Via Citi’s chief global strategist, Matt King:

Markets seem optimistic that central bank plans to modestly reduce their support for markets in coming months can be achieved without disruption. We are not convinced.

When other people’s children behave badly, the temptation is to presume it’s something to do with the parents. But then one day, even if you managed to avoid the terrible twos, your very own adolescent comes downstairs to breakfast with a look that could curdle the milk in its carton, fails even to grunt a response to your cheery good morning, and makes straight for their mobile phone. It shortly becomes clear that the mere fact of your breathing is something they find deeply offensive. Nothing in their previous twelve-or-so years of almost uninterrupted sweetness gave any hint of this. Where on earth did you go wrong?

We imagine central bankers must feel similarly underappreciated every time markets fall into similar bouts of grumpiness. Like any parent, their initial instinct is to blame some sort of “external shock” – Eurozone sovereigns; weakness in emerging markets; a drop in oil prices; too much time spent hanging out with undesirable hedge-fund types. Like any parent, we think they would do well to focus less on eliminating potentially malign influences from the playground, and more on examining what in their own behaviour has left their offspring so fragile in the first place.

Misunderstandings over the effects of QE seem to us almost as large as the gap between how parents think their adolescents ought to feel and how they feel in practice. If you tell your teen you are going to reduce their screen time steadily down to zero because you are worried it’s affecting their behaviour, they do not simply sit there full of fond gratitude for the day you gave them a phone in the first place. At some point, they snap. This may not be justified, but a combination of habituated expectations and peer comparison means it is what happens in practice.

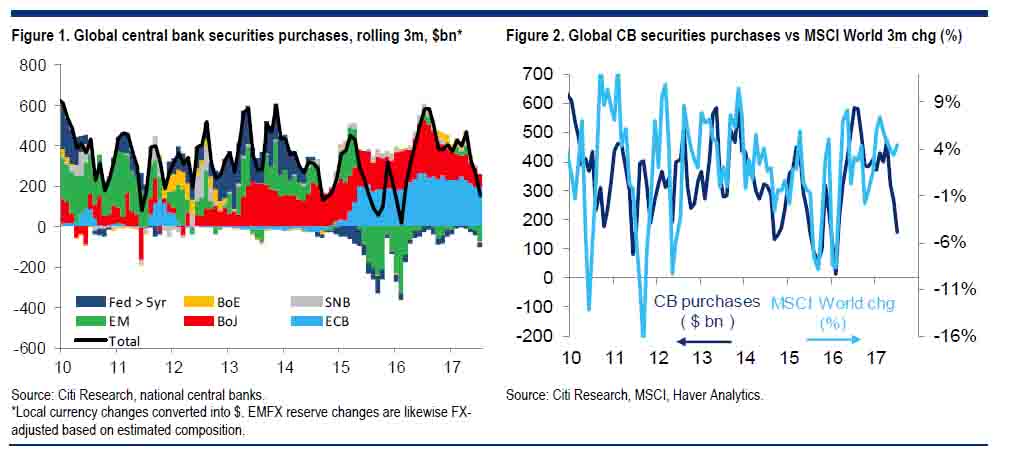

Central bankers’ ideas about QE seem likewise to owe more to an academic view of an ideal market than to the drivers of the price movements we see on our screens every day. Of all the tens of academic and central-bank papers assessing the impact of QE and other central bank liquidity injections, not one considers the (really rather obvious) approach which is our favourite: simply adding up the global total value of securities purchased by central banks each month (Figure 1) and then comparing it with the spread movement in credit or the price movement in equities (Figure 2).

- First, we argue that in assessing potential dependence on QE, central banks have largely been looking in the wrong places and at the wrong metrics: QE works globally and in terms of the flow of CB purchases, not in terms of the stock, and exhibits stronger relationships with risk assets than with government bonds.

- Second, we argue that the primary mechanism through which QE has had an impact is an enormous squeeze on the net supply available to absorb private investors’ savings – and that following QE1, relatively little has fed through to the real economy.

- Third, we argue that central banks would be able to make a smooth exit either if fundamentals had improved so as to justify risk assets’ lofty valuations, or if those valuations were not so lofty in the first place – but demonstrate that neither of these is the case.

- Finally we look at the conclusion we think central banks ought to draw – and contrast it with what seems likely in practice. It can be tough to do the right thing as a parent.

What happens in any market when you get steady net demand but zero net supply? Prices go up – regardless of the fundamentals. It sounds trite, but isn’t that exactly the pattern we’ve had across markets the past few years – be they govies or credit or equities or EM or real estate? 2015 was an exception, but of course that’s exactly the period when net supply to markets did increase thanks to the drop in EMFX reserves, meaning that money that was previously being crowded into risk assets ended up absorbing increased net supply in govies.

The … reason we think the transition will be difficult is simply that the starting valuations are so high already. It would be much easier for fundamentals to take over from central bank liquidity if the valuations across markets they needed to justify were not close to the highest we have ever seen. Credit spreads have basically been tighter only in 2007 (a level which many investors thought would never be revisited). Equity volatility is at its lowest since the 1950s. The cyclically-adjusted P/E ratio on the S&P has been higher only twice: at the height of the dot-com bubble in 2000, and in 1929. Those with long memories are already fretting about valuations across the board and warning investors against being greedy.

Many investors we speak to seem almost to have given up on valuation as a metric. Rather like real estate in London or New York or Hong Kong, they are resigned to it: it may look expensive on paper, but the price is what it is, and they buy anyway. Several told us they would rather lose lots of money in company with the rest of the market than underperform slightly in a continuing rally and then suffer a fall in assets under management as investors moved elsewhere.

Indeed, much has been written about the wave of money migrating away from active managers towards ETFs and passive index funds. In a market rallying with low single-name volatility, the only way an active manager can outperform is by throwing caution to the wind and ensuring that they are long risk relative to the index. If large numbers of managers adopt the same strategy, it will inevitably render the market vulnerable.

As a general rule, it is probably easier to reduce teens’ dependence on phones if you have not been through multiple iterations of previously trying to do so, only to give in when they then responded badly. Depending on how you add up the various episodes of global QE, in markets we are either still on iteration #1 (our global central bank liquidity metric has remained permanently positive since 2009), or conversely at least iteration #10 (three episodes of QE + Twist in the US, two distinct periods from the ECB, two from the BoE, and at least two prolonged ones from the BoJ). While at a global level there has never been any attempt to reduce the size of central banks’ securities holdings, on each occasion to date that even the flow of purchases has been reduced, first markets and then the economy have faltered to the point that central banks have given in and come back with more liquidity still.

If the historical relationships shown earlier were to hold, the relatively modest reductions planned by the Fed and likely from the ECB over the next year, coupled with the surprisingly large reduction we have already seen in purchases from the BoJ since the shift to yield targeting, would be consistent with IG credit spreads widening some 100bp and global equities selling off 30%.

Central banks have tended to ignore such risks – indeed, with Janet Yellen memorably stating she considers another financial crisis unlikely within our lifetimes – in part because they are less convinced of markets’ deviation from fundamentals than we are, but also in large part because their very definition of financial stability is one which is centred on the banking system. Stability is equated directly with leverage; if there is less leverage, there can be no risk to stability. The other factor which has helped valuations reach this point is that no one can quite imagine the specific sort of trouble the market will get itself into.

“What’s the catalyst?” we are often asked. Yet as with your children, if you wait until you can already see what sort of trouble they’re involved in, there’s a good chance you’re responding too late.

Our best guess is some combination of market sell-off associated with investor outflows. With some over $800bn having gone into fixed income mutual funds over the past five years, of which over $500bn having gone into some form of IG credit fund, it would not be especially surprising to see some combination of elevated valuations and higher real yields on deposits or other safe assets cause investors to decide to take profit. Yes, there might well be some form of external trigger (concerns about conflict with North Korea?), but this in itself might well be unrelated.

With debt/GDP at record high levels across most economies, it would be similarly unsurprising if negative wealth effects caused the resultant sell-off in risk assets to feed through to the real economy. Just because the rally in markets did not boost growth as much as central bankers were hoping does not mean that a sell-off would not affect it negatively: indeed, the fact that the benefits of market gains are narrowly distributed but losses might well be socialized means that increasing debt may well be automatically increasing the likelihood of an asymmetric reaction.

Note further that we are therefore fully expecting markets to move first, and the economic reaction to follow only thereafter. It is not that we see higher interest rates leading to a spike in corporate defaults leading to outflows and an investor sell-off; it is that default rates have been suppressed (relative to their historical relationship with GDP growth, and relative to corporate leverage) by the supply-demand imbalance and wave of investor inflows allowing corporates to roll maturities and abandon covenants, and that a reversal of those inflows – whatever its cause – might lead to the expectation of increased defaults thereafter.

This pattern may seem surprising, but of course it is exactly what happened in 2000 and 2007. It is not that a weakening economy precipitated a sell-off in the NASDAQ, or that a sudden recession dragged down the US housing market; it is that the bursting of each market bubble dragged down the economy. On each occasion it took a lower level of real interest rates to make investors change their minds about the assets they’d been buying and head for the safety of cash; on each occasion there was a higher level of debt across non-financial sectors.

Now, there is more debt still.

Quite right and precisely how the business cycle is likely to end. The question is when?

The key is credit markets. If CB tapering does drive up yields then the rest will takes care of itself as the risk-free rate rises, dragging down risk.

But why would yields rise? Lowflation is entrenched. Wage inflation is stalled. If CBs taper into that too fast (or at all) then markets are going to leap straight to the conclusion that it’s a policy error and buy bonds, driving yields down and, potentially, asset prices even higher. Add to this a slowing China and a Europe deflated by the tearaway EUR in 2018.

The MB fund is certainly positioned closer to the exit than it has been for much of 2017 but we’re still dancing and will keep doing so until we can see signs of actual inflation to underpin Fed tightening. That might come in the second half of next year as the oil market properly tightens.

For now, 2019 still looks a bigger risk to markets to us than does next year.

————————————————————————————————

Disclosure: I’m the strategist for the Macrobusiness Fund which is currently overweight international stocks. We also run an international equities fund. Both of these will benefit from a falling Australian dollar so I am definitely talking my own book.

Register your interest in the fund and we’ll be touch.