The Turnbull Government is optimistic that its proposed 0.5% increase in the Medicare levy will be passed by the Senate. The bill will be put before the upper house later today, although a vote is unlikely before September. The Labor Opposition is pushing for the increased levy to be restricted to people whose annual income exceeds $87,000, whereas the Government hopes to secure the support of crossbenchers. From The Australian:

…the government has been quietly negotiating with crossbenchers to sideline Labor…

Mr Morrison has dismissed the Labor argument for a $87,000 threshold for the tax by pointing to the approach taken with similar measures in the past, including four years ago when former prime minister Julia Gillard and Mr Shorten backed a 0.5 per cent increase for all workers to fund the disability scheme when Labor was in power.

A senior government source told The Australian the government was putting the package to the parliament because it was happy to debate the policy, and the need to fund the NDIS, over the objections from Labor.

Mr Morrison has already introduced safeguards in law to ensure the Medicare Levy will be waived for individuals earning up to $21,655 a year, families earning up to $36,541 or retired couples who qualify for a seniors’ tax offset and earn up to $47,670 a year. The bill also expands the “phase-in” rules that apply the Medicare Levy at a concessional rate for millions of workers depending on whether they have children. As an example, a family with two children and a taxable income of up to $43,253 will not pay the levy, an increase from the previous threshold of $42,613.

The increase in the exemptions will cost the budget $180 million over four years and add about 100,000 people to the nine million who are exempt from the Medicare Levy.

The increase in the levy will be $350 a year or about $1 a day for a worker earning $70,000.

While I have no issue with raising funding to pay for growing health expenditure, I do not believe that raising the Medicare Levy is the best or fairest way to do so.

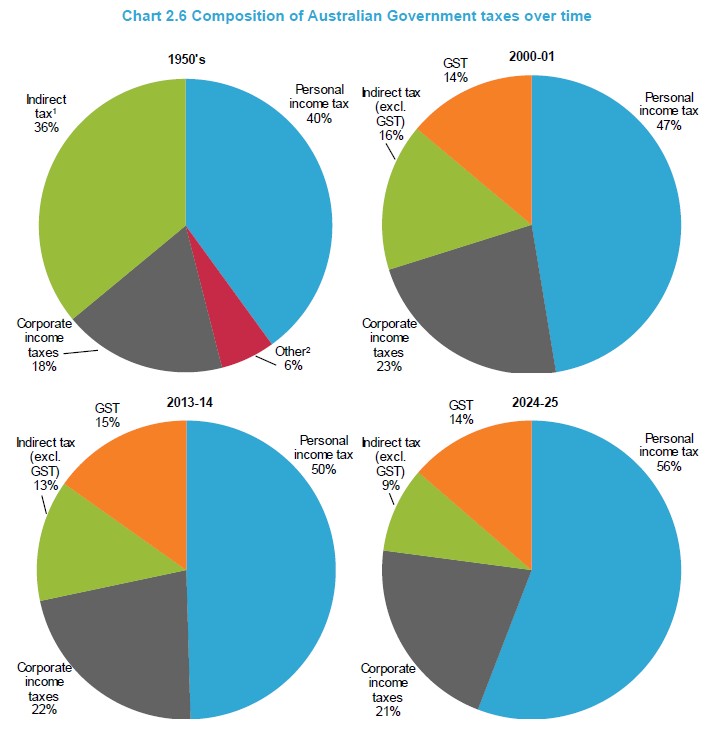

Australia’s tax system is already too heavily reliant on working Australians, with 50% of the Australian Government’s tax take already coming from personal income taxes. Worse, under current arrangements, this share is forecast to rise to 56% in the decade ahead on the back of bracket creep (aka “fiscal drag”), as inflation pushes workers into higher tax thresholds (see next chart).

Raising the Medicare Levy would effectively worsen the income tax burden even further, punishing working Australians.

It would also have deleterious impacts from an inter-generational perspective, since it would be younger Australians who are called upon to fund public services for their retired parent’s and grandparent’s, who tend to be far wealthier than they are.

As revealed by the latest Census, more than 80% of retirees own their homes, which are conveniently excluded from the assets test to qualify for the Aged Pension (see next chart).

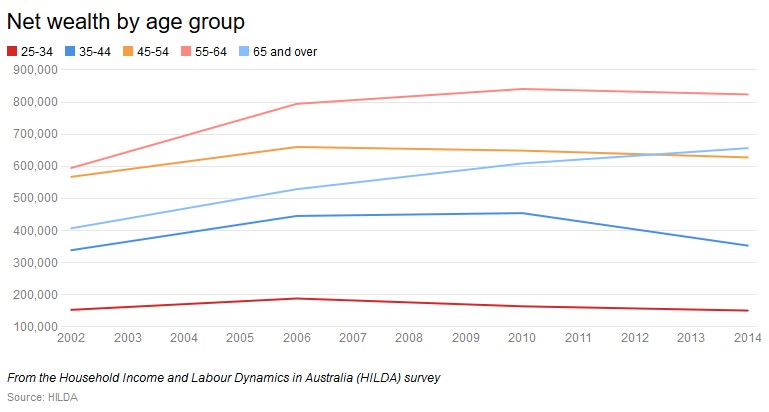

These 80%-plus of retirees have also enjoyed massive windfall gains in wealth, thanks to the mammoth surge in Australian home values over the past 20 year (see next chart).

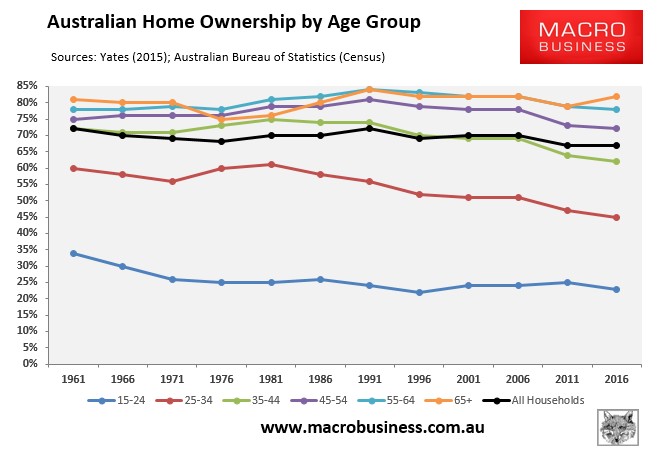

And this surge in retiree housing wealth has, of course, come at the direct expense of their grand children, who are now either locked-out of housing altogether (see above chart), or are required to undergo a lifetime of debt servitude in order to afford a home.

Rather than raising the Medicare Levy, which would unduly burden younger working Australians, a better approach would be to raise the required health funding via a combination of other measures, for example:

- Abolishing the planned cut to the company tax rate, from 30% to 25%.

- Further tightening tax concessions, such as negative gearing, the CGT discount, and fringe benefits on company cars.

- Abolishing the private health insurance rebate, which let’s face it is inflationary and hasn’t reduced pressure on public hospitals.

- Tightening means testing of the Aged Pension by including one’s principal place of residence in the assets test, supported by an expansion to the Pension Loans Scheme, so that asset-rich retirees can continue to receive income support via a government-run reverse mortgage.

- Cracking down on discretionary trusts and private companies, which allow relatively well-off individuals to avoid tax by diverting and ‘sheltering’ their income or income producing assets.

- Implementing a broad-based Commonwealth land tax.

What Australia should not do is simply raise the tax burden on younger working Australians, while the key beneficiaries of government programs (via the Aged Pension and health and aged care expenditure) pay minimal taxes on their income and enjoy massive untaxed wealth.

Expanding health funding is fine. However, it should be done via broadening the tax system and eliminating waste in an efficient and equitable manner, so that everyone with means shares the burden.