Grant Wardell-Johnson, a partner at KPMG’s Australian Tax Centre, has called for an end to (or major reform of) Australia’s dividend imputation system arguing that it is holding the economy back. From The Australian:

Australia introduced the imputation regimen in 1987 and made franking credits refundable for super funds, individuals and charities about 17 years ago.

I believe it is time to revisit and, possibly, rebalance our tax system such that we become more outward-looking.

Conceptually, one option is to move to a partial imputation system, using the funds saved from reduced franking credits to lower the company tax rate and to put a discount on unfranked dividends paid by Australian companies. This could be a general direction for change.

There would be five key advantages of such a move:

First, it would reduce the disincentive for Australian companies to invest offshore and enhance the chances of retaining head offices of major businesses in our capital cities…

Secondly, such a proposal would slightly tilt the investment bias away from safer short-term investments (which are more likely to produce franking credits) and towards longer-term ventures, possibly riskier, but ones which could produce significant market-generating innovations.

Third, it would reduce the incentive for high dividend payout ratios which can act as a disincentive to innovative investment…

Fourth, it would improve the attractiveness of R&D, through the discount on unfranked dividends. Currently the tax concessions associated with R&D cannot be passed on to shareholders.

And finally, the partial imputation system would still provide an incentive, albeit reduced, to pay Australian tax. It would also lessen the incentive for streaming taxable dividends…

It is not without accident that the last two decades have seen many countries retreat from full imputation, and adopt a partial system. The list includes the Britain, Germany, France, Italy, Finland, Norway, Singapore and Malaysia. The reason is largely that as our world becomes more global, imputation produces less benefit.

The idea certainly has some merit.

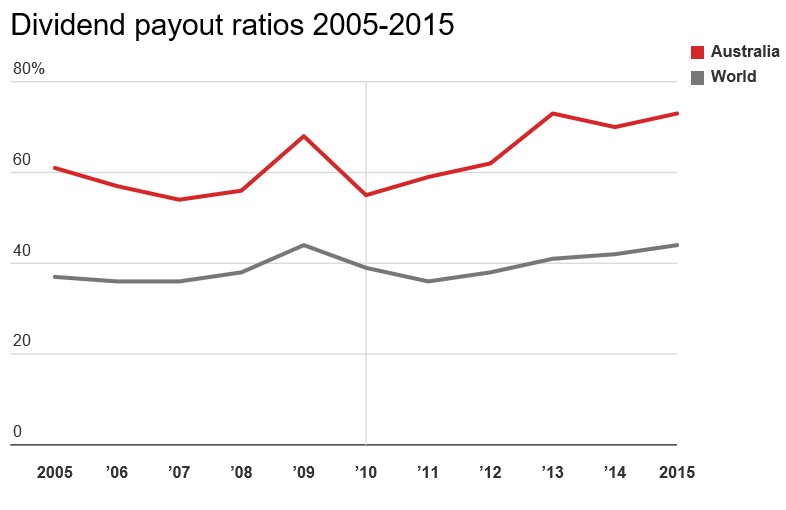

As argued by Paul Docherty, Senior Lecturer as the Newcastle Business School, Australian firms have high dividend payout ratios by international standards, and these have grown consistently faster than earning over recent years.

The average firm around the world currently returns less than half of profits to shareholders, whereas Australian firms return more than 70%:

This high payout ratio in Australia arguably comes at the cost of economic growth via less business investment. That is, the increased demand for dividends within an imputation tax system restricts firms’ access to their preferred source of financing: retained earnings.

Another issue not mentioned by Grant Wardell-Johnson is that Australia’s dividend imputation system is costing the Budget dearly thanks to the fateful decision in 2000 by former Treasurer, Peter Costello, which allowed the conversion of franking credits into cash refunds for shareholders. This enabled tax-free (mostly wealthy) superannuation holders over the age of 60 to claim imputation credits even though they pay no tax. The Australia Institute explains:

When companies pay dividends to Australia shareholders out of after-tax profit, shareholders also receive ‘franking credits’ which are a credit against their own tax obligation and based on the tax paid by the company. This system, known as ‘dividend imputation’ is unusual and only 4 other countries in the world use it.

However, in 2000 Mr Costello made the system even more generous to shareholders by allowing them to get a cash refund if they receive more in ‘franking credits’ than they actually owe in tax. Because income from superannuation is tax free for people over 60, high income retirees can use franking credits to get a cash gift of over 40 cents for every dollar they receive in dividends.

The ATO estimates that Peter Costello’s decision to allow ‘excess’ franking credits to be refunded as cash cost $4.6 billion in 2012-13.

At a minimum, Peter Costello’s changes in 2000 should be unwound so that investors should only be allowed to offset franking credits against tax that they have paid.

If the goal of dividend imputation is purely to avoid double taxation, then it makes absolutely no sense to allow retirees paying zero tax on their superannuation earnings to then also receive cash refunds for their franking credits. Such a situation is not only inequitable and effectively a subsidy to the (mostly) rich, but the cost to the Budget is simply too high to be ignored.