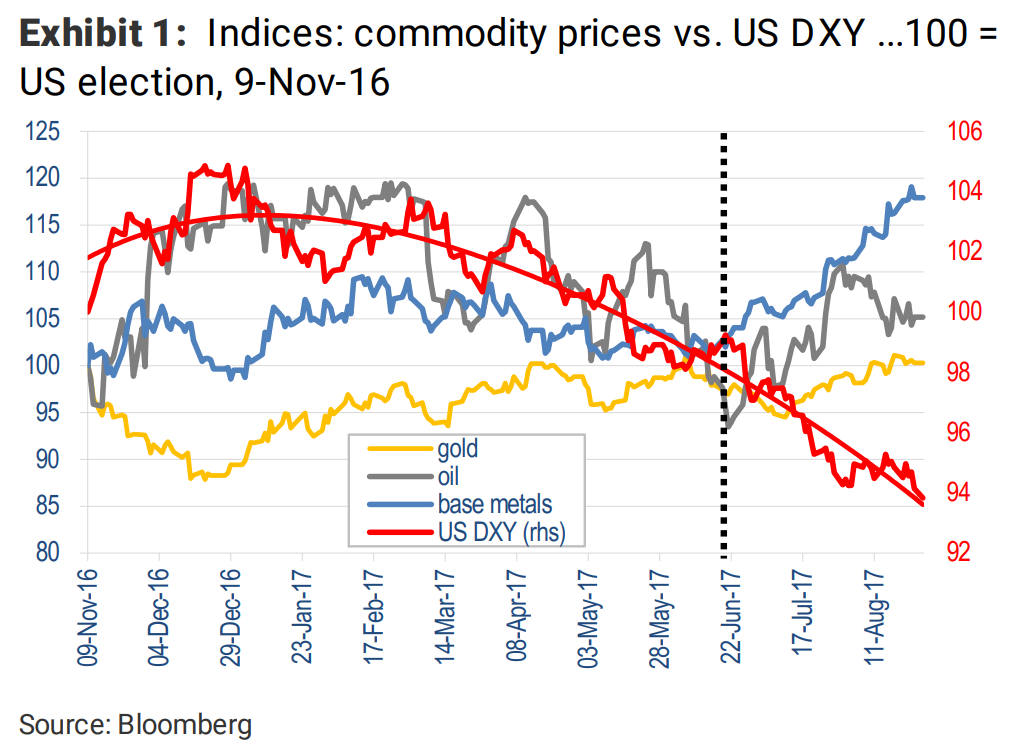

Since mid-June, commodity price performances have been dominated by a currency trade. So what events could terminate this driver? Currencytrade, mostly: Over the last 8-10 weeks, ithas been increasingly difficult for us to identify the fundamental basis of the general lift in commodity prices (now >15-40% since mid-June). Yes, prices for bulks (iron, coals) can probably be explained largely in terms of industry/market fundamentals (restocking, robust demand, profit-boosting industry reform). Similarly, restocking in zinc and nickel markets have helped lift prices of those trades. But similar scale price hikes for fundamentally weak trades like copper,aluminium and lead (guided by market signals; trade data) – revealed to us a universal exogenous driver:a USD-based currency shift.

Since Nov-16… In less than a year, we’ve seen several large price swings hit Commodity World. Two of them were USD-related. The US election (9-Nov-16) prompted a >10% general price rally over 4 weeks,as the USD strengthened. And right now, commodity prices are up again, but this time on USD weakness. Hang on, two price rallies, but on opposite USD shifts? True. It’s because each event’s riskbackdrop was different. Post-election, markets positioned for new inflation risk, on the promise of a US infra-build story (commodity fruitCAKE: popular questions, 09-Dec-16). Nine months later, that risk has probably disappeared, replaced by waning confidence/clarity in the US outlook + USD-selling – making US$-priced commodities ‘cheap’,given their unchanged global demand outlook (i.e. conventional inverse relationship restored). The fact that the DXY dropped below its Nov-16 level (Exhibit 1) in Jun-17, is probably one basis for Commodity World’s price rally since then.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.