The Commonwealth Bank of Australia’s apparent failure to properly monitor transactions for money laundering and possible terrorism funding makes action from American regulators inevitable say financial crime experts.

American lawyers have told Thomson Reuters that CBA was already responding to information requests from a number of US agencies with differing mandates and enforcement agendas and the announcement of a formal investigation, a precursor to enforcement action, is now only a matter of time.

Edward Wilson jnr, partner at Venable in Washington, DC, said American financial intelligence unit FinCEN would already be involved in the case through various agreements with Australia’s anti-money laundering (AML) regulator Austrac.

“FinCEN is already interested in this case. CBA has US branches and deals in US dollars. For both reasons, CBA will be required to comply with American AML laws,” Mr Wilson said.

…An Australian financial crime investigator, speaking on condition of anonymity, said the discovery process that is taking place at CBA was creating major headaches for the institution.

“The bank is in serious trouble because there are internal reports talking about these things from several years ago. That’s my understanding from talking with various people, a number of whom were former bank executives and managers,” he said.

…Stanley Foodman, founder of Foodman & Associates in Miami, said the seriousness of the allegations and the fact CommBank has a New York presence suggested FinCEN and other federal and New York state regulatory agencies would investigate.

“A request from another regulatory authority is a likely trigger for a US federal and New York state regulatory investigation,” Foodman said.

“Also, any US federal or New York state regulator reading the international press regarding this matter could initiate its own US-based investigation.”

The best course of action now for CBA would be to disclose everything to the US regulators, sources said.

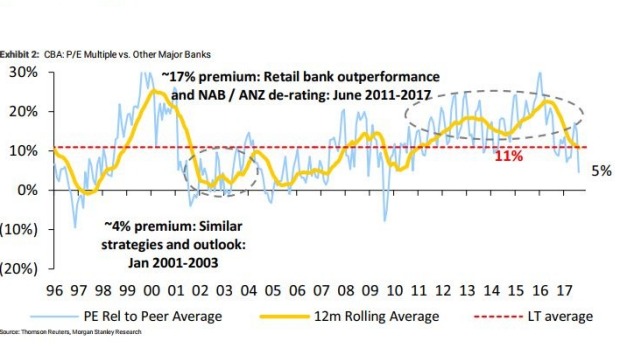

CBA’s P/E premium to peers has contracted to its lowest level since 2010. However, we believe the stock remains over-valued and execution risks have increased,” they said.

“CBA has been Australia’s premium bank for 20 years: CBA has traded at an average P/E premium of ~11 per cent to the other three major banks over the past 20 years.”

The research said CBA’s shares had only been at a discount for to its peer group over four short periods in 1996-97,2001,2004 and 2009. Morgan Stanley attributed this to factors including a higher return profile, clear strategy and “superior execution.”

But Wiles tells investors CBA’s premium is now harder to justify and that Morgan Stanley’s earnings estimates to do not factor in potential penalties and or other implications from AUSTRAC’s court action against the bank.

AUSTRAC is alleging CBA failed to comply with money laundering and anti-terrrorism financing rules over a a number of years.

“The outlook for retail banking has become more challenging and the problems at ANZ and NAB have now been largely addressed,” the research said.

“In fact, we would argue that the majors’ strategies and outlook are more similar today than they have been at any time since 2003 before ANZ bought NBNZ (late 2003) and NAB suffered from its FX trading losses and a deterioration in UK profitability (2004).

“With this in mind, we note that CBA traded at an average premium of ~4 per cent from 2001 to 2003.

As the Commonwealth Bank money laundering-terror funding affair worsens, suddenly it becomes apparent that the innocents, CBA shareholders, are looming as the major victims.

Already they have watched their CBA shares fall about 10 per cent since the Austrac announcement on August 3 of civil court action against the lender for alleged breaches of money-laundering and anti-terror financing laws. Shares in Australia’s second largest bank, Westpac, were almost steady over the same period.

Accordingly, on the basis of a comparison between CBA and Westpac shares, the market thinks that the combination of corporate damage and fines to CBA will be between $13 billion and $14 billion. That’s more than last year’s CBA $10 billion profit.

If, theoretically, the CBA fines and damages (not the impact on the business) total more than one year’s profit or $10 billion then CBA shareholders not only lose out via the share price fall but will be forced to inject a major chunk of the loss back into the company via lower dividend and/or share issues so as to restore the bank’s capital ratios.

In other words it’s the shareholders rather than the directors and managers who pay the fines and damages.

There is something wrong with a system where this happens.

No, there isn’t. While if it turns out that the directors have acted corruptly then they should be charged accordingly, and the bank claw back pay and bonuses. This is still obviously small beer compared to the overall damage to the firm.

Advertisement

That’s where shareholders have to pay which, frankly, they should. They all bid up CBA to a high premium on its superior earnings without asking why the earnings were there. CLSA’s Brian Johnston pout is beautifully:

“It is also becoming clear that the AUSTRAC AML allegations go well beyond a simple “coding” oversight on its fleet of Intelligent Deposit Machines, and seem to point to a culture where CBA’s management were willing to tolerate risk slippage/customer dissatisfaction in order to deliver cost efficiency and excess shareholder returns in a challenging growth environment.”

Risk and reward. CBA shareholders wanted higher returns, they took a risk to get them.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.