Ah, Jess Irvine:

The team at ABC’s Four Corners assembled a thrilling package about the Australian property boom last Monday.

It came replete with forecast of the “perfect storm” for property and an inevitable popping of the property “bubble”.

…Absent a rise in the jobless rate, which has been falling recently, it’s hard to see where the trigger for forced property sales would come from. In times of price weakness, home owners tend to just sit on their properties, keeping volumes low and price falls capped.

Australia has never seen a precipitous fall in house prices, as has occurred overseas. Price booms tend to be followed by period of price stagnation, rather than falls. Australian banks have never been willing to offer “no recourse” loans as in many other countries, like the US. If a mortgage holder can’t pay, their house is repossessed and the bank recoups its money. In other countries, many borrowers can just walk away, and do.

Australian mortgage holders, by comparison, will keep paying the mortgage until it is absolutely impossible.

The other unique feature of our housing market is the degree to which people have variable interest rate loans. This makes us incredibly sensitive to changes in interest rates. Indeed, some of us make a very good living feeding Australian’s obsession with interest rates and house prices.

This sensitivity to interest rate changes makes monetary policy – the setting of borrowing rates by the central bank – a potent tool of economic management.

Perhaps the biggest reason to believe Australia’s property boom won’t go spectacularly bust is that the Reserve Bank won’t let it happen.

There is good reason to believe that future interest rates will remain lower than they have in the past.

OK, so, as we know know, Ireland has “no recourse” home loans more draconian than Australia’s:

It didn’t help much. But, as we know, when it comes to property bubbles and busts, Domainfax has its favourites.

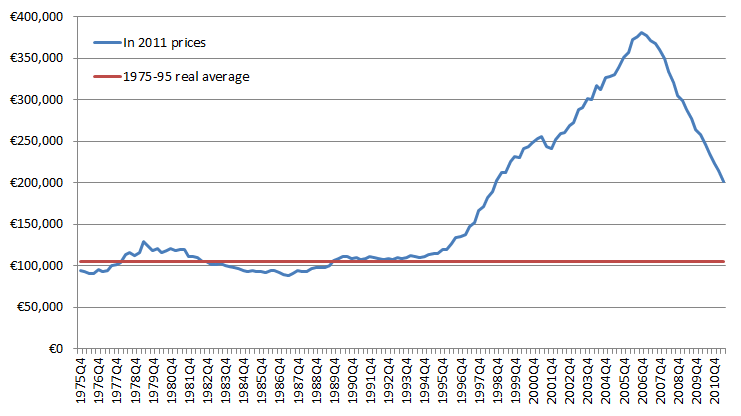

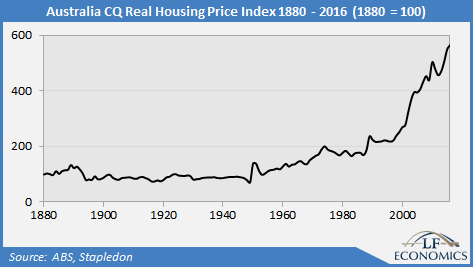

Australia has had some decent cyclical busts with large precipitous falls in the late eighties in Sydney and Melbourne and nationally in 1890s. The Sydney 2003 mortgage belt bust was also pretty sizeable. Though it is true that we’ve more often had slow melts, including the one that lasted 70 years after the 1890s crash:

The tail looks a bit like the Irish chart, no?

As for the RBA, Jess is absolutely right. It will fight any crash all the way down, as it should. But how far down it that? At 1.5% it only has one percent of cuts left versus 5.75% of cuts post GFC. And if property price falls require those cuts then you can be sure that bank funding costs will be rising and banks keeping half of those cuts for themselves. Indeed, in the worst case, banks will be hiking when the RBA runs out of cuts:

Nor does Jess note that regulators have clearly identified the bubble now and are tightening macroprudentially to stop it. An absence of hikes does not equal higher prices any longer.

But, as we know, when it comes to property bubbles and busts, Domainfax has its favourites.

This is all a sad and sorry ritual. Jess writes her lies, I point them out. Let’s leave the rest to Irvine’s co-commentator who nicely fingers what this article is really about. From Ross Gittins:

What too few people realise is how much of government spending goes not directly into the pockets of voting punters, but indirectly via businesses big and small: medical specialists, chemists, drug companies, private health funds, private schools, universities fixated by their ranking on global league tables, businesses chasing every subsidy they can get, not to mention international arms suppliers.

The budget, in other words, is positively crawling with vested interests lobbying to protect and increase their cut of taxpayers’ money.

A government that can’t control all this potential business rent-seeking – isn’t perpetually demanding better value for taxpayers; perpetually testing for effectiveness – is unlikely to have much success in limiting the growth in its spending.

Put Jess Irvine and property policy-dependent Domainfax right at the top that list of rent-seekers.