Prime Minister Malcolm Turnbull says South Australia’s energy plan is an “experiment” that should have been conducted privately.

“You really have in South Australia, of course, been subjected to an experiment by (Premier) Jay Weatherill. People really should conduct these experiments, as dangerous as that, privately somewhere in expert company rather than inflicting it on an entire state,” the prime minister said.

Mr Turnbull said Labor’s approach to energy was a combination of ideology and politics, compared to the Liberal focus on economic and engineering. “But on reflection, I think I’ve been too kind to them. It’s actually ideology and idiocy in equal measures,” he added.

Meanwhile, the Weatherill government is finalising contracts worth more than $111 million for diesel generators to prevent blackouts this summer.

…Nine generators, currently being shipped from Europe to South Australia, will run on diesel at two sites to provide up to 276 megawatts of power for the next two summers. They will then be moved to one site and be switched to gas as a permanent power plant.

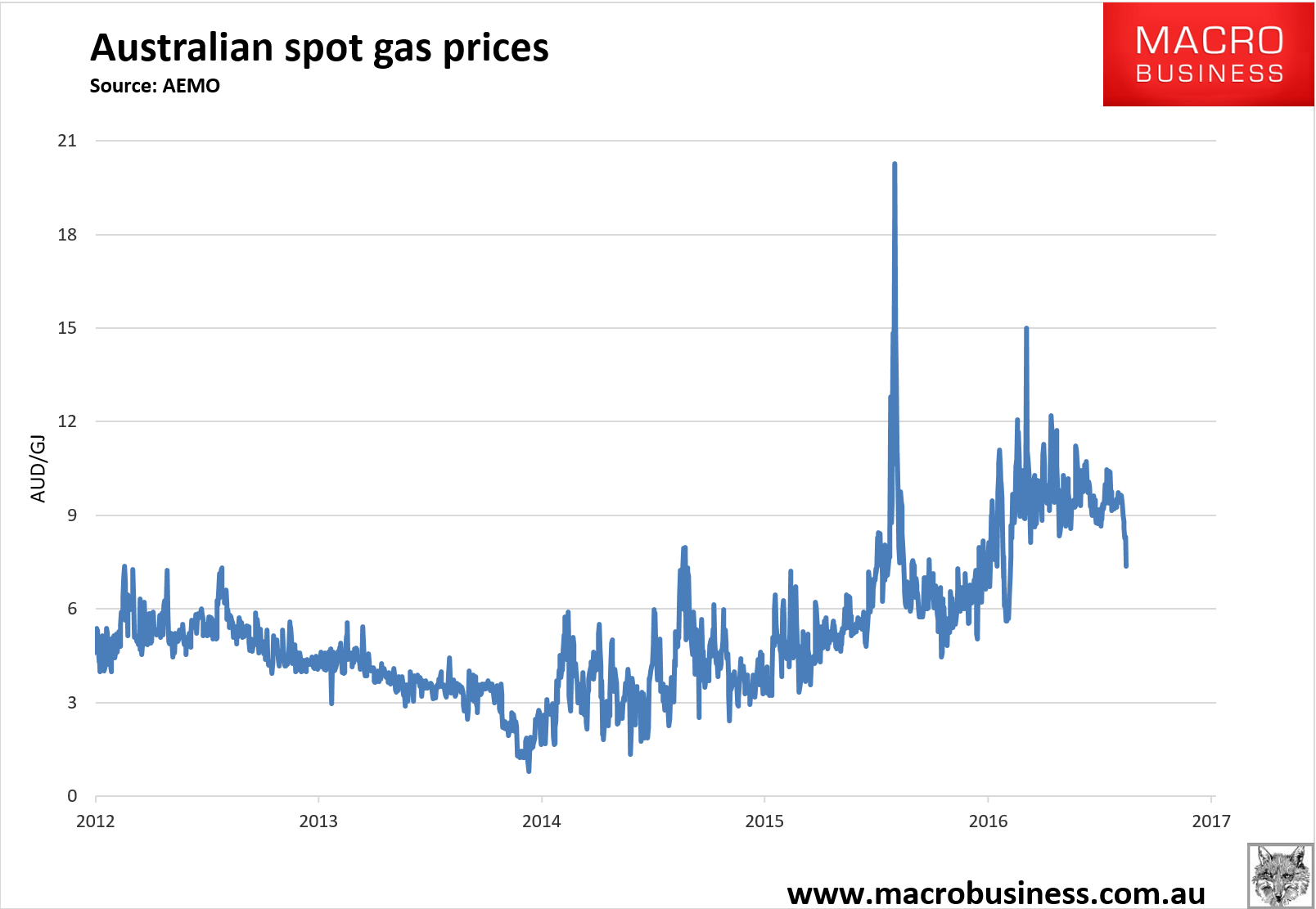

One more time for the dummies. Power prices are not high in SA because of renewables. They are are high owing to the east coast gas crisis.

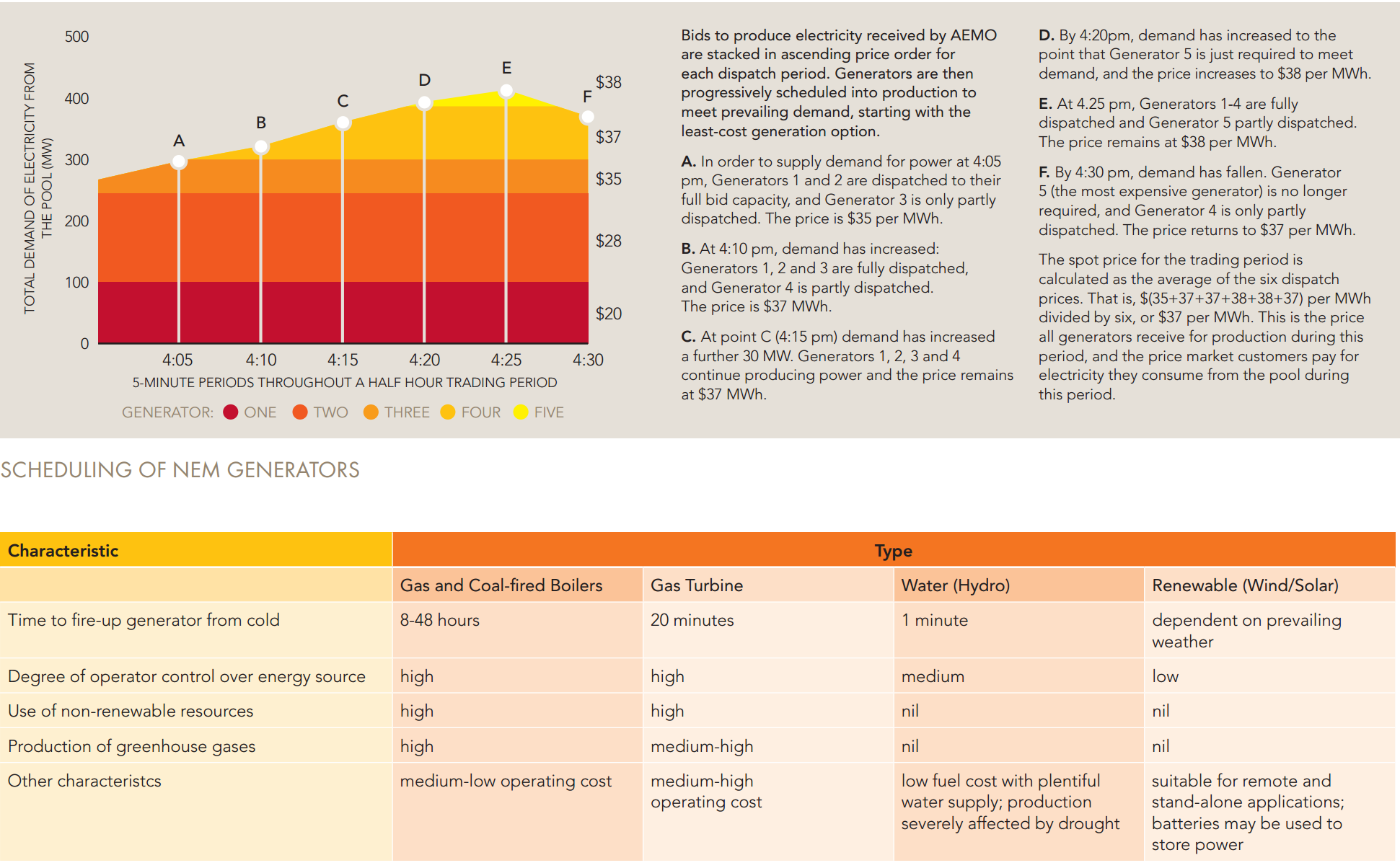

Recall that gas sets the marginal cost of electricity in the NEM owing to where it sits in the wholesale electricity market bid stack. See Australian Energy Market Operator description below:

Advertisement

Turnbull’s politicisation of the issue is deeply ironic given his own party has stirred nothing but energy chaos for a decade and his efforts to fix the problem of gas remain pathetically weak.

Belatedly, Do-nothing Malcolm has finally acted on a domestic gas reservation mechanism. It is starting to impact gas spot prices which have fallen to their lowest in a year:

Advertisement

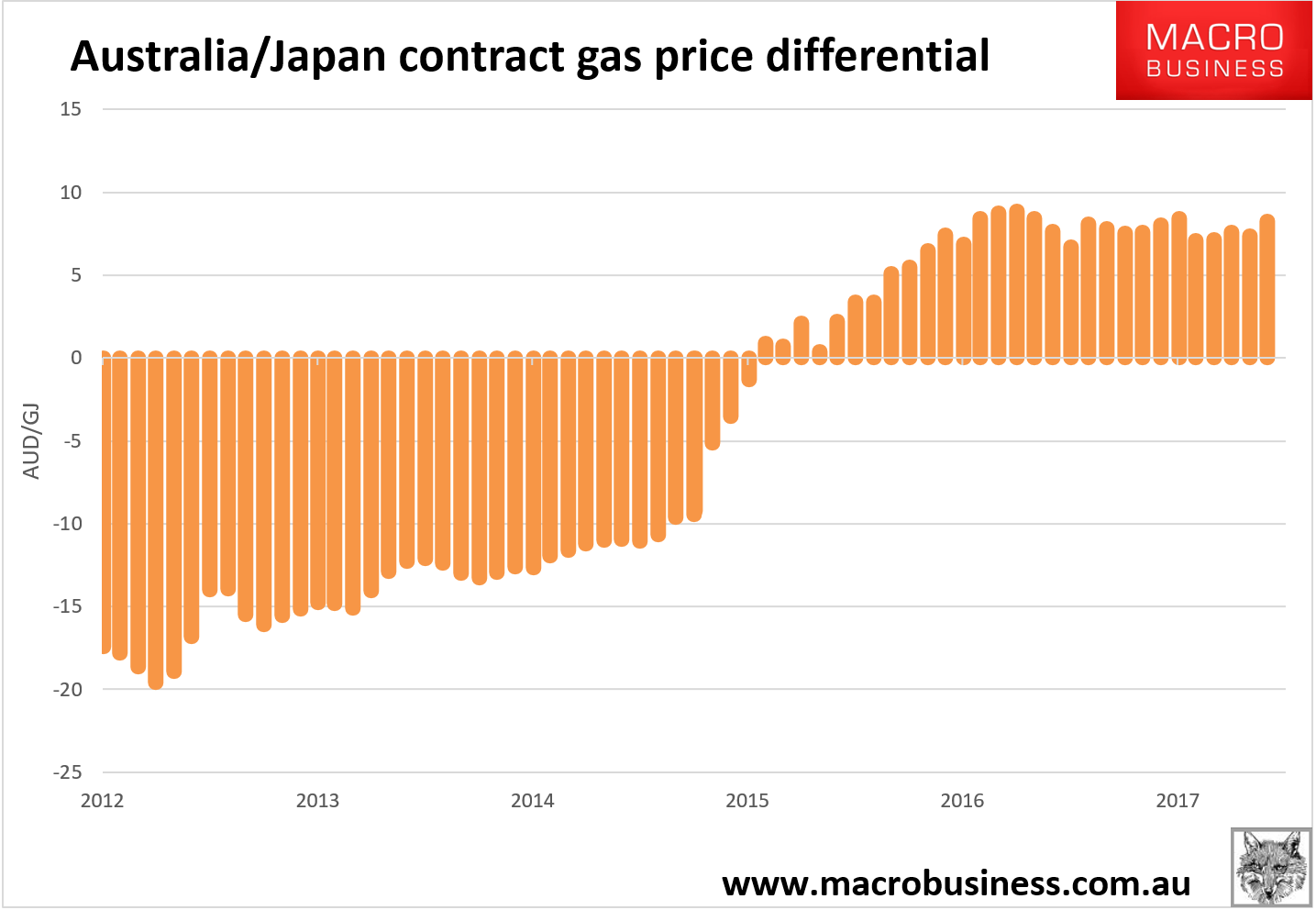

However, the mechanism known as the ADGSM is too slow and too weak. Spot markets account for only a fraction of east coast volumes and there is no evidence yet that the contract market has softened. It has a long, long way to fall before it reaches anything like acceptable prices given trading is anywhere up to $20Gj from $3Gj a few years ago. Meanwhile, the same gas can be bought in Japan at around $8Gj:

Advertisement

Export net back ought to be around $7.20Gj in QLD and $9.20Gj in VIC. These prices should only be the first goal for the ADGSM. They are still plenty high enough to trigger further supply development if it is forced by use it or lose it rules for reserve holders.

Meanwhile, the team at Credit Suisse have already given up on the ADGSM:

High prices set in stone?

It feels ever more certain to us, as things evolve, that the ADGSM will bring little to the domestic gas market other than sustainably higher prices and a catalyst to invest with more certainty in importing LNG.

Whilst we wrote earlier this year (here) that we saw third-party gas as the most logical gas to target in order to balance the market, it was under the construct that some form of subsidy could occur to allow the domestic market to get the gas at the price that the LNG projects are buying that gas at. The ADGSM has targeted this gas, but left price alone. In reality, at the federal level, it is impossible to target price as reservation falls under state not federal rules.

As we sit back and assess what we think the ADGSM will achieve, the sad reality is that our ever firmer view is that it adds some complications to the tenure of available domestic supply (by looking at a short market in blocks of 1 year – although what else can you do, hopefully at least the determination is made as early as possible each year) but more unfortunately will actually enshrine higher domestic gas prices. To be clear, many of the legislative mistakes were made back at the time of sanction, not now, and the nature of Australia’s resource ownership at the state level, leaves few other options open.

Whether there are any policy options available that could reach a different outcome is well beyond our pay grade but, unfortunately for domestic buyers, by effectively only targeting GLNG volumes, and not price, the benchmark price for domestic gas will be set at the netback price on by far the highest price gas heading out of Curtis Island.

Where credit can be given to the ADGSM is that it should at least alleviate the possibility, or maybe just excuse from wholesalers, of scarcity pricing. Sure the new effective price is high, but at least a ceiling is there (and in theory other sellers can step up to the plate and try and beat that price).

Ironically all gas producers, including Santos, should actually be pleased with the ADGSM. It is certainly easy to understand the economic rationale for the upstream industry holding out GLNG as the poster child of all that is wrong, given this highest of benchmark prices it sets.

With toys being propelled out of prams from all sides of the debate, it is very hard to get a clear picture of who and what is impacted, not to mention what the ultimate aim of the domestic gas market should be. What we do feel ever stronger about is that importing LNG into the Southern States is rational at every level (economically, politically and from a security of supply perspective).

We have spent a long time looking for winners in the whole east coast gas debate. Whilst the ADGSM might have ensured the upstream industry ironically end up as potentially beneficiaries, there is clear scope for material returns to be made for those importing LNG. We try and talk through some of the logic and broad numbers around importing in this note and explain why, perversely, it is perhaps the outcome that should be most supported by politics, given (particularly with subsidies) it can deliver gas into Australia below the price at which the ADGSM is seemingly setting.

A lot of mudslinging, rarely with a pure motive

One of the greatest challenges in the east coast market is to work out, collectively, what is the desired outcome of the intervention (or lack thereof). It is extremely hard to find an impartial view on it all, where agendas aren’t set by financial or political implications.

The reality is that the 3 Queensland projects were waved through under a Labour government, yet the incumbents definitely “own” the problem. The resources are owned by the states, many of whom have obfuscated gas development in their own states that clearly puts future gas development in jeopardy, but we would stop short of adhering to the view that the moratoriums/political red tape have really done anything to stop material amounts of gas that would otherwise have come to market now or in the near future. However, the battle lines are drawn politically with state politics and the upstream gas industry seemingly held accountable (just not financially accountable by the ADGSM).

The upstream industry is relatively united in its push to highlight GLNG/Santos as problem creator, as well as politics and the pipeline industry. As mentioned prior though, for anyone with gas to sell domestically, getting the benchmark price set as GLNG netback (given it has the highest price contract by some way) sets a higher price for domestic sellers.

The wholesalers of gas (AGL, Origin, EA etc) seem to blame all of the upstream industry, government and the pipelines – this may be closest to reality, aside from not acknowledging a number of them both deciding to sell gas to the LNG projects and currently making huge margins where they do still have contracted gas to onsell.

So it goes on that everyone is pointing the finger at everyone, perhaps unsurprisingly with the conclusion of their point providing a financial or political win to themselves.

The ADGSM looks set to enshrine higher prices

For all the mudslinging from all parties, the culmination of it all to date is the ADGSM. There is plenty of commentary around at the moment that the reduction in spot gas prices in Australia show the ADGSM is starting to work – we would highlight this is far more likely due to the maintenance at the LNG projects on Curtis Island, but also that the real challenge here is to provide long-term, contracted gas to industrial users, not a few TJ/d floating around cheap on the spot market for a few days.

As we have discussed before, and seems increasingly likely, the actual outcome of the ADGSM looks to be an enshrining of higher gas prices for the domestic market. Sure it will be cheaper than the A$20/GJ+ that gets bandied about, but from a producer perspective it will lock in higher well head prices, by some margin, than are currently seen. To be clear, we believe prices would have been far higher if just left to the open market too, but in many ways the structure of the ADGSM provides a more solid foundation to a view on pricing (if potentially to a lower price than leaving to market forces would have delivered).

Again the debate comes back to what the ADGSM actually wants to achieve, or more accurately what legislation over resource ownership would actually allow federal politics to achieve. The incessant argument by the upstream industry that there isn’t a problem with supply, just with price, is as unhelpful as it is ridiculous. There aren’t many industries in the world where price can’t fix supply, but it is a moot point in this debate. Absolutely gas will be diverted by the LNG projects at the right price, but when prices are already 2x or more (at the well head) than they were a few years ago, it isn’t rational to suggest that the market “owes” the poor, old upstream industry a higher price to incentivise it to supply more gas domestically.

But is providing affordable gas to domestic industrial users what the target should be? Everyone will have their view on this, it is not our place to push our views onto the debate. What we can say is that the ADGSM as it stands will not be a golden bullet to reduce gas prices on the east coast and has, perhaps inadvertently, anchored the domestic gas price to the highest cost gas out of Curtis Island.

As we have highlighted before (here), setting GLNG netback, as the ADGSM will do, as the swing provider of gas will set prices at the highest benchmark level available out of Curtis Island. At US$65/bbl oil there is a ~A$6/GJ difference between our forecast GLNG netback price and our spot LNG netback price. As such, every upstream producer, including Santos, should be delighted to see GLNG “targeted” under the ADGSM.

Again, we are not trying to pass judgement on the fairness of this all, but the ADGSM only has the power to limit exports not mandate gas to be sold domestically (reservation is a state decision, not federal). It would seem likely too that, under the ADGSM, a net exporter might still be able to export their shortfall gas if they make it available and no one buys it.

So if a shortfall year is called, GLNG theoretically offer that gas to the domestic market (for that 1 year tenure, not longer) at their netback price, meaning they see no FCF destruction. Let’s assume Santos can free up some extra reserves outside of the Horizon contract, they can then sell to that price which is ~A$14/GJ delivered to Victoria at US$60/bbl (remembering that if that gas can come from the Cooper they can save some transportation costs vs physically transporting gas from Queensland to Victoria).

The logic of importing is compelling

There is doubtless plenty who will ridicule the concept of importing LNG into Australia just as it becomes the largest gas exporter in the world in a few years’ time. However, whilst it sounds optically (not sure how something sounds optical, but you know what we mean) stupid, we believe it is both logical and economically compelling.

One of the first things to remember is that the resources are under state ownership and legislation, not federal. On top of that there is an expensive, unregulated pipeline network that connects these states on the east coast.

In reality, Victoria, for example, deciding to import LNG whilst Queensland exports it is no different to a European country who has some indigenous production deciding to import LNG rather than take more pipeline gas from another country (Russia etc) that it is connected to. There are no collective, overriding constitutional powers over all the gas in Australia, just like there isn’t in say Europe. So each individual state should rationally look to secure gas, whether it has indigenous supply or not, at the cheapest price possible. Sure, their own state policies may be obfuscating cheaper indigenous gas coming to market, but that is beside the point when you are a gas buyer – you can be ideological, or you can try and secure the most affordable gas physically available.

So when one gets past the misguided notion that there is a federal solution to this all, and that it is “illogical” to import LNG, it all comes down to a question of price. Where and how can gas be procured the cheapest. This is where importing comes into its own in the new world order.

The domestic price is getting anchored to expensive LNG

As we have discussed prior, the domestic gas price under the ADGSM is getting anchored towards a very high priced contract at GLNG. We estimate that, for rule of thumb (without knowing the exact slope or constant), that we should assume that the GLNG contract is on a slope of ~14.5x. For these numbers, we are assuming that is for a GJ price, not a MMbtu, so closer to a 14x slope in reality which may be too low. Whilst MMbtu is the common LNG parlance, we’ll stick to GJ here to make it easier to discuss in the context of the Australian domestic gas market.

This would equate to a >A$10.50/GJ netback price at Wallumbilla at US$60/bbl oil, after taking into account cash liquefaction costs on Curtis Island. In other words this is the price at which GLNG is FCF ambivalent between exporting the gas and selling it domestically.

For someone looking to import LNG into Australia (or anywhere) now, it is likely that you could sign a long-term (10+ years if desired) contract on a slope of 11-12x (again, we are assuming a GJ, not MMbtu number, so divide by 1.055 to get the MMbtu number). At US$60/bbl oil, this would equate to gas costing ~A$9.60/GJ pre transportation costs. This is despite the fact that the netback GLNG price avoids ~A$1/GJ in cash liquefaction costs.

Transportation costs the real clincher

If you landed from Mars you would probably look at the above numbers and say, fine the imported LNG is cheaper than the GLNG contract, but surely it is going to be cheaper to transport that gas from Queensland to say Victoria than it is going to be incur the cost of fuel gas, ship it from another country and then regasify it. Thanks to an unregulated, effectively monopoly pipeline network in Eastern Australia, this is where people would be wrong.

Clearly it costs less to transport gas from Queensland to NSW than it does to Victoria, but if we take Victoria as the example then, depending on who you listen to, it costs somewhere between A$2.75-3.50/GJ to get gas from Wallumbilla through the pipeline network.

If one was importing LNG then shipping from say Western Australia or PNG might cost you ~US$0.50/GJ. The bigger unknown is the cost of the regas facilities. At a best guess, we assume that the combined cost of the FRSU and the onshore facilities would be ~US$1/GJ.

Hence, if the gas was the same price at Wallumbilla as at say in PNG (and we are actually arguing it is cheaper in PNG on new LNG slopes) then the imported transportation/regas costs are coming in at ~A$2/GJ vs the A$2.75-3.50/GJ from the pipeline network.

Putting the numbers together

We should make very clear that these numbers are all estimates to highlight the scale of the opportunity available. Only when you actually take a decent volume to an LNG seller will you find out what they will sell for, likewise with shipping costs and building the regas infrastructure.

As an importer you have the option to sign up a traditional oil linked contract, a US Henry Hub based contract or take your chances on the spot market (or a mixture of some or all of these benchmarks).

There are a number of moving parts in input costs here (some of which can be hedged of course), but we have come up with 6 different delivered price scenarios to Victoria. We have used a 75c A$/US$ for all scenarios:

■ GLNG netback with lower pipeline costs: This assumes a 13.8x slope for the GLNG contract (we suspect well too low), which equates to a 14.5x slope on a GJ basis. We have assumed cash liquefaction costs are 9% of the export price and that pipeline costs are A$2.75/GJ.

■ GLNG netback with higher pipeline costs: This assumes all of the above, apart from with A$3.50/GJ pipeline costs.

■ Importing oil linked LNG on 12x slope: This assumes LNG is imported on a FOB 12x slope on a GJ basis (~11.4x on a MMbtu basis), shipping is US$0.50/GJ and regas costs (including onshore) are US$1/GJ.

■ Importing oil linked LNG on 11x slope: This assumes LNG is imported on a FOB 11x slope on a GJ basis (~10.5x on a MMbtu basis), shipping is US$0.50/GJ and regas costs (including onshore) are US$1/GJ.

■ Importing Henry Hub low end: This assumes a US$2.75/mmbtu Henry Hub price (+10% sourcing fee), US$2/GJ for US liquefaction, US$1.50/GJ for shipping and the same US$1/GJ for regas in Australia.

■ Importing Henry Hub high end: This assumes a US$4/mmbtu Henry Hub price (plus 10% sourcing fee), US$2.50/GJ for US liquefaction, US$2.30/GJ for shipping and the same US$1/GJ for regas in Australia.

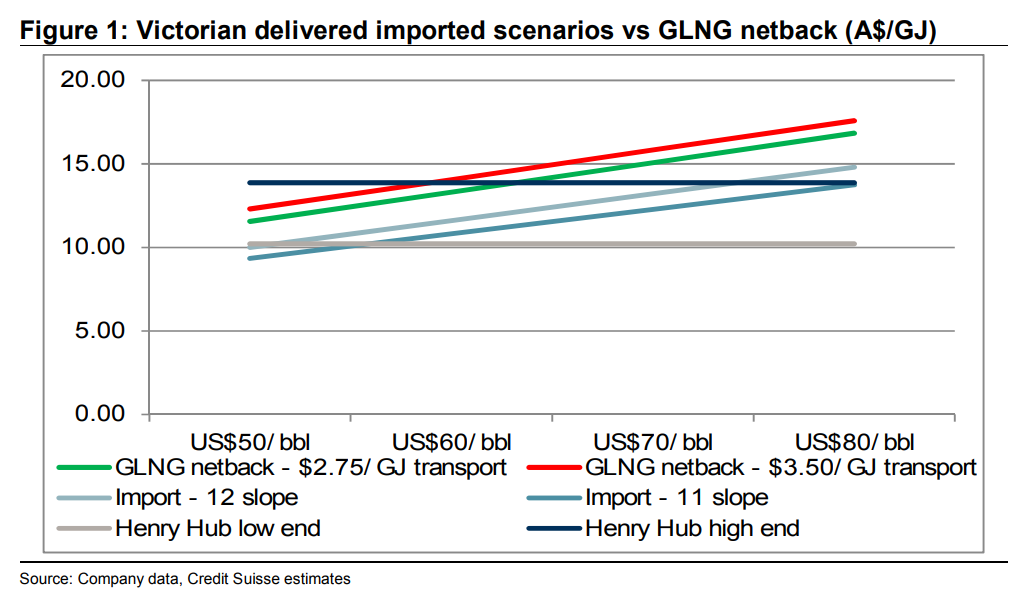

As can be seen in Figure 1, the spread of delivered prices is extremely large, unsurprisingly dependent on assumptions around the key inputs.

One thing we would highlight strongly though, if you believe there is a strong enough base of demand that importers can contract, is that oil-linked imports are sustainably cheaper than the GLNG netback price. In effect, importers clip the spread on the price differential plus the fixed transportation cost differential.

For Henry Hub based imports, it clearly depends hugely on the input variables. Henry Hub is still a traded commodity, but does intuitively appear to have less volatility risk on a 5-10 year view than oil does (although saying that about any commodity is probably silly, including oil as well of course). The bigger variants for Henry Hub based imports are the liquefaction fee and the shipping rates – with the liquefaction fee, a large part of US contracted volumes have been taken by portfolio buyers who have not yet resold those volumes (Woodside being a point in case). To the extent that these players are willing to recoup only part of their liquefaction costs in order to on-sell the volumes, this fee could be below the cost of new build liquefaction (which itself seems to come down).

Granted with a wide range, and dependent on how much risk importers are willing to take on, at higher oil prices we could be talking about a A$2-4/GJ cost advantage versus GLNG netback priced gas delivered. If one was importing 50-150PJa of gas, and these numbers are post recouping the cost of your infrastructure, this is big biscuits.

Does the margin get competed away?

There is plenty of logic that might say that the other LNG producers in Queensland (APLNG and QCLNG), who do have spot cargoes, would logically come in and sell their volumes domestically at a price which is above the spot LNG price. Currently, and on our numbers for the next few years, the spot price is likely to be well below contract prices.

Even with the contracted buyers from APLNG and QCLNG, one could argue too that they would be willing to swap out their gas off higher priced LNG contracts (but lower than GLNG), divert some volumes domestically, and repurchase the volumes on the LNG market.

However, we are not sure either of these arguments will stand the test of time.

Firstly when it comes to QCLNG and APLNG selling domestically versus spot cargoes, certainly in the case of APLNG post FY18, if Sinopec do not exercise DQT (Downward Quantity Tolerance) it is quite unclear, given their lower drilling and still marginal 2P reserve cover, whether they will make any incremental volumes available. For both though, beyond this, we again do not think they would look to lock in long term volumes to another source given the huge uncertainty over resource deliverability that both projects have (and remembering that APLNG reserves are booked on ~US$75/bbl oil).

When it comes to swapping out an existing contract, again whilst the buyers might not want the gas now, in China particularly, this won’t necessarily hold true forever. Again here too, if the LNG projects lost some export volumes, given current oil prices and the resource uncertainty, it is not entirely obvious to us that they would look to contract in the same level of volume. At current oil prices it is a real risk that some volumes are uneconomic down the line – so sure, again, they might drip feed in gas when it makes sense, but for short tenure.

Beyond all of this too, as both QCLNG and APLNG are quick to tell us all, they are large suppliers to the domestic market. Given the scale of these volumes, and the initially relatively small volumes the domestic market needs, it may be more punitive to price negotiations on their existing gas to add more supply to the domestic market “cheaply” than it is to let prices rise to their “natural” level under the ADGSM.

Until existing take or pays run out on pipeline capacity, it is unlikely that the pipeline operators would cede any of the margin back to domestic gas producers to transport the gas down to the Southern States. Longer term, importing LNG feels like a major threat to their volumes, but when payments for the next decade are >90% take or pay, it is hard to believe that tariffs would be cut.

This is not all to say that an importer might not have to give some of the margin on offer to the consumer. However, given the prospective margins on offer, it appears that there is plenty of food on the table for all parties to feast on.

Stock implications (or lack of) getting clearer

As things stand at present, it is increasingly probable to us that Santos escapes any financial punishment under the ADGSM. Indeed, entirely counter-intuitively, if Santos are able to free up some gas to sell domestically then GLNG being targeted under the ADGSM is the best thing that could happen to them.

Whether this is right or wrong is not really our place to debate. Under the constitution of resource ownership in Australia, with the resource owned by the state, there is a strong argument that little else other than the current mechanism could have been implemented.

It is a shame if the outcome of all of this is that prices do just sustain a high level and that the domestic gas industry is not forced to reinvent itself to drive down costs, but that appears the path we are going down. With ~300PJa of latent capacity on Curtis Island, and ~60PJa of that under a very high priced GLNG contract, even with imports it is almost inconceivable that there wouldn’t be an end market for new volumes, at a high price, for domestic producers.

In terms of LNG imports, AGL is the most publicly advanced. To us the opportunity looks large enough for other entrants to succeed as well though. Clearly there is logic to LNG portfolio players who are long volumes (e.g. Woodside et al) to look at this, but relationships with industrial customers on the east coast are also key. We continue to believe, from our conversations with industrial gas buyers, that there is a risk of the incumbent intermediaries losing their social license to operate in the wholesale market.

If we are correct to assert that the ADGSM will do little other than prevent scarcity pricing and may in fact inadvertently anchor the market to the highest contracted LNG setback price; the implication is that the current period of high domestic gas prices will be prolonged. AGL and Origin will be beneficiaries of this high price environment in our view: AGL because of the spread between gas power generation costs and its low price coal generation portfolio; Origin due to its strong contracted gas portfolio position and not insubstantial coal power generation. AGL may also through its LNG import leadership gain a first mover advantage and entrench itself with a dominant gas supply position to the southern states.

On the flip side, longer term, a sustained higher gas price does introduce risks on the demand side for both gas and electricity for AGL and Origin. With a large part of electricity demand in Australia from C&I customers (versus ~1/3 for gas), if higher gas prices have a material impact on industrial Australia and see large parts of it close down, that will impact demand for both gas and electricity materially.

Advertisement

$20Gj looks like scarcity pricing to me. Certainly it is discriminatory.

Very obviously the government needs to clearly define what it considers to be the appropriate price and the ADGSM needs to be toughened up until the so-called “market” meets it. If that fails then it’s time to stop the pretense that this is market at all and apply direct price controls. Victoria is already edging that way:

Victorians should be offered a regulated no frills energy price that doesn’t require them to constantly renegotiate contracts, an independent review panel has recommended.

The review was sparked by fast-rising power prices, which have grown by 200 per cent since 2000. The three-person bi-partisan panel of former Labor Victorian deputy premier and Melbourne Water chair John Thwaites, deputy chair of St Vincent’s Health Australia Patricia Faulkner AO and former Liberal minister for public transport and roads Terry Mulder, recommended the introduction of an unconditional basic service offer, which would be set by the Essential Services Commission (ESC).

The basic service offer would be available from all retailers to consumers, designed to protect vulnerable consumers and people who do not switch retailers frequently. But the retailers are also able to offer deals which have lower and higher prices.

If the review’s recommendations are adopted, discounted offers which the retailers regularly offer will have to be displayed in dollar terms, rather than as a percentage, providing greater transparency into the pricing of offers.

Advertisement

The east coast gas “market” has collapsed in any meaningful sense. Social licence has dissolved into a gas cartel that is stealing directly from households and business.

Given the key role energy plays in industry and household income, the national interest is very obviously at stake.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.