From Roy Morgan Research:

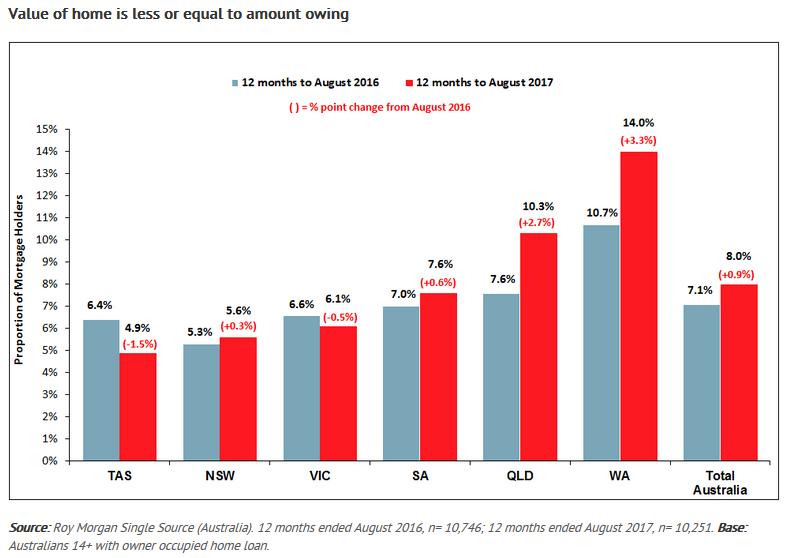

It’s Official: Overall some 8% (345,000) of mortgage holders in Australia in the year to August 2017 have been identified as having little or no real equity in their home, an increase from 7.1% twelve months ago. This is based on the fact that the value of their home is only equal to or less than the amount they still owe, placing them at considerable risk if they have to sell or prices decline.

These are the latest findings from Roy Morgan’s Single Source Survey which is based on over 50,000 interviews per annum, including more than 10,000 with owner occupied mortgage holders.

Apart from the ability to keep up with mortgage repayments, another critical factor in assessing financial risk for mortgage holders is to compare the value of their property with the amount outstanding on their loan. The purpose of this is to establish the level of equity (if any) they have, as this is a major component of most households’ financial position and potential risk.

Mortgage holders in WA most at risk

On average, the value of properties in Australia subject to a mortgage is well in excess of the amount outstanding but there are problem areas. The state at highest risk is WA where 14% (71,000) of mortgage customers’ have no real equity in their home.

Over the last 12 months there has been an increase of 3.3% points in the proportion of mortgage holders in WA with little or no equity in their home. Tasmania has the lowest proportion of mortgage holders with little or no equity in their home, with only 4.9% (4,000). NSW is the second-best performer with 5.6% (81,000) of mortgage holders facing equity risk, followed by VIC with 6.1% (62,000), SA with 7.6% (26,000) and QLD with 10.3% (89,000). The strong performance in VIC and NSW is due mainly to the rapid rise in Sydney and Melbourne prices which has generally outpaced the amount owing on mortgages.

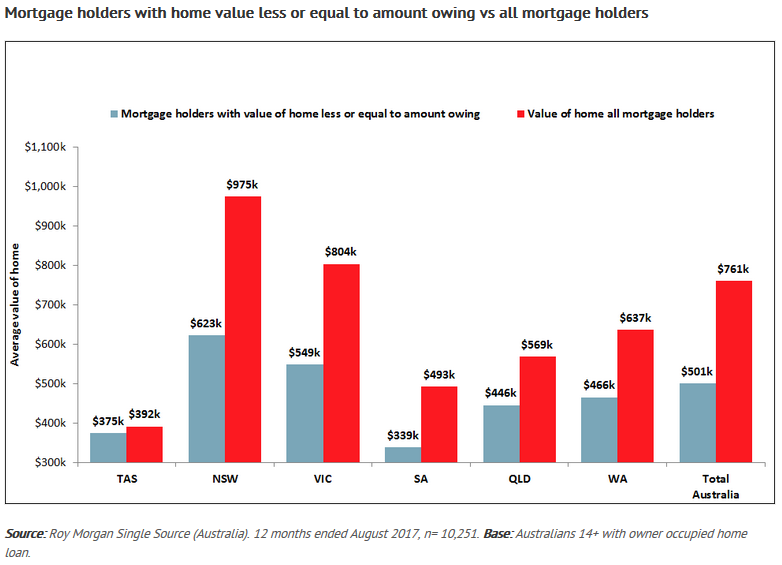

Lower-value homes face more equity risk

The mortgage holders with little or no equity in their homes have much lower average house values ($501,000) compared to all mortgage holders ($761,000).

Across all states, the value of the homes overall with a mortgage is much higher than the value of homes owned by mortgage holders who have no real equity in their home. In NSW for example, the average value of homes with a mortgage is $975,000, compared to the much lower average of $623,000 for mortgage holders where the value of their home is less or equal to the amount they owe. In VIC the figures are $804,000 for the average home value with a mortgage, well above the $549,000 for mortgage holders with no equity in their home.

Norman Morris, Industry Communications Director, Roy Morgan Research says:

“Over the last 12 months there has been an increase from 311,000 to 345,000 in the number of home borrowers having no real equity in their homes, this represents a considerable risk, particularly if home values fall or households are hit by unemployment. Other potential contributing factors to this increase in mortgage stress include borrowers maintaining debt for other purposes rather than paying off their loan and the use of interest only loans. If home-loan rates rise, the problem would be likely to worsen as repayments would increase and home prices decline, with the potential to lower equity even further.

“The mining boom and associated increase in housing demand and house prices in WA, followed by the slowdown in the mining sector in WA, and a decrease in house prices continues to see it having the highest proportion of mortgage holders faced with little or no equity in their home. If house prices decline further in WA and unemployment increases then more mortgage holders will be facing a tough situation.

“Borrowers in lower-value homes continue to be among the most likely to be faced with the problem of little or no equity in their homes. Higher-value properties with a mortgage appear to be facing a much less risky position because they are likely to have had their loan longer and may have had a far larger deposit, particularly if they have traded up.

“Although the majority of Australians with a mortgage have considerable equity in their home, speculation is emerging that the growth in house prices must soon come to an end and when it does, so will the growth in home equity.

“This data is drawn from the Roy Morgan Single Source survey which interviews over ten thousand owner-occupied mortgage holders per annum, enabling an in-depth understanding of their complete financial position, including the estimated value of their home. This database is unique and provides detailed insights for anyone involved or interested in this key segment of the Australian population”.