CEDA: Housing bubble to run another 40 years

Lot’s of material today from CEDA on the bubble:

Historically low interest rates, an unprecedented period of continuous economic growth and strong levels of migration have contributed to ever escalating real housing prices in Australia’s capital cities. The rapid pace of house price growth has contributed to growing housing affordability concerns.

However, the housing affordability problem is not uniform across Australia. While the issue has particularly affected the cities of Sydney and Melbourne, as Dr Nigel Stapledon outlines in Chapter 1, the Perth market is currently in decline. Additionally, housing booms and busts are a commonality in Australia’s history. In light of these factors, where does the current period of pricing sit in relation to previous housing market cycles, and is it cause for concern?

To analyse where Australia’s current affordability problem sits in relation to past property cycles, the first chapter of this publication looks at the past 50 years of housing in Australia’s major cities. Dr Stapledon rounds-out this comparison with a look at the housing experience within other countries in the OECD, finding that it would be “a mistake for buyers to assume that this period is any guide to the future” and that a unique set of circumstances, including the resources boom, has led to this current period. However, he notes that cities with world-class amenities and restricted planning policies will always face greater demand and supply issues than other cities.

When housing becomes unaffordable, the obvious solutions proposed are those that increase supply or reduce demand, and indeed the Turnbull Government has a firm stance that increasing housing supply is the key to unlocking more affordable house prices.1 In Chapter 2, Professor Chris Leishman looks at why, despite policy attention, supply never seems to be able to meet demand.

The complex market structures in the housing sector represent a number of challenges to policymakers. The Planning Institute of Australia has stated that extra costs can be accrued when there are planning delays, which then results in costs being borne by developers, which then pass onto the purchaser, thereby increasing housing unaffordability.2 As Professor Leishman cites, this interaction between the planning system and the development land market can often result in developers staggering permit completions to capitalise on rising market prices. Naturally, this is a difficult issue to solve, and as Professor Leishman puts it, the very nature of the new housing sector has “inadvertently” been created in such a way that drives up the costs of housing.

Looking at the other side of the housing solutions equation, Associate Professor Emma Baker analyses the emerging drivers of housing demand in Chapter 3. As she details, demographic changes, such as unevenly spread population growth – which is predominately happening in NSW and Victoria – are increasing the pressure placed on housing in these states. Additionally, Australia’s ageing population and the increase of one-person households pose new demand-side challenges. These issues are likely to exacerbate with time, and as such, policymakers need to draw their attention to the areas where supply can adapt to these changes, as well as avenues that are available to cool demand.

In Chapter 5 Associate Professor David Morrison looks at the demand-side levers suggested by commentators that can be pulled to achieve this. The suggestions include negative gearing reforms (“by placing a limit on the number of rental properties each investor may hold”), further restrictions to offshore investors through taxation, and imposing a land tax on all property that is uniform throughout the Commonwealth.

While there have undoubtedly always been rising and falling costs of housing in the Australian market, the changes in Australia’s demographic and issues prohibiting supply keeping up with demand are certainly factors driving the current cycle. These challenges pose a number of social issues. The search for affordable housing has pushed many less well-off households to regional areas or on the urban and peri-urban fringes of the major cities, where employment opportunities and access to transport and amenities tend to be relatively poor compared with the inner and middle regions of the larger cities.

Intergenerational issues arise when many younger households, the millennial generation, are unable to access home ownership or can only afford to buy in regions where house price growth generally has been more constrained. This means they do not have the same opportunities to accumulate housing wealth as earlier generations, such as the baby-boomers, many of whom have experienced massive increases in wealth as a result of rising housing prices. Professor Rachel Ong explores this issue in Chapter 4.

Professor Ong also details in her chapter how intergenerational issues can give rise to intra-generational equity issues. For younger generations, increasing earnings inequality and increasing job insecurity have meant that many lower income households are unable to afford home purchase or are unwilling to commit to it. This inequity is compounded when some, but not all, can rely on the “bank of mum and dad” to assist them into home purchase. Additional intra-generational inequities arise for those excluded from home ownership in all generations because of tenancy legislation that tends to favour landlords over renters and results in rental housing providing less tenure security than owner-occupation.

When housing affordability becomes a national issue, economic growth is undermined in a number of ways. A lack of affordable housing can create a spatial mismatch between housing and jobs with a consequent negative impact on economic productivity as labour market participation and geographic labour mobility are reduced. When this happens, the labour market is less flexible than is needed to respond to structural change. Productivity is also reduced when congestion associated with this mismatch and inadequate public transport add to travel times for workers and delivery costs for producers. Reduced employment opportunities will increase income inequality which, in turn, can lower sustained economic growth, as shown by both the IMF and OECD.

The resilience of the Australian economy is threatened by the potential impact of the house price induced rising household debt, held by first home buyers and by established households encouraged by the prospect of capital gains to increase their investment in housing. Concerns with financial stability led to a tightening of lending standards in 2014 but concerns with macroeconomic stability currently are of more concern.

The chapters in this publication provide a more detailed analysis of these issues, and point to the key factors creating the current housing affordability issue. The recommendations that follow take into account the complicated nature of housing reform, and suggest some of the changes that might be needed to address Australia’s housing affordability problems.

All old news for MB readers. The only thing that report does not address, as usual, is excessive immigration. Though Dr Judith Yates offers this cheery prospect:

Looking forward, there can be little sense of optimism about future housing affordability outcomes:

- Demand pressures are likely to continue over the next 40 years. Economic growth per capita is (still) predicted to continue, although at a somewhat lower rate than experienced over the past 40 years. Australia’s population also is projected to continue to grow at only a slightly lower annual growth rate than over the past 40 years, with this growth being concentrated in Sydney and Melbourne.

- Supply constraints are likely to remain. Urbanisation trends are expected to continue, with the proportion of people living in Australia’s capital cities projected to rise from a current 66 per cent to almost 74 per cent.24 Jobs in the future are projected to grow in service and knowledge based industries with skilled labour being favoured over unskilled.

- This will reinforce the steady growth in earnings inequality that Australia has experienced since the mid-1970s.

Increasing population, increasing economic growth and increasing concentration of well-paid employment opportunities, therefore, are likely to continue to put pressures on well-located land in our metropolitan regions. Such pressure will be reinforced by:

- Increasing income and wealth inequality;

- A tax-transfer system that encourages established households to hold on to the growing equity in their owner-occupied housing and to increase their housing wealth by borrowing to invest in residential property; and

- A housing finance system that remains biased towards those most able to pay.

Pressures on the private rental market will continue as low and middle income households are excluded from home ownership and higher income households choose to rent rather than own. As Baker in Chapter 3 and Ong in Chapter 5 observe, these changes indicate a new housing landscape and suggest a need to rethink housing policy.

By my reckoning that will take the median Sydney house price to roughly $4m. Of course, why stop there? Today’s migrants will all be old and require replacing by then so it’ll run for another 40 years, then another, so on and so forth.

The good doctor might want to look out her window now and again. If the mass immigration driving population growth runs for a few more years at current levels then Pauline Hanson will be PM.

The point is that such ponzi-led growth is producing major socio-economic fractures that will break it sooner rather than later (which is kind of the what CEDA is addressing in the overall report).

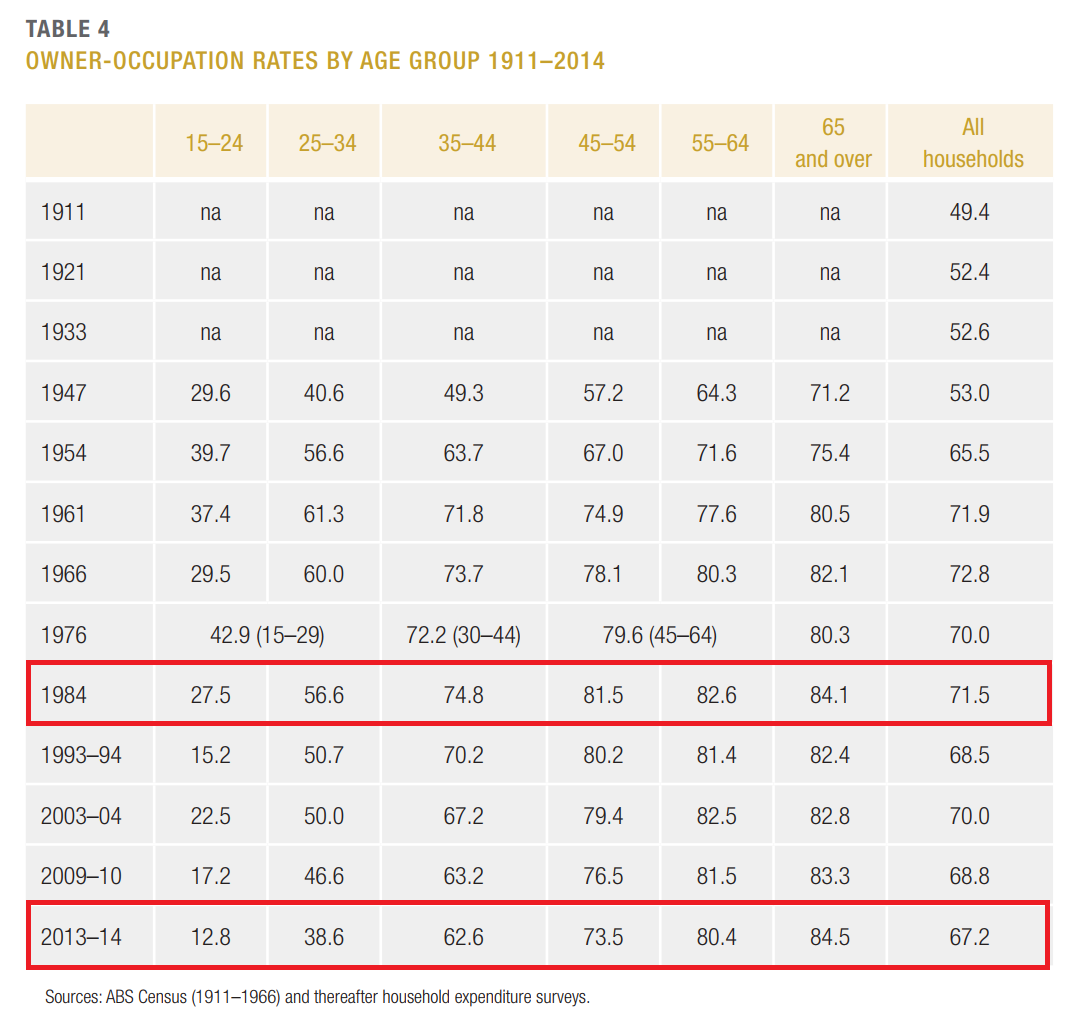

Check out this table:

In the end, the bubble is really just one thing, Baby Boomers screwing everyone else. Ipso facto:

- it will end when the Boomers are screwed back, or

- the system itself breaks of excess.

As it happens we appear to be approaching the convergence of both with Labor’s negative gearing reforms and peak household debt dead ahead.

40 years, my butt. The full report is here.