After completing stuffing its regulatory response to the gas market for several years, by resisting reservation and allowing reserves to consolidate in a blood-thirsty cartel, the ACCC seems finally to be getting ahead of things:

The national competition watchdog has taken the extraordinary step of releasing “appropriate benchmark prices” for natural gas on the east coast, after finding that many industrial users are being offered gas at more than double those rates.

The move by the Australian Competition and Consumer Commission came as the regulator calculated a large supply gap in the east coast gas market for 2018, echoing findings from the national energy market operator earlier on Monday. Both organisations handed their findings on Monday to Prime Minister Malcolm Turnbull, who is threatening to impose caps on LNG exports from Queensland unless the shortfall is filled.

The “benchmark” tariffs determined by the ACCC are based on forecast international spot prices for LNG in 2018 and are $7.77 a gigajoule for the south-eastern states, and $5.87 a gigajoule for Queensland.

They compare to prices offered to industrial users in the south-eastern states of $10-$16 a gigajoule, compared with historical prices of $3-$4, according to competition chief Rod Sims.

While the regulator said the benchmark prices were intended to be able to assess domestic prices, they look set to stir worries in the gas industry about potential regulatory intervention into commercial negotiations on contracts.

Here’s the full release:

The Australia Government has released the ACCC’s first interim report into the supply of, and demand for, wholesale gas in Australia.

The ACCC Gas Inquiry 2017-20 Interim Report focusses on likely supply and demand conditions for 2018. Estimates of gas supply have been compared to estimates of demand in the east coast gas market for 2018, based on estimates of exports obtained from the liquefied natural gas (LNG) producers and the Australian Energy Market Operator’s (AEMO) projections of domestic demand.

“The interim report projects a supply shortfall in the east coast gas market of up to 55 petajoules (PJ) in 2018, which could be as high as 108 PJ if domestic demand is higher than expected,” ACCC Chairman Rod Sims said.

“One PJ is enough gas to supply the residential needs of Warrnambool, Wollongong or Penrith, or a large industrial user for a full year. The significant shortfall is reflected in prices being offered to commercial and industrial customers for 2018 supply which are multiples of historical price levels of $3-4/GJ.”

“The effect of higher gas prices is felt right across the economy, from households to big business. Gas and gas-powered generators are also an important part of electricity generation, so higher gas prices feed in to higher electricity prices, leading to a double hit for many.”

“Over a third of the commercial and industrial (C&I) users the ACCC interviewed are considering either reducing production or closure due to high gas prices. For many of these users, gas is a feedstock to production or an essentially irreplaceable source of energy, and with the products they make often supplied on international markets higher gas costs cannot be passed on,” Mr Sims said.

The ACCC reported last year, in its East Coast Gas Inquiry, that the Queensland LNG projects caused a significant disruption to the market and the supply-demand balance. In 2018, the LNG projects will together produce over 70 per cent of the east coast’s gas and account for two-thirds of the east coast’s gas demand.

“The expected shortfall could be reduced to a significant extent if the expected sales on international LNG spot markets were instead redirected to the domestic market,” Mr Sims said.

“It is unclear why we are not seeing more steps being taken by the LNG projects to supply more gas into the domestic market. Although we accept some additional coordination costs would be likely and agreement of the joint venture parties of the LNG projects is required.”

The ACCC has determined appropriate benchmark prices against which to assess current domestic prices and prices being offered to C&I users. These benchmark prices, based on international LNG spot prices, are $5.87/GJ in Queensland and up to $7.77/GJ in the rest of the east coast. This latter price takes into account the cost of transporting gas from Queensland to users in the south, as some domestic gas buyers in the south now have to rely on contracting with the Queensland LNG producers to meet their needs.

Domestic users in the south are facing very high gas prices, largely as a result of the expected supply shortfall in the south and lack of competition between the southern gas suppliers. Prices in the south could be significantly reduced if additional sources of supply are developed in the south to increase the level of supply and diversity of suppliers.

“We are seeing domestic prices on the east coast well in excess of the appropriate benchmark levels and many C&I users needing to recontract for supply in 2018 and beyond are holding out in the hope of improved conditions. There is a lot of pent-up demand,” Mr Sims said.

“This situation on the east coast is in stark contrast with the situation in Western Australia, which is not connected to the east coast gas market. The west is expected to be well supplied in the short to medium term. For C&I users in the west, there are five suppliers competing for their business and prices are low, in the region of $6/GJ. On the east coast, particularly the southern states, users generally have only one supplier, and price offers in 2017 have generally been in the range of $10-16/GJ.”

“The situation in the east coast gas market is serious and options to address the problems in the immediate term are limited,” Mr Sims said.

The Australian Government has recently implemented the Australian Domestic Gas Security Mechanism (ADGSM), which allows for the restriction of LNG exports in an expected shortfall year, with the aim of directing those supplies to meet domestic demand.

“Export controls may go some way to addressing this shortage in the short term. However, further steps are needed to address the underlying problems of lack of gas supply and lack of diversity of suppliers in the east coast gas market. Supply-side solutions are needed to bring more supply and suppliers into the domestic market, particularly in the southern states,” Mr Sims said.

“Blanket moratoria and other restrictions on developing new supply should be replaced by case-by-case assessments to allow for new sources of supply to respond to high domestic prices.”

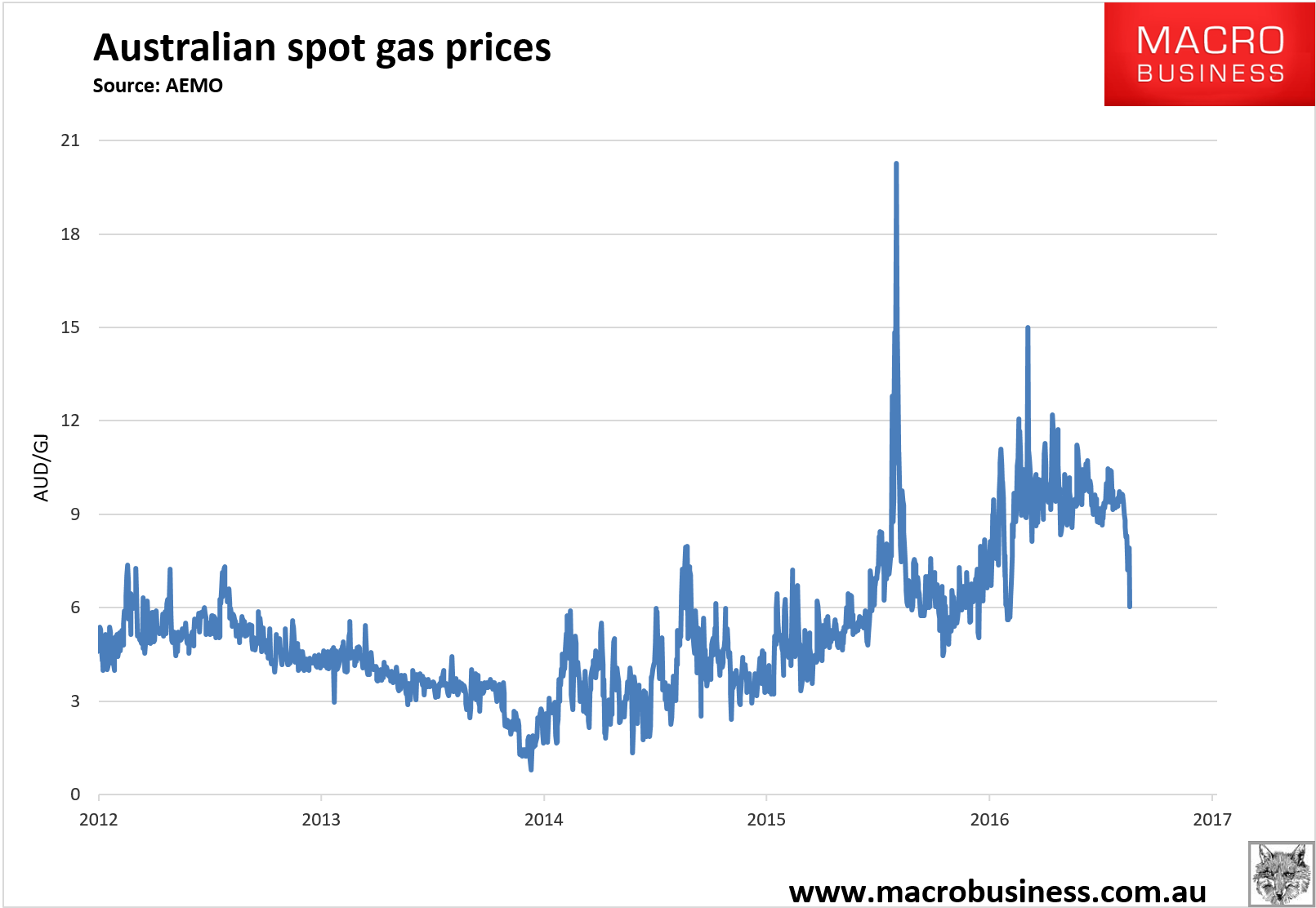

Those prices are basically export net back. Amusingly, spot markets have cratered in line with the prices:

Now contracts need to follow. Longer term price fixing is not the answer because we should be aiming for even lower prices than export net back. For that we need to see:

- larger domestic reservation;

- harsh lose it or lose it laws for reserves;

- a domestically-focused national gas company to force acquire or expropriate reserves as required and develop them in ways that assuage community anxiety about fracking, as well as benchmark prices in the market via mandated margins;

- tougher pipeline regulation.

Smash the cartel.