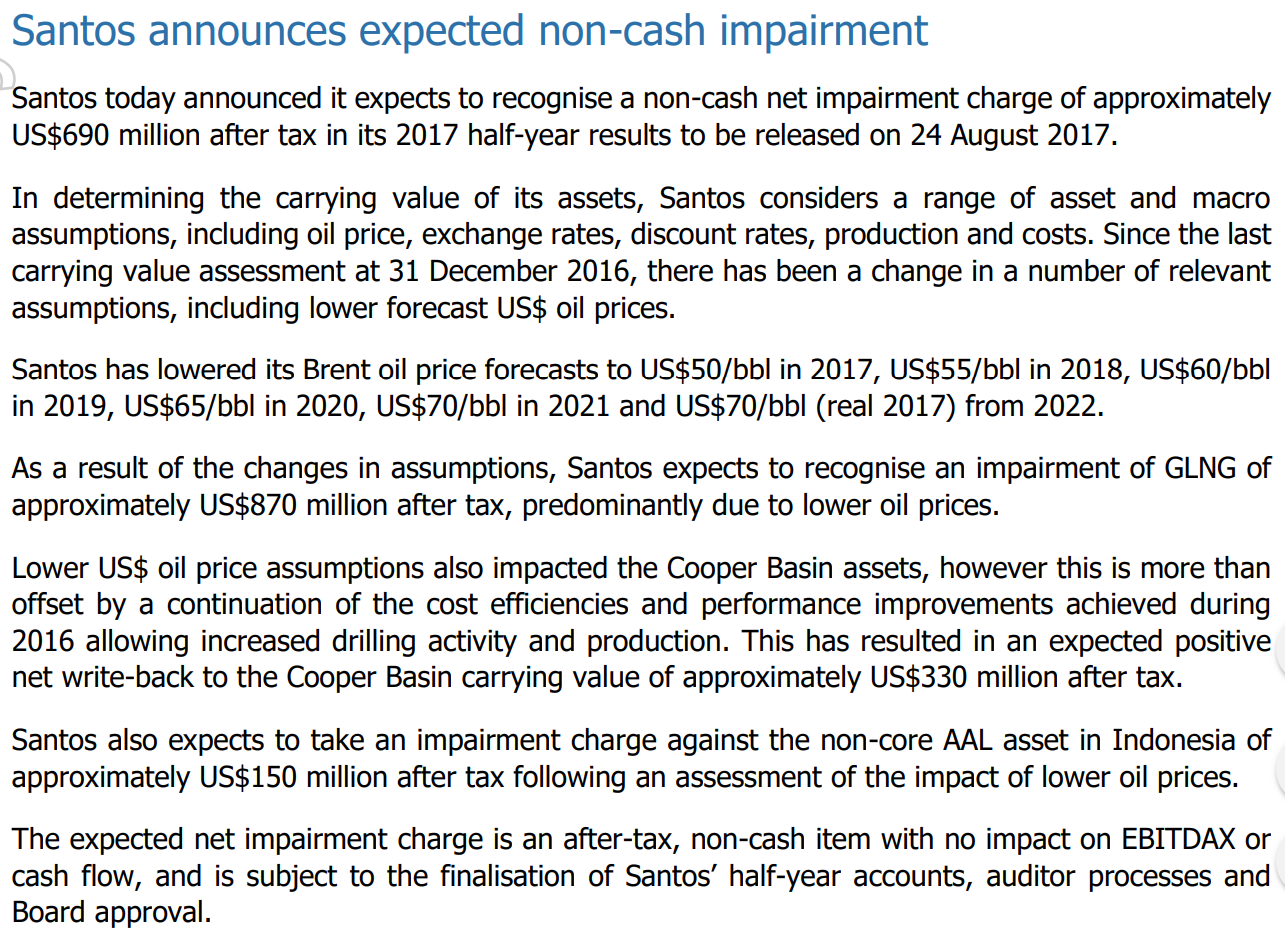

From Australia’s worst company, STO:

That’s nearly $3bn in write downs on GLNG now. It only owns 30% of the great $18.5bn elephantine failure so over half of the carrying value is now gone. Worry not, the rest will disappear in due course as those oil forecast are never met.

As it throws loss-making gas offshore at a bowel-shaking rate it continues to ravage the east coast economy to offset it, via UBS:

STO announces 15 PJ gas sale agreement with Pelican Point Power Station

The agreement will see gas from both GLNG and Santos sold to the 480 MW Pelican Point Power station owned by ENGIE in Adelaide, South Australia. Gas sales will commence in January 2018 and run for a couple of years. Pelican Point output has increased in recent months; at current generation levels it requires 20-24 PJ gas/annum.

Petronas and Kogas may make positive margin from the transaction

STO owns ~66% of gas production from the Cooper Basin, which we estimate will produce ~85PJ (gross) in 2018. With its forecast 56 PJ share of gas supplies, STO has a 50 PJ/annum contract with GLNG, known as the “Horizon” contract. We expect gas for Pelican Point to be derived from a combination of Horizon gas and STO residual equity gas. With oil prices remaining depressed and global LNG market oversupplied, we believe GLNG LNG buyers Petronas and Kogas may take advantage of low spot LNG prices to procure the cargoes they need and sell gas into the domestic market and generate a positive margin. As an example, at US$50/bbl oil price we estimate the LNG price ex-Gladstone to be US$7/mmbtu (equivalent to A$8.30/GJ). If GLNG has sold its gas to Engie at a similar price, there would be no economic impact to GLNG. If Petronas and Kogas then procure alternate LNG volumes for <US$7/mmbtu on the spot mkt (where prices are currently $5-5.50/mmbtu), they could effectively reduce their cost of supply.

Expect more GLNG deals to be done, but ADGSM uncertainty remains

GLNG is the only LNG project affected by the recently announced Australian Domestic Gas Security Mechanism (ADGSM). We expect GLNG to look to enter into more domestic gas sales where appropriate, though contract durations are expected to remain short. Does this remove any requirement for GLNG to supply gas into the domestic market if a shortfall is determined by the Resources Minister under the terms of the ADGSM? No. GLNG will remain a non-net contributor to the domestic market, so it will still have obligations under the terms of the ADGSM in our view. The Government has yet to make a decision on whether there will be a shortfall in 2018.

What is the point of the ADGSM if it doesn’t lower prices to at least export net back (and frankly, lower)? That’s US$5-6.

It has never been more clear how easy it is to rob credulous Australians blind.