Jonathon Tepper has a new name for the CBA:

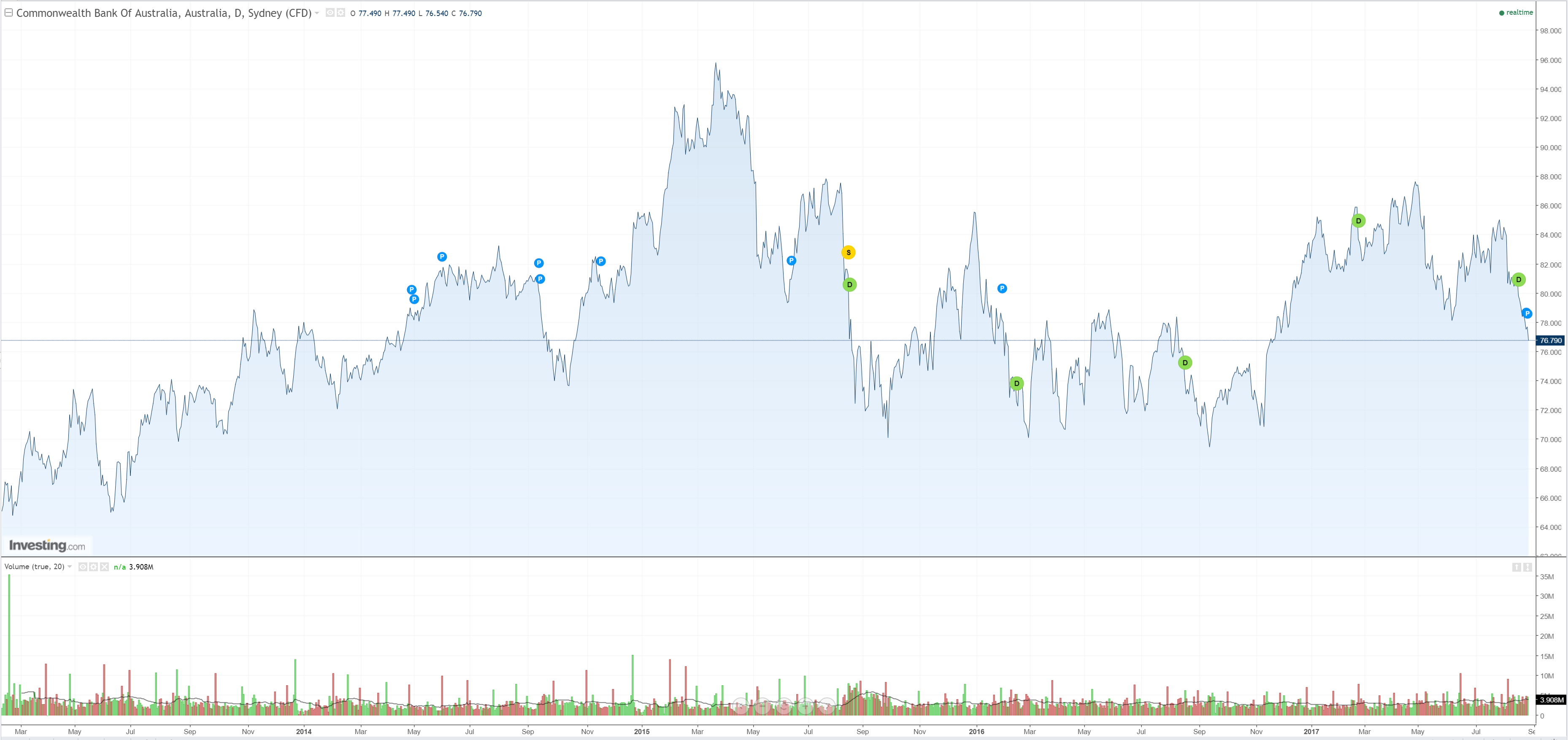

And investors are voting with their wallets, hitting new lows:

The chart still suggests no support right down to $70 and with the politics getting worse who knows? The under-performance is worsening but the whole sector appears increasingly tarnished:

Advertisement