‘…so you’re a commodity analyst, and you don’t track bitcoin? Should I be worried about that?’ – bitcoin enthusiast

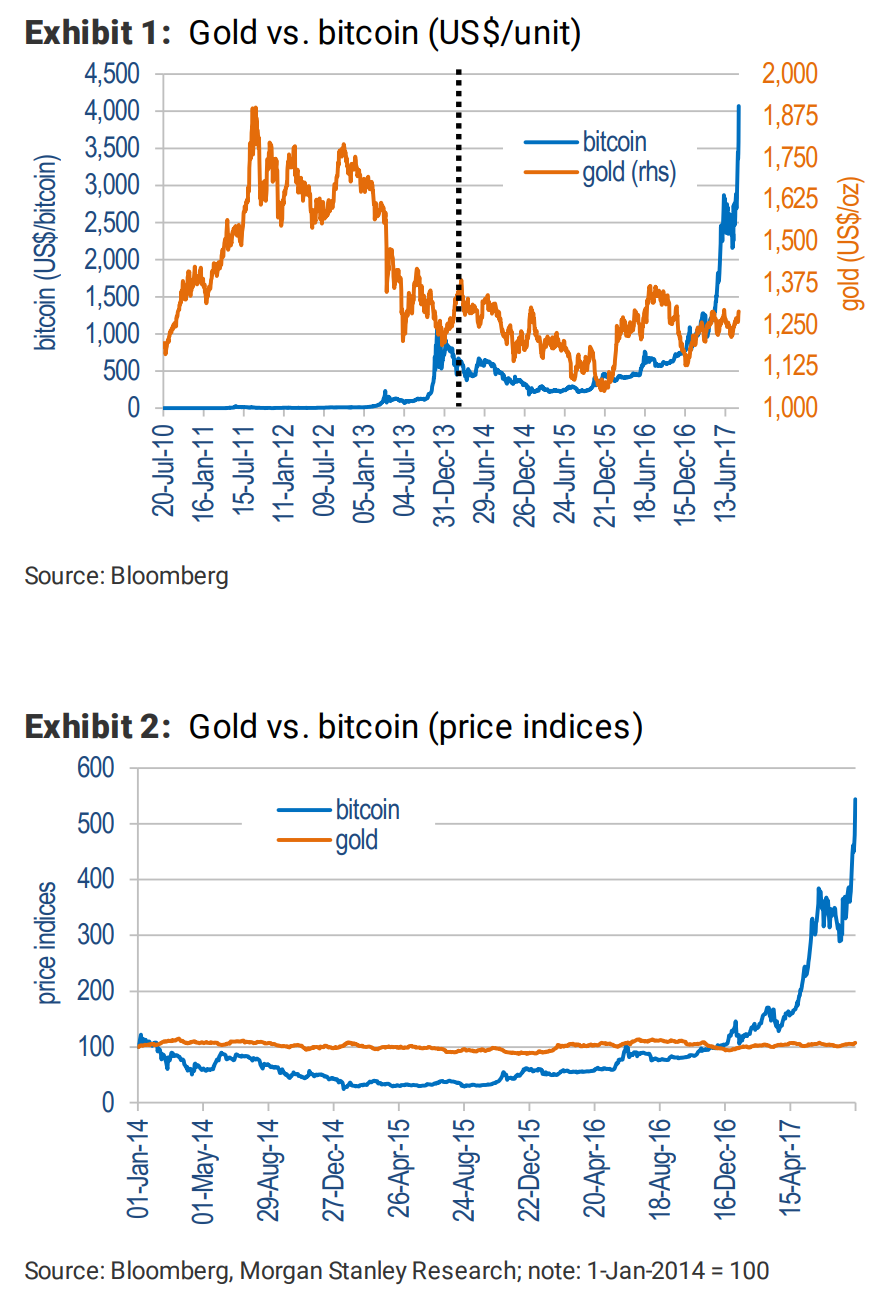

Latest fiat money: Bitcoin’s value has lifted about 5x since a period of relative stability pre-Nov-16, to over $4,000/bitcoin (Exhibit 1,2), on mainly rising geopolitical tensions. Curiously, we’re receiving investor queries on this price performance. As commodity analysts, we don’t model the bitcoin market, or set price forecasts for it. Yes, to expand total bitcoin supply, parties are invited to engage in ‘mining’. But this is a misleadinguse of the term. The fact is,as a globally accessible ‘cryptocurrency’,electronically exchanged directly between players,via a decentralized, intermediary-free, repository-free system (since only 2009) – bitcoin’s really just another fiat money,not a commodity. Why flag it then? Well, beyond its ongoing price surge, some investors believe that bitcoin’s better than gold as a hedge against inflation/uncertainty.

A currency, defined: Both gold and bitcoin possess the properties of a viable currency:a widely accepted medium of exchange;are fungible, durable, portable, divisible and scarce. Butunlike gold, bitcoin exists within a system that can instantly transfer value worldwide + supply is constrained, potentially underpinning its long-term price. These other properties confirm that bitcoin is not a commodity money like gold, but a type of fiat money, consistent with trade currencies:a currency established by law (i.e. in this case,not by government, but certified by network nodes + recorded in public ledger = ‘blockchain’).

Better than gold? So for global money transfers – bitcoin’s a good medium. Indeed, for this function, bitcoin’s better than gold; probably better than conventional fiat currencies too (i.e. transaction costs). But the popular view that this immature currency is also superior to gold as a hedge against inflation/uncertainty, still needs to be tested. Some claim that the protocol limiting bitcoin’s supply growth rate + total that can ever be created (i.e.21 million, by 2140),underpins its value. But if bitcoin is successful long term, we should continue to see competitor cryptocurrencies and market strategies emerge (Global Financials & Payments: Blockchain: Unchained? 16-Jun-17) to exploit the new economic rent – a bearish risk for bitcoin’s price (i.e. few barriersto-entry). And what of uncertainty? Over millennia,gold has demonstrated its ability to endure and preserve value under all circumstances. By contrast, bitcoin’s global platform literally requires the lights to stay on.

It’sa risk: Gold’s value to financial markets has already been incrementally marginalized over the centuries, by the rise of trade-/productivity-backed fiat money. Bitcoin is the latest money to offer gold’s long-standing capabilities + some other unique benefits. While it too may somehow undermine gold’s demand outlook, the rate/scale of the shift depends on the willingness of investors to engage bitcoin/cryptocurrencies. And willingness first requires a time-consuming, trust-building exercise.

Let me ask, then, is bitcoin an asset or a currency? With the wild volatility current at large does anyone seriously hold bitcoin as a fiat currency? I mean, shit, why buy a pizza today with bitcoin at $5 when next month it’s it’ll be $2.50? Next year it might by 50 cents or 5 cents or $100. It’s complete nonsense to discuss it as an inflation hedge when it has effectively no value as a currency.

To see pricing stabilise, bitcoin and other cryptos will have become so widely used so quickly that they’re very unlikely to ever make it. Moreover, the infinite creatibility of cryto means that value can never be stable (wanna buy some MBcoin?), unlike gold, which is just nice and shiny like nothing else.

Sorry so say it but crypto remains nothing more than the first ever fully digistised global ponzi scheme.

Advertisement

I’m surprised governments have not shut it down already.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.