weighted average wholesale gas price for eastern Australia since the start of 2016. The chart shows that the weighted average wholesale price has increased from around $4.30/GJ in 1Q16 to just over $5/GJ by 2Q17. It should be noted that the average is weighed down by a number of long term legacy gas supply agreements with Qld CSG suppliers (e.g. APLNG supply contract with ORG). The ACCC also reported that the weighted average price of new gas contracts entered into since the start of 2016 for 2018 delivery was approximately $7.30/GJ (at Wallumbilla in Qld or explant in Victoria).

So wholesale prices are increasing as legacy contracts roll off and new contracts are struck at higher prices. In our previous section we outlined the major sources of new gas supplies. But what is the cost of developing these new gas supplies and will their development bring down gas prices?

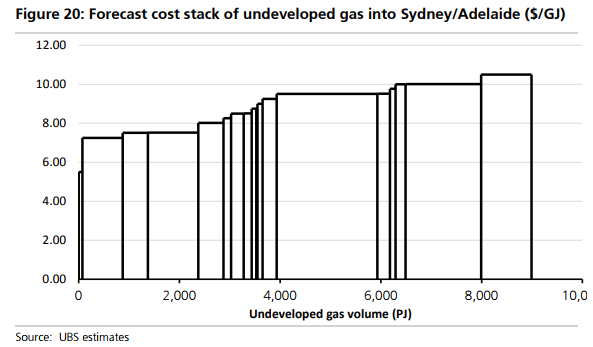

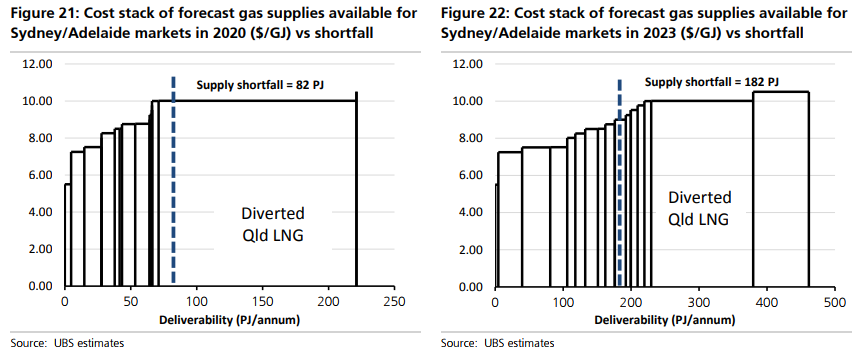

The following chart summarises our estimate of the cost stack of undeveloped gas supplies delivered into the Sydney or Adelaide markets. We use these markets as Qld and Victoria will likely have access to lower priced gas, thanks to holding more indigenous gas supplies that are most likely to be developed, leaving Sydney and Adelaide markets increasingly the more expensive markets for gas.

The above chart shows that, on a delivered basis, there is more than 3,000 PJ of gas that could be developed and supplied into these markets at gas prices below $9/GJ. But the above chart is misleading as it doesn’t provide any information regarding gas deliverability or timing. The real question is: How much gas deliverability is available to be supplied into these markets in 2020 or 2023 and at what price? The following charts show our forecast gas deliverability from currently undeveloped supply sources to meet demand. In 2020 we estimate the shortfall of gas supply into Eastern Australia is 82 PJ, which increases to 182 PJ by 2023

The above charts show that, due to the time, cost and regulatory challenges involved in bringing new gas supplies to market, insufficient gas is available by 2020 to avoid the need to divert Qld LNG south (which we estimate will have a delivered price of around $10/GJ). By 2023, the supply shortfall will have increased to 182 PJ, but the additional 3 years provides greater opportunity to bring new supplies into the market. This includes options such as NSW CSG and LNG imports. Overall we see some potential for the marginal cost of new gas supplies to be below $9/GJ (delivered), however this will partly depend on whether NSW CSG can be developed (we estimate the delivered price of Narrabri gas to be $7.25/GJ). What do we conclude from this analysis?

(1) There is plenty of gas available to meet future domestic gas shortfall, but one of the larger volumes is high priced gas diverted from Qld LNG.

(2) The high gas price of diverted LNG provides an incentive to develop new gas supplies to meet this shortfall at a lower price

(3) We expect southern markets will remain reliant on diverted Qld LNG until at least 2022, and potentially beyond this date depending on the pace and scale of development of alternate gas supplies.

(4) Approximately 50% of the shortfall can be met by gas supplies that are expected to be sold at or below $8/GJ. Prices of $9/GJ may be required to meet the forecast shortfall in 2023, but to achieve this outcome, the development of NSW CSG would be needed in our view.

(5) To truly bring down future gas prices to levels below $8/GJ on a sustainable basis will require the discovery and development of large, new (and ideally liquids rich) gas volumes. The most likely location of these volumes is offshore Victoria.

(6) Discovering more cheap gas requires time (no exploration activity planned until late 2018 at the earliest). It will likely take 6-7 years to appraise and develop the new supply sources, and offshore Victorian acreage has been explored for many years – what is the remaining prospectivity?

(7) The above analysis doesn’t take into account any potential pipeline constraints. Companies with existing unutilised or underutilised capacity may be able to ship gas at a lower incremental cost, but where capacity expansion is required, the volume of gas available vs the cost of expansion may place limits on the movement of some gas.

And the conclusion:

East coast gas pricing outlook

This price outcome is consistent with our current view that contract prices will average in the $9-11/GJ (delivered) over the next 5+ years.

This should see the weighted average gas prices to increase from the current levels of $5/GJ to over $7/GJ as legacy contracts roll off;

New gas contract prices to trend above $7.30/GJ ex-field, which equates to >$8.30-9.30/GJ delivered into Sydney or Adelaide, depending on where the gas is sourced from (higher if sourced from Qld); The east coast market will remain reliant on diverted Qld LNG supplies until at least 2022 in our view. A substantial reduction in east coast gas prices will require the discovery and development of a large, low cost gas volume. The most likely location of this is offshore Victoria, but not a lot of activity is planned in the near term and development from discovery could be 7+ years away.

With Qld set to be the marginal price setter in the market for the next 5 or so years, we see delivered contract prices to migrate above $9/GJ.

Downward pressure on prices beyond this period requires a step-up in exploration, appraisal and development efforts as well as removal of some regulatory barriers impeding exploration and appraisal activities.

The answer is obvious and it is not market-based. Gas reservation needs to be ramped-up aggressively and the prices fixed.

Remaining gas reserves are too expensive to develop privately. They should be expropriated and developed by a gas national champion.

Advertisement

This market has failed. Only government can fix it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.