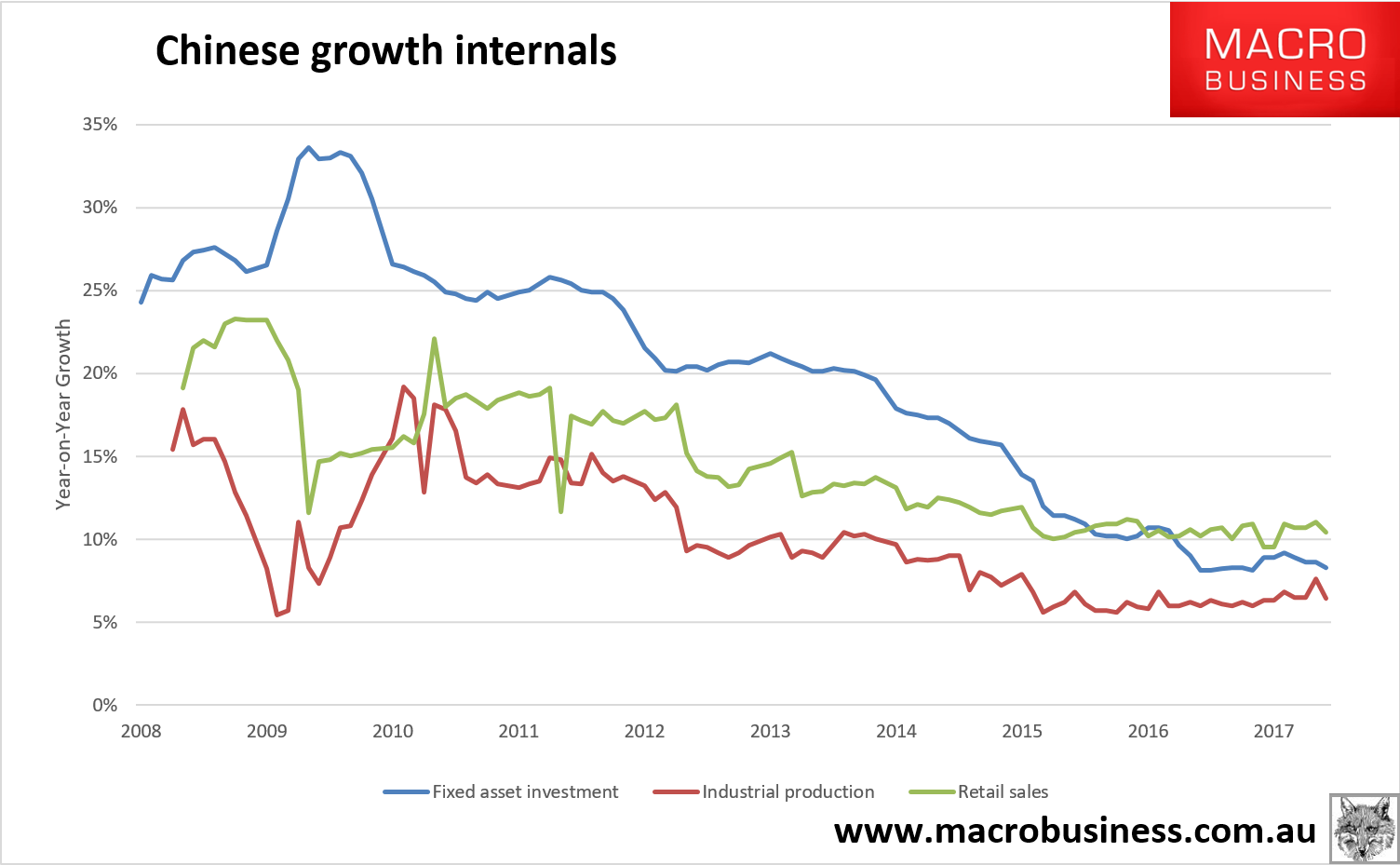

I’ve been waiting for it for while and now we get our first clear evidence of slowing growth arising from policy tightening. Chinese data for July has just missed across the board with Industrial production in at 6.4% vs 7.1% expected, fixed asset investment at 8.3% versus 8.6% expected and retail sales at 10.4% versus 11% expected:

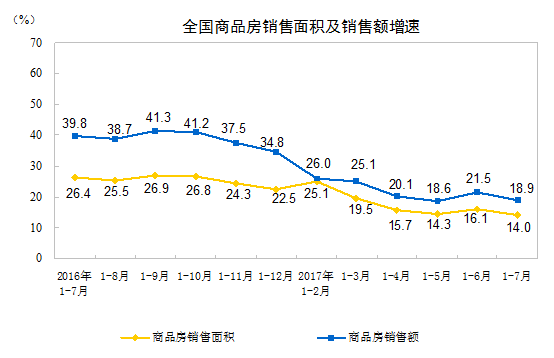

Some of this is clearly numberwang with give back after last month’s surge but there is stronger evidence of an ongoing trend slowing in construction. Floor area sales continue to decelerate year to date:

Advertisement

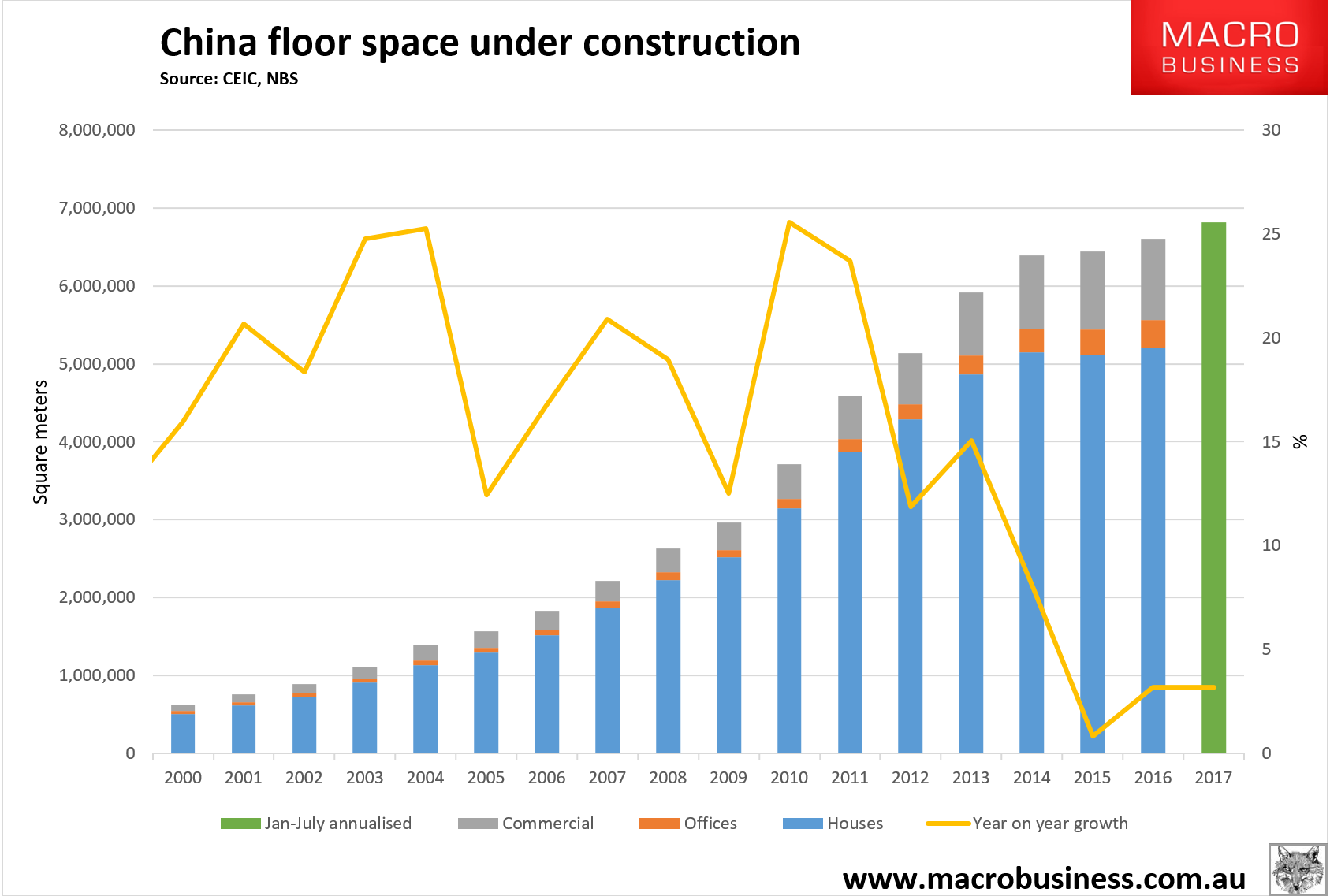

Total floor space under construction fell back to 3.2% year to date and ought to backtrack further over subsequent months: