Below is the opening statement delivered today by RBA governor, Phil Lowe, to the House of Representatives Standing Committee on Economics [my emphasis]:

Chair

Members of the Committee

It is a pleasure to be here in Melbourne to explain our thinking on the Australian economy. My colleagues and I view this as an important part of the accountability process for the Reserve Bank. As usual, we look forward to answering your questions.

Since we last met in February, the global economy has strengthened. As a result, in most advanced economies, economic growth has been sufficient to push unemployment rates down further. A number of countries now have unemployment rates that are close to, or below, conventional estimates of full employment. Conditions have also improved in many emerging market economies, partly due to an increase in global trade. Commodity prices have mostly risen over recent months.

In China, growth has surprised on the upside a little of late. The main challenge there continues to be containing the risks from the build-up of debt, while at the same time keeping growth on a steady path. This remains a work in progress. Economic growth has also picked up in the euro area, with conditions the best they have been since the euro area crisis in 2012. On the other side of the ledger, though, in the United States the earlier optimism that the new administration’s fiscal policies would spur stronger growth has dissipated.

Since we last met, the Federal Reserve has increased interest rates twice and the policy rate in the United States now stands at 1¼ per cent. Despite this, the US dollar has depreciated in global markets, which has surprised many observers. The Bank of Canada has also increased its interest rate, reversing some of the policy insurance it took out earlier when the outlook was less positive. Elsewhere, there is no longer an expectation that central banks will announce yet further monetary stimulus and some central banks have indicated that they may scale back some of the current stimulus if conditions continue to improve. This is a positive development.

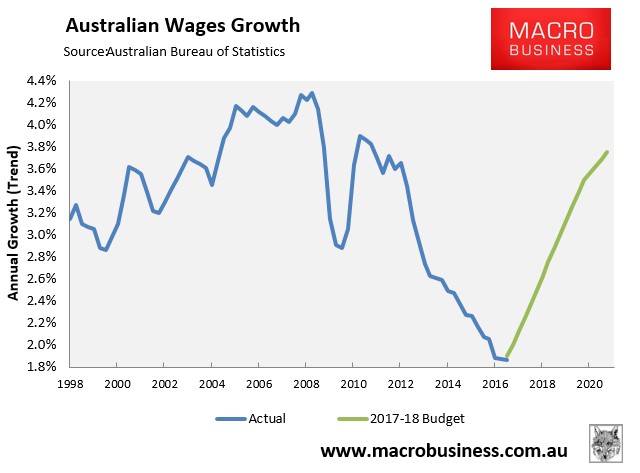

As well as this change in the outlook for global monetary policy, another prominent theme in discussions of the global economy of late has been the slow growth in wages. Despite the success that a number of countries have had in generating jobs, wage growth remains low. This is contributing to a continuation of inflation rates that are below target in most advanced economies, although in headline terms they are mostly higher than a year ago.

The reasons for the low growth in wages are complex. The fact that it is a common experience across countries suggests some global factors are at work. One possibility is that workers feel a heightened sense of potential competition; either from advances in technology or from international competition. More competition means less opportunity to put your price up. In the case of workers, it means slower rates of increase in wages. At the same time, many workers feel an increased sense of uncertainty and they feel less secure. This too is contributing to slow aggregate wage growth. The slow growth in wages is underpinning the low inflation outcomes in much of the world. It is possible that these effects will pass and that the normal relationship between tighter labour markets and higher wages will reappear. It is also possible that the current environment turns out to be quite persistent. How things turn out on this front is likely to have a significant bearing on the next stage in the global economic cycle.

I would now like to turn to the Australian economy.

The most recent GDP data are quite dated now and are for the March quarter. They showed growth weaker than we had earlier expected. This, however, partly reflected temporary factors, including weather-related disruptions to production and quarter-to-quarter volatility in resource exports. Since then, the recent run of data has been consistent with a pick-up in growth. There has been an improvement in survey-based measures of business conditions and capacity utilisation has increased. Employment growth has also picked up and retail spending has been a bit stronger of late. Financial conditions remain favourable, with interest rates remaining low and banks willing to lend.

The Reserve Bank released its latest forecasts for the economy last Friday. In summary, our central scenario is for GDP to grow at an average of around 3 per cent over the next couple of years. This would be better than we have seen for some time. The transition to lower levels of mining investment following the mining investment boom is now almost complete. This means that falling levels of mining investment will not be a drag on the economy for much longer. Instead, with some large LNG projects reaching completion soon, GDP growth is expected to be boosted by a lift in LNG exports.

For some time we have been looking for a strong pick-up in private business investment outside the resources sector. This is taking longer to occur than expected. While we do see positive signs in parts of the economy, many firms still show some reluctance to commit to significant investment, often citing a range of uncertainties. It is possible that this reluctance will continue for a while yet. But it is also possible that the improvement in business conditions that we have seen will give firms the confidence to invest more, after a period of under-investment. We have incorporated a middle path into our own forecasts.

On the investment front a positive development has been an increase in spending on public infrastructure, particularly transport. This is directly supporting aggregate demand and is having some positive spin-offs elsewhere in the economy. It is also addressing earlier under-investment and should improve the supply side of the economy.

Another factor that has a bearing on the outlook is the behaviour of households. There is an adjustment going on, with many people getting used to lower growth in their real wages. Many now see this as more than just a temporary development, with wage increases of 2 point something per cent now the norm. In my view, the underlying drivers of the slower wage growth in Australia are much the same as we are seeing overseas. At the same time, the household sector is also dealing with higher levels of debt relative to income. Higher electricity prices are also affecting household budgets. This all means that consumer spending behaviour is something we continue to watch carefully.

One positive development in this area over recent times has been a pick-up in employment growth, which should boost incomes. A little while ago, employment growth was on the weak side and the unemployment rate had ticked up. In contrast, in recent months employment growth has been noticeably stronger and more people have entered the labour force. Encouragingly, the gain in jobs is evident in all states, including in Western Australia and Queensland, which have been adjusting to lower levels of mining investment. Our central scenario is for the national unemployment rate to move gradually lower, although it is likely to be some time before we reach what could be considered full employment in Australia.

Another area that we continue to watch closely is the housing market. Conditions continue to vary significantly across the country. The Melbourne and Sydney markets have been much stronger than elsewhere. There are some signs of slowing in these two markets, although these signs are not yet definitive. In some markets, a large increase in the supply of new dwellings is expected over the next year as new buildings are completed. This increase in supply is expected to have an effect on prices.

In terms of inflation, when we last met I suggested that inflation was at a trough and was expected to increase gradually. Recent outcomes have been consistent with this. Both headline and underlying inflation have risen and are currently running a little under 2 per cent. Inflation is likely to continue to move higher gradually, with the headline measure boosted by higher prices for tobacco, electricity and gas. A consideration working in the other direction is increased competition in the retail sector, particularly from new entrants. This is likely to continue for a while yet. The low wage increases are also contributing to the subdued inflation outcomes.

One factor that is influencing the outlook for both economic growth and inflation is the exchange rate. The recent appreciation means lower prices for imported goods and it is weighing on the outlook for domestic output and employment. Further appreciation, all else constant, would cause a slower pick-up in inflation and slower progress in reducing unemployment.

Since August last year, the Reserve Bank Board has held the cash rate steady at 1.5 per cent. This setting of monetary policy is supporting employment growth and a return of inflation to around its average rate of the past couple of decades. The Board is seeking to do this in a way that does not add to the medium-term balance-sheet risks facing the economy. It has been conscious that a balance needs to be struck between the benefits of monetary stimulus and the medium-term risks associated with rising levels of debt relative to our incomes.

As a result, the Board has been prepared to be patient. The fact that the unemployment rate has been broadly steady has allowed us this patience. We have preferred a prudent approach, which is most likely to promote both macroeconomic and financial stability consistent with the medium-term inflation target.

The Reserve Bank has continued to work closely with APRA through the Council of Financial Regulators to address financial risks. Our assessment is that the various supervisory measures – including a focus on lending standards and placing limits on investor and interest-only lending – will work to strengthen household balance sheets over time. Financial institutions have adjusted to the new requirements and these requirements are contributing to the resilience of the system as a whole.

I would now like to briefly mention three matters related to the Bank’s other functions that may be of interest to the Committee.

The first is that the banking industry is in the final stretch of developing the New Payments Platform (NPP). As we have spoken about previously, this new payments infrastructure will provide Australians with the ability to make real-time, information-rich payments on a 24/7 basis. It will also make addressing of payments much simpler, using email addresses and mobile phone numbers, rather than BSB and account numbers. It has been a complex project and the Reserve Bank has played an important role, both in policy terms and as a provider of a key part of the infrastructure. As the government’s bank, the Reserve Bank will also make the new payment capabilities available to its government banking customers. The new system is expected to commence processing payments later this year. It is likely to start off small and gradually ramp up next year as financial institutions gain experience with a new way of operating 24/7.

The second matter is that when we met in February, I said that I had commissioned an external review of the efficiency of the Bank’s operations. That review has now been completed. It concluded that our support areas were functioning well and assisted the achievement of the Bank’s important public policy objectives. At the same time, it suggested some areas for us to focus on. One was the development of a shared internal services centre to drive continuous improvement. Another was further evolution in our approach to IT as some of our major IT-related projects come to an end. These projects are in the banking and payments areas and have been undertaken in the national interest. As these projects wind down we are looking to make sure that the size and structure of our IT function remains appropriate. More broadly, as some of these projects finish this year, the Bank’s overall staff numbers will decline.

Finally, I would like to take this opportunity to announce that we will be releasing the new $10 banknote next month, on 20 September. Printing of the new notes has been completed at our printing works in outer Melbourne. The new notes contain the same world-leading security features as the new $5 note that we issued last September, including the clear top-to-bottom window, and the tactile feature so that it can be recognised by vision-impaired members of the community. Construction has also recently been completed on our new banknote storage and processing facility at Craigieburn, which will soon commence operations.

Thank you. My colleagues and I are here to answer your questions.

The RBA certainly doesn’t sound too confident that the Budget’s forecast wages explosion will materialise: