From CoreLogic’s Cameron Kusher comes a nice breakdown of last weeks’ ABS biennial survey of household income and wealth:

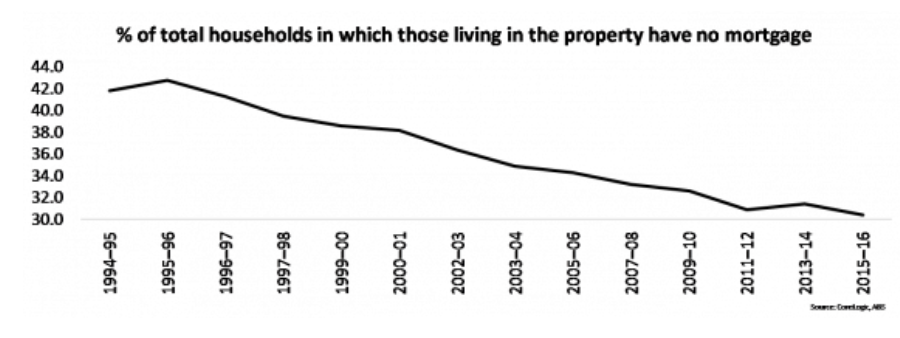

As at the 2015-16 release 30.4% of households were lived in by someone that owned that property outright. This figure was lower than the 31.4% in 2013-14 and as the above chart shows it has been steadily trending lower over recent years. In fact, at the peak throughout the timeframe shown, 42.8% of households had no mortgage in 1995-96. This is an interesting statistic when you consider than many people suggest that lower mortgage rates result in improved housing affordability. In June 1996 the standard variable mortgage rate was recorded at 9.75% compared to a mortgage rate of 5.4% in June 2016. The ongoing decline in mortgage rates has pushed dwelling values higher and although it has made servicing mortgage debt easier it has not led to a greater proportion of the population living mortgage free.

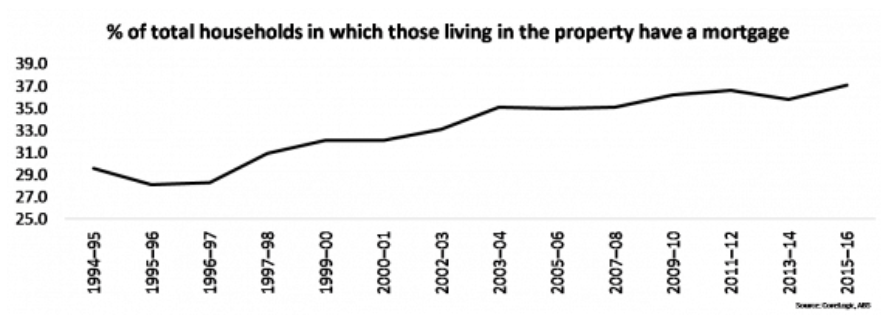

With fewer households owning their home outright, there has been an increase in the proportion of households that live in a home that they own and still carry mortgage debt. In 2015-16, 37.1% of households had mortgage debt which has increased from 35.8% in 2013-14. At its low point over the period highlighted on the chart, 28.1% of households had mortgage debt in 1995-96. Since 2003-04, there has consistently been a higher proportion of households with mortgage debt than those without.

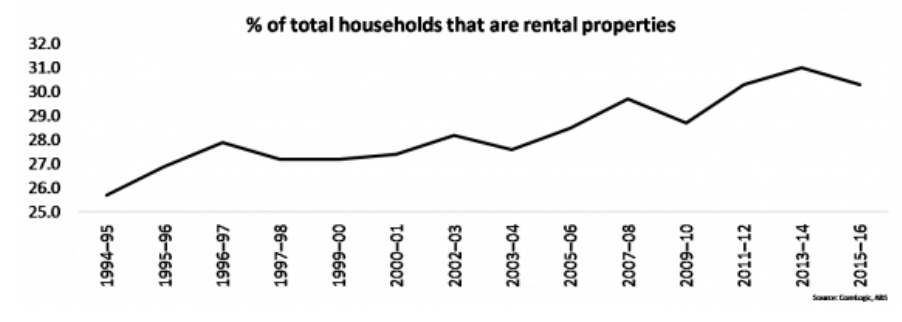

As the rates of outright home ownership have fallen there has been a rise in the proportion of households which are rented. Whereas outright home ownership has continued to fall and ownership with a mortgage has risen, it is interesting to note how the proportion of rental households has actually declined since the last survey. The latest data shows that in 2015-16, 30.3% of households nationally were rented compared to 31.0% in 2013-14. Back in 1994-95 only 25.7% of households were rented…

The charts presented highlight how home ownership is continuing to decline which is leading to a greater proportion of the population either being in mortgage debt or renting. As the population ages this can create challenges especially if an increasing number of Australians are retiring but still carry mortgage debt. It also highlights that simply building more homes is not necessarily a solution to increasing home ownership rates. As we’ve seen over recent years during a housing construction boom first home buyer levels have been at near record-lows and housing investment levels have hit all-time highs…

We would expect that over the coming years, the rate of home ownership will continue to fall especially given we have seen dwelling values continue to climb since June 2016.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.