Over the last two decades, Australia has experienced remarkable conditions in the housing and mortgage markets. The extreme growth in land prices, due in large part to the actions of the nation’s passive and reluctant financial regulators, has now placed the housing market in a precarious situation which is now holding the rest of the economy to ransom. We believe that should the federal and/or state governments, including the RBA, fail to enact ‘successful’ policies to stimulate the artificial demand component in the housing market, dwelling prices may be close to reaching its peak as growth in mortgage debt slows. The economy is currently creaking under the weight of a historically large stock of household debt, a fair proportion of which will never be repaid by borrowers. Mortgage control fraud in Australia is widespread and many international wholesale lenders – who assist in funding the banking system – may find out the hard way that they have invested into nothing more than a $1.7 trillion ‘piss in a fancy bottle scam.

Mortgage Control Fraud

According to Professor William K. Black (a leading specialist on bank control frauds), lenders often engage in fraudulent practices. This is termed “control fraud”, whereby the controlling agents use the firms as a weapon and shield to intentionally defraud by lending far in excess of what borrowers are capable of servicing over the life of the loans. Under these conditions, lenders produce guaranteed, exceptional short-term profits through a four-part strategy: extreme loan growth, high leverage, minimal loss reserves and declining underwriting standards.

Mortgage control fraud in Australia has reached epidemic levels, especially in direct lending to high-risk borrowers and repackaging these loans into seemingly high-quality RMBS. As per our Parliamentary submissions into the Penalties for White Collar Crime Inquiry (2016) and Consumer Protection in the Banking, Insurance and Financial Sector Inquiry (2017), including field research, has provided evidence to suggest the regulators (ASIC and APRA) have played a critical role in allowing mortgage control fraud to flourish despite laws to protect both consumers and institutional investors from this white-collar crime.

The unfortunate reality for victims of mortgage control fraud is that our regulators do not investigate allegations brought to their attention despite forensic evidence (paper trails) demonstrating evidence of fraud. At the centre of the control fraud is the intention to deceive both borrowers (asset side) and those who fund a bank’s ability to expand their mortgage book (liabilities side). The fraud is also facilitated by the issuance of large numbers of interestonly loans which have the appearance of affordability during the initial years despite borrowers having no ability to service the principal portion of the loan.

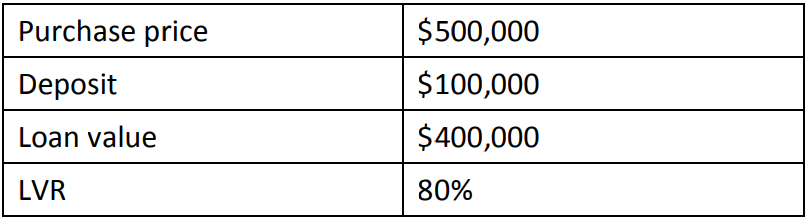

The LVR Scam

The loan to value ratio (LVR) is calculated by dividing the value of the loan by the purchase price of the property. A simple example is illustrated below.

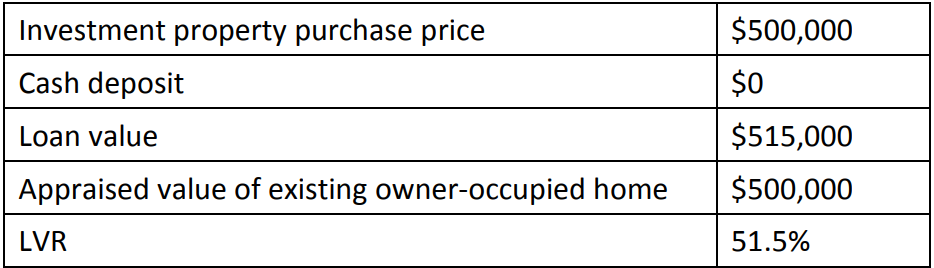

While this simple calculation is common practice in other jurisdictions, Australian lenders tend to use a more complicated method: the ‘combined loan to value ratio’ (assome UK banks use). This approach allows lenders to report the cross-collateral security of one property which is then used as collateral against the total loan size to purchase another property. This approach substitutes as a cash deposit. The use of unrealised capital gain (equity) of one property to secure financing to purchase another property in Australia is extreme.

This method also makes it easy for investors to accumulate multiple properties in a relatively short period of time despite high house prices relative to income. This has exacerbated risks in the housing market as little to no cash deposits are used. The example below indicates how the LVR would be calculated i.e. a debt-free borrower close to retirement who purchased their owner-occupier home in the 1980s and has bought an investment property today.

Another way to reduce the LVR is to divide the loan into multiple segments (split loans). Lenders then record the multiple loans using a simple unweighted average which does not take individual loan values into account. These examples demonstrate how Australian lenders have been able to issue loans to investors in excess of 100% of the purchase price. Lenders then record these loans as having far lower LVRs than is actually the case.

Ah yes, the great rehypothecation rort. And the implications for bank capital are, well, see for yourself, formerly from Deep T.:

There are two ways an Australian Deposit taking Institution (“ADI”) calculates capital to be allocated against a residential mortgage. Either in accordance with APRA’s APS 112 Attachment C or under Advanced Basel II methodology. Let’s address the rather simple APRA methodology first and then look at the implications of the advanced method.

My critics may be saying that I oversimplify. If it’s the simple truth then they’re correct but you can’t understand the bigger position without knowledge of the basic fundamentals. That’s where it starts.

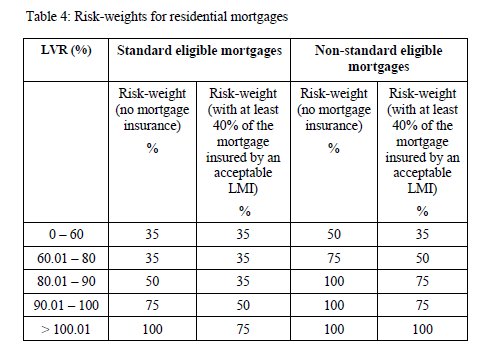

My simple question is, how much capital does an ADI need to allocate to a mortgage over time? Let’s start with a $100 mortgage and the table below from APS 112 for standard mortgages.

The way ADI capital calculations are articulated, a 100% weighting on a $100 loan asset translates into $8 of capital but APRA weights standard residential mortgages as per Table 4 which shows a lower weight for lower LVR’s.

Therefore if a mortgage is standard and written at 95% LVR then the capital allocated is $100 *75%*8% = $6. On the basis that an ADI wants a 20% return on capital then a borrower pays $6*20%=$1.20 pa to the bank as a return on capital. We’ll not complicate matters by doing the calculation for mortgage insurance as this also involves calculating the capital required for the LMIs.

However, I will make the unsubstantiated statement that the total capital now in the system needed by both the ADI and LMI is at least equal to the amount required for an uninsured mortgage. However, for a very long time it was not and a significant arbitrage was in the system between ADI’s and LMI”s until 2008.

The definition of standard loan is as follows as referenced in APS112.

6. A standard eligible mortgage is defined as a residential mortgage where the ADI has:

(a) prior to loan approval and as part of the loan origination and approval process, documented, assessed and verified the ability of the borrowers to meet their repayment obligation;

(b) valued any residential property offered as security; and

(c) established that any property offered as security for the loan is readily marketable.

The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region.

Sounds reasonable enough, even the last sentence. But here lies the “arbitrage the system” opportunity that every banker dreams of. APRA in APS-112 have insisted that property is revalued by an ADI if “it becomes aware of a material change in the market value of property in an area or region”. I will express an opinion here that I’m sure APRA was trying to protect against properties falling in value but have left open the biggest game in town for all our banks.

Currently the major and regional banks use the services of the new technology of automated valuation models (AVMs) to revalue their mortgage books upwards to decrease their capital requirements. Has a light switched on yet as to why there has been such a dramatic rise in the use and media coverage of those property valuation spruikers. If anyone knows of one of those banks who do not use AVMs can you please let us all know.

So what is the effect of continually revaluing the properties upwards? Using our standard 95% LVR mortgage above, let’s assume a revaluation so that the LVR is now 85%. The capital required is now $100*50%*8%= $4 with a return on capital requirement of $4*20%= $0.80 pa. Quite a difference, and if we go one step further, then the result and achieve a 75% LVR then the capital is now $2.80 with a return requirement of $0.56.

So with roughly a revaluation of the property of 20% (ask any property spruiker, “That’s nothin’ mate!”) a bank can save itself $3.20 of capital per $100 of mortgage which can be recycled as capital to support another mortgage. Think about how that increase in both return on capital and funds allocated to another mortgagor slave is an absolute incentive for bankers to perpetuate the cycle up of house price valuations. Their reward? Huge bonuses based on what is in essence a positive reinforcement spiral where everyone pats each other on the back for what a great job they’re doing. Well at least, that is, until the money runs out.

What was that? Did you hear anything? Maybe the sound of a slow burning fuse?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.