In Friday’s opening statement to the House of Representatives Standing Committee on Economics, RBA Governor Phil Lowe argued that wages growth is likely to remain low both internationally and in Australia:

The reasons for the low growth in wages are complex. The fact that it is a common experience across countries suggests some global factors are at work. One possibility is that workers feel a heightened sense of potential competition; either from advances in technology or from international competition. More competition means less opportunity to put your price up. In the case of workers, it means slower rates of increase in wages. At the same time, many workers feel an increased sense of uncertainty and they feel less secure. This too is contributing to slow aggregate wage growth. The slow growth in wages is underpinning the low inflation outcomes in much of the world. It is possible that these effects will pass and that the normal relationship between tighter labour markets and higher wages will reappear. It is also possible that the current environment turns out to be quite persistent. How things turn out on this front is likely to have a significant bearing on the next stage in the global economic cycle…

There is an adjustment going on, with many people getting used to lower growth in their real wages. Many now see this as more than just a temporary development, with wage increases of 2 point something per cent now the norm. In my view, the underlying drivers of the slower wage growth in Australia are much the same as we are seeing overseas. At the same time, the household sector is also dealing with higher levels of debt relative to income. Higher electricity prices are also affecting household budgets. This all means that consumer spending behaviour is something we continue to watch carefully.

Then in the Q&A session, Phil Lowe reportedly argued that wages growth could reach 4%. From The Weekend AFR:

[Lowe] said it should be a reasonable expectation for wages growth to hit 4 per cent.

“We should be able to generate average hourly wage increases of three point something; if we did the right thing we could do 4 [per cent],” Dr Lowe told the committee of MPs. “But that’s up to you”.

…he told MPs wages growth of 4 per cent could be possible, which would be consistent with inflation of 2.5 per cent – which is the central bank’s target – and productivity growth of 1.5 per cent.

“It’s certainly plausible and it’s pretty close to our central scenario,” he said. “We’re expecting the unemployment rate to gradually drift down and as it has it as it drifts down there will be more pressure in the labour market and wage increases should pick up.

“I think there’s basic laws of supply and demand that still work and they work in the labour market”…

“Our staff estimate is still that full employment in Australia is probably around 5 per cent…and it’s going to take us, on our current forecast, quite some time to get to that…. certainly a couple of years.”

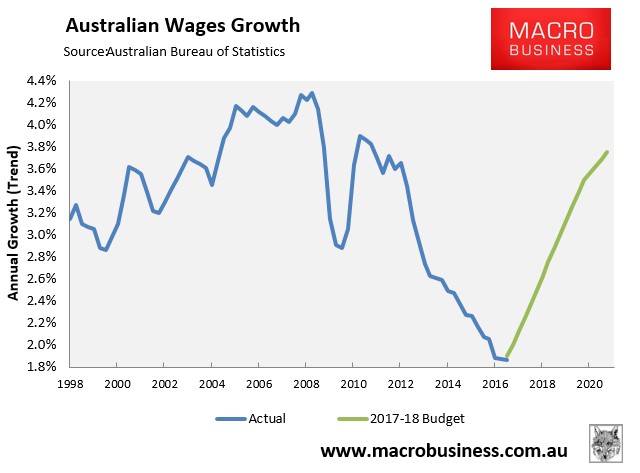

So after initially contradicting the May Budget’s forecast of a wages explosion (see next chart), now the forecast suddenly became realistic once more. Interesting.

In our view, the huge rebound in wages growth forecast in the Budget is very unlikely to occur.

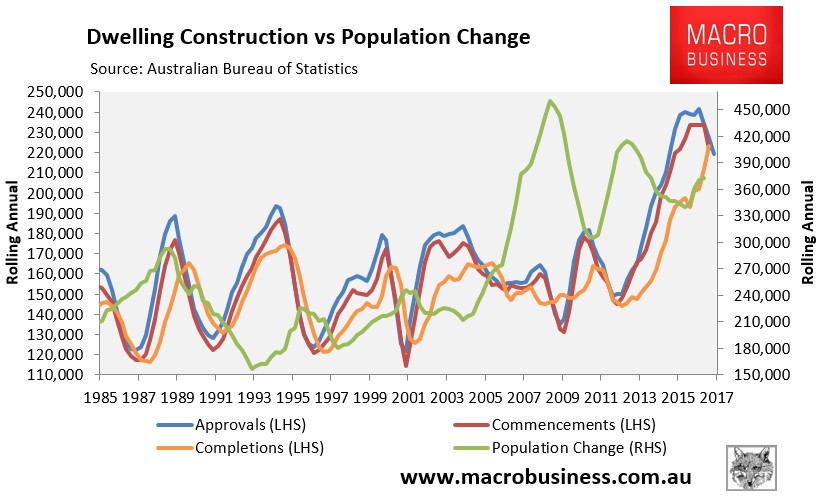

First, although the mining investment boom will have ended over the forward estimates, Australia is facing another bust from the unwinding of the epic dwelling construction boom, which will only be partly offset by increased infrastructure investment:

Second, there is a high likelihood that the giant housing bubbles in Sydney and Melbourne will finally correct over the forward estimates, possibly dragging down the other markets. If this happens, household savings will rise, and consumption and employment will fall, dragging down overall wages growth.

Remember, the large reduction in the savings rate since mid-2002 has helped support consumption and ergo jobs and wages growth. A rising savings ratio, which almost always happens amid a housing correction, would have the opposite effect.

Third, the terms-of-trade is likely to fall further than the Budget’s own (very optimistic) forecast of -2.75% in 2017-18 and -4.25% in 2018-19.

Finally, the Turnbull Government has stupidly chosen to maintain a record ‘skilled’ permanent migrant intake, as well as an appallingly low pay floor of $53,900 on temporary ‘skilled’ foreign workers, which will help to maintain spare capacity in the labour market, undermine workers’ pay and conditions, and dampen overall wages growth.

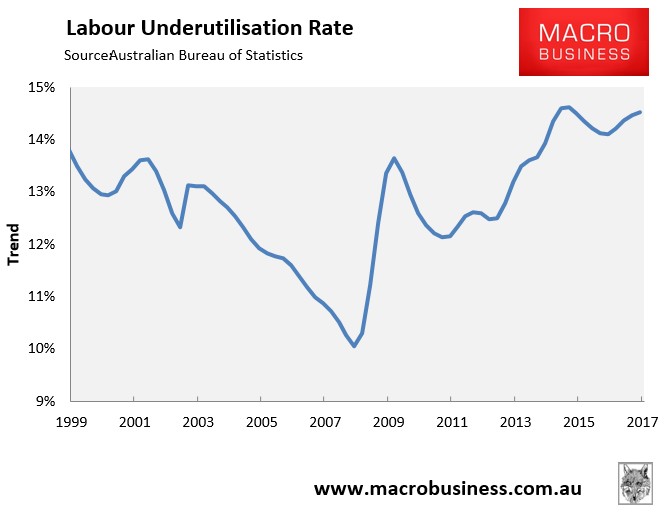

In any event, the unemployment rate is not the right metric to look at with respect to wages growth. Rather, it is the labour underutilisation rate, which is still stuck at a stubbornly high 14.5% (see next chart), suggesting the economy is operating below capacity and there is a negative output gap. This will need to come down materially to generate any significant wages growth.

{kind=link}