The central banker elite meet in Jackson Hole, Wyoming for their annual symposium later this week, but ECB President Mario Draghi made traders sit up and notice a day or two early last night with a speech in Germany. What was surprising, particularly in the midst of the anti-QE brigade, was his staunch support for quantitative easing (QE) that so far has made economies “more resilient”.

So we’ve gone from emergency one-time measures, to “mild tapering”, to monthly purchases, to “this is awesome, makes us all better”.

Here’s the speech via Bloomberg:

Money (sic) quotes for those unable to watch it:

“when the world changes as it did ten years ago, policies, especially monetary policy, need to be adjusted. Such an adjustment, never easy, requires unprejudiced, honest assessment of the new realities with clear eyes, unencumbered by the defense of previously held paradigms that have lost any explanatory power”

“you need serious conceptual analysis and base policy on that, not on prejudice, or — even worse — on moral grounds,” he told reporters after his speech. “Some people say ‘Oh, QE is immoral, because it creates money out of nothing.”

Advertisement

“a large body of empirical research has substantiated the success of these policies in supporting the economy and inflation, both in the euro area and in the United States”

We all know what happens when central banks do studies on themselves and their own performance, don’t we Martin Place?

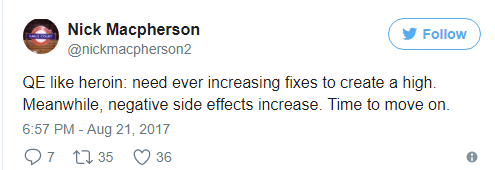

Is there an end game to all this bond buying or are we all turning Japanese? Some have likened QE and the way central bankers see it as a hammer to hit all nails, real or imaginary, as “heroin”:

Advertisement

Nicholas Macpherson, who was permanent secretary to the Treasury from 2005 to 2016, said on Twitter on Monday that attempts to boost the money supply through bond purchases are increasingly leading to “negative side-effects.

Bond traders are fretting that both the ECB and the BOJ are running out of bonds to scoop up as part of their expansive QE programs. With the Fed trying to wind down its own QE without pulling the rug out under the huge bubble in sovereign bonds, this is shaping up to be a massive market risk as overvalued stocks also put managers under pressure on where to allocate funds.

The ECB’s own rules restrict it to only purchasing a third of each country’s debt in circulation, and the supply of German Bunds and Portuguese debt in particular is starting to run thin.

“The 33 per cent issuer limit in Bunds presets a course of [purchase programme] exit, no matter the inflation outlook,” says Harvinder Sian, a Citigroup analyst.

The problem is inflation, or a lack thereof. While in toto the EU economy is recovering on a GDP basis, there has been a trend down in inflation this year to 1.3% last month after hitting 2% earlier:

Advertisement

The best estimates are for inflation to stabilise at around 1.4% next year, nowhere near where Mario Draghi sees animal spirits takeover and thus continue the bond buying program.

The problem of supply of bonds stems from an unlikely place: Germany, where the ECB owns ca.€400 billion of its €2.1 trillion bonds – almost hitting the one third limit rule.

More from FT:

Advertisement

That would effectively force the central bank to selectively taper its bond-buying programme by continuing to purchase the debt of peripheral countries while quitting Germany’s debt markets. The ECB is also approaching its purchase threshold in some smaller eurozone countries. It will max out on Portuguese, Dutch and Irish debt next spring, according to estimates by UBS.

The declining supply of bonds available also means that the ECB is “at risk of reducing stimulus too soon”, says Richard Turnill, global chief investment strategist at BlackRock.

Although many want monetary policy normalisation as soon as possible, the reality is that the European and Japanese economies remain structurally weak with a huge overhang of debt as they struggle to climb out of a potential deflationary spiral.

There are lessons here for the boffins in Martin Place who may have to enact similar QE measures down the road, but I’m not sure they have the right culture in place to look both outward and outside the central banking paradigm.