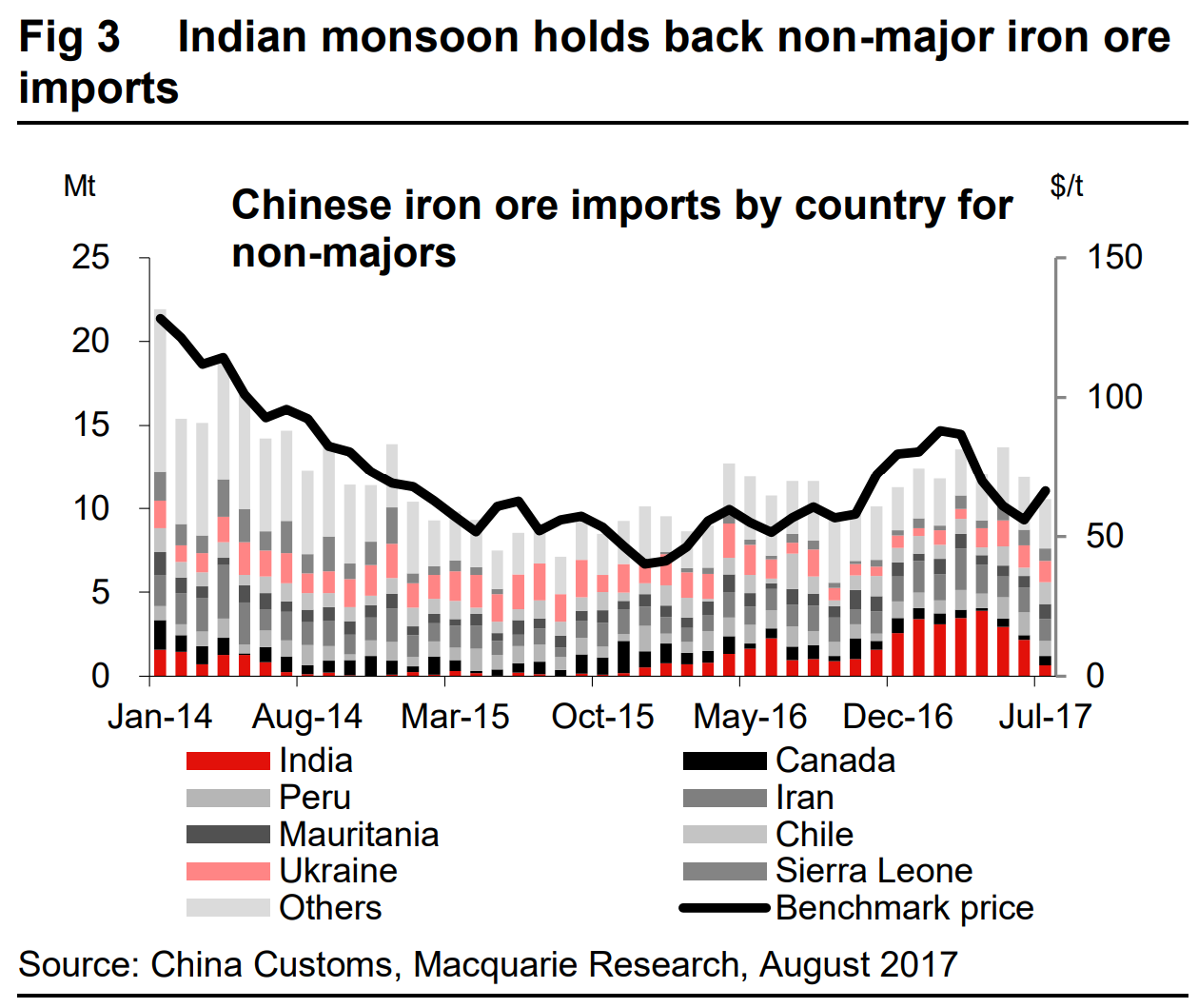

Non-major iron ore slips on Indian summer: Iron ore numbers reveal a marked slump in nonmajor, seaborne supply as India remains largely out of the seaborne market. Despite a sharp uptick in prices during July, Chinese imports from non-major supply, a very price elastic segment of the market, fell to 10.3 Mt, the lowest this year. India is the culprit: exports to China totalled only 0.66Mt in July – equivalent to an annualised run rate of only 7.7Mt/y, compared to more than the 40Mt/y rate achieved in Q1. The ongoing monsoon season means that a weak print from India was always expected, but the July number came in below our expectations down 33% YoY. We continue to expect a strong comeback in the coming months: at current spot prices and Fe discounts, exports from Goa breakeven around $65/t and are cash positive. This should provide miners with a strong incentive to resume exports once the monsoon season ends in September.

Goan ore is much cheaper than that. But the argument is right.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.