by Chris Becker

Easing tensions on the Korean peninsula have caused stock markets to rally and a retreat from key safe havens like Yen, which lifted Japanese stocks for the first time this week. Gold prices remain elevated while a small selloff in local bonds continues as iron ore prices also retreat.

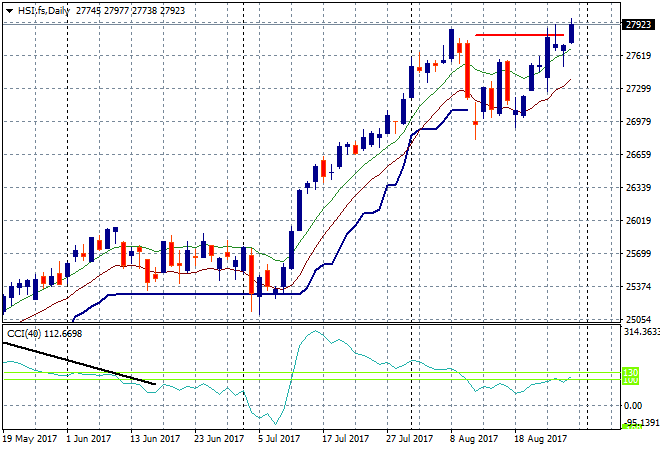

In mainland China the Shanghai Composite has put in another scratch session to be down only a few points at 3363 extending its pause here after the big breakout recently. The Hong Kong based Hang Seng Index is doing much better, up nearly 1% and closing just above 28000 points. This takes it past its previous daily high and lets the door wide open for a further advance:

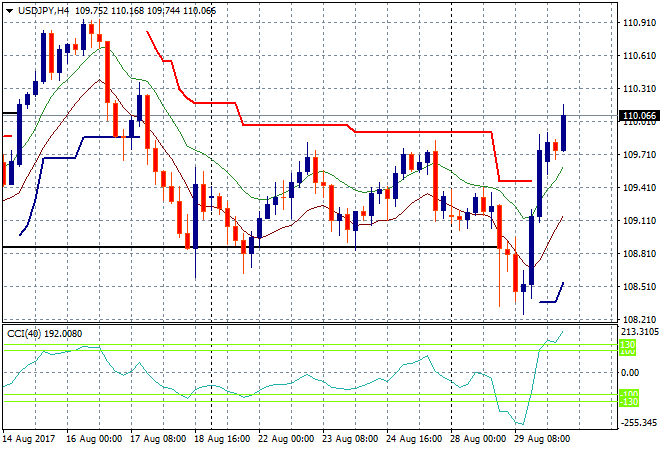

Japanese stocks finally rallied on the weaker Yen. The Nikkei lifted nearly 0.75% to close at 19504 points, still remaining below the very firm resistance at the 20,000 point level but at least making a start at a recovery. The USDJPY pair has broken above the 110 handle to make a new two week high in a very swift move here, with the next target at 110.90:

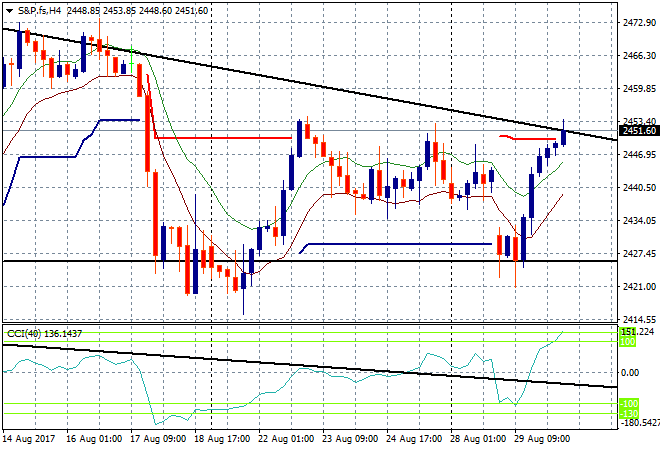

S&P futures are up following the Asian rally, but tonights GDP print has to be on expectations as nerves are still stretched thin:

The ASX200 has put in a scratch session to finish where it started the day at 5663 points as the 200 day moving average level remains an anchor on any further advances.

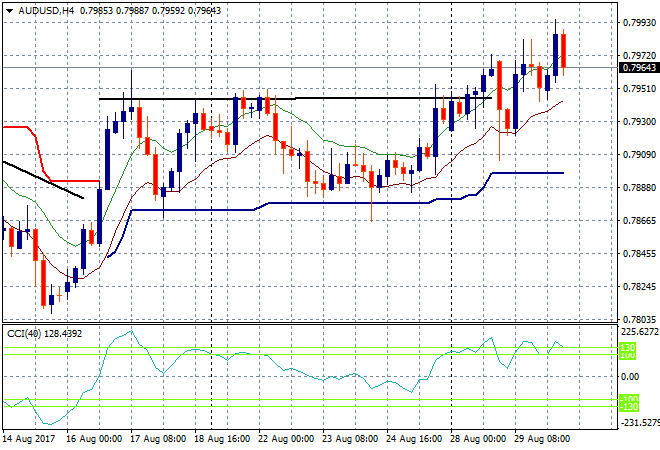

The Aussie dollar has pushed higher on the back of the partial GDP news, almost reaching the 80 handle against USD, before settling at 79.60 going into the London session. Former resistance is now support here at 79.40:

The data calendar has two important and currency sensitive releases tonight, first the German CPI print for August, then US 2Q GDP.