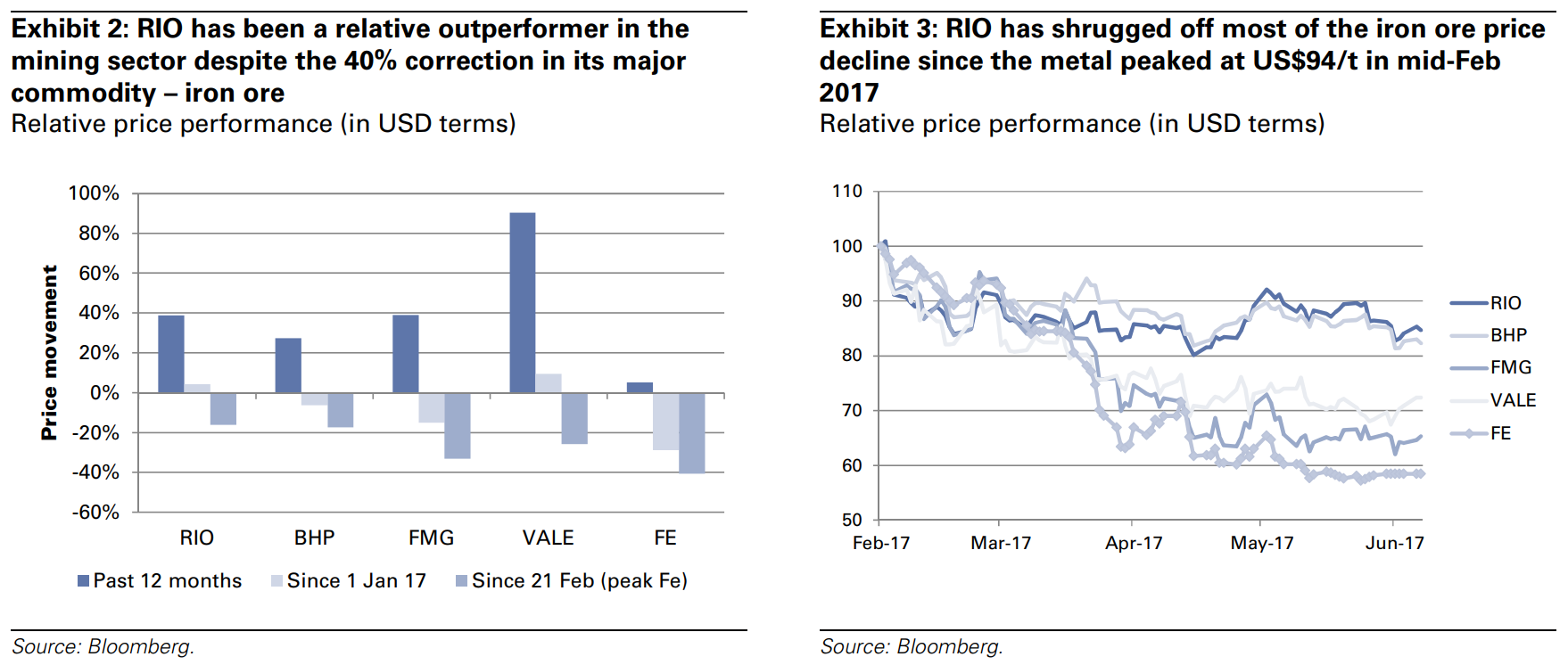

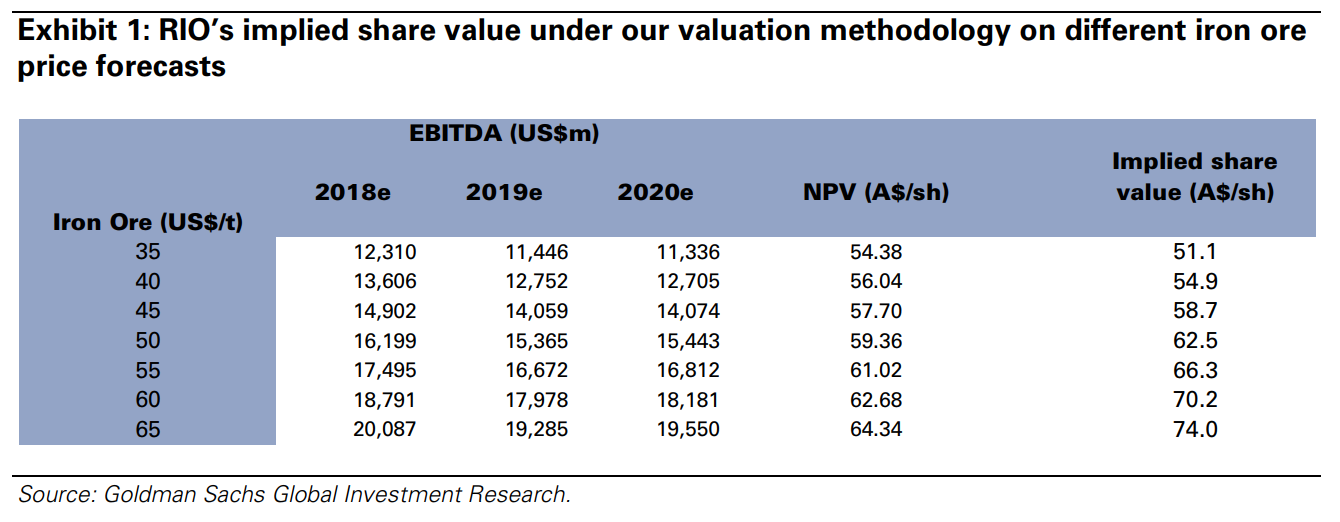

RIO has been one of the best performing large-cap mining companies over the past 12 months driven by rising commodity prices, rapid balance sheet deleverage and early mover advantage in capital returns. However, RIO’s fortune remains heavily intertwined with its largest commodity – iron ore. And here is the catch on the RIO investment case. Since iron ore peaked at US$94/t in February 2017, it has fallen by c.40%. However, RIO is down just 16% whilst its iron ore peers in FMG (-33%) and Vale (-26%) have been more impacted by the falling iron ore price. We put the outperformance down to RIO’s better balance sheet and capital returns. With iron ore prices remaining in a state of flux, we examine the bull and bear investment drivers for RIO in 2H17 and beyond.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.