The Australian Institute (TAI) has released a great paper by renowned energy analyst Dr Hugh Saddler, entitled National Energy Emissions Audit – Electricity Update, which reveals a strong correlation between domestic electricity prices and gas prices, despite gas making up only 10% of electricity generation.

Below are the key extracts from this report:

High electricity prices are caused by the high wholesale price of gas, in both SA and other states

A specific examination of retail prices in SA leads to three strong findings:

electricity prices have historically always been higher in SA than in other states, because there are no low cost, high quality coal and hydro resources in the state;

there is absolutely no positive relationship between the share of wind generation in supply and wholesale electricity prices in the state – in fact a negative correlation;

there is a very strong positive correlation between wholesale gas prices and wholesale electricity prices. It is therefore concluded that price increases in SA, and to a large extent in other states also, are almost entirely the consequence of high wholesale gas prices…

Electricity prices

On 1 July, retail electricity prices increased substantially – reports suggest between 10 and 20 percent, though that depends on how the calculations are done – in Queensland, NSW, SA, Tasmania and the ACT. Prices in Victoria will change, and almost certainly increase, on 1 January 2018. The announcement of the increases has provided ill-informed commentators with another opportunity to attack renewable generation, singling out South Australia for special criticism.

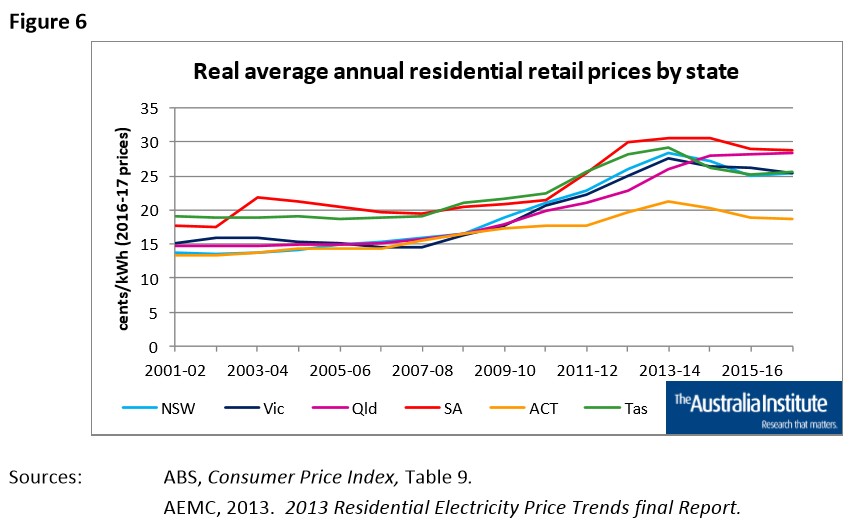

NEEA Electricity Update seeks to provide soundly based factual information about Australia’s electricity system, in the hope of raising the quality of policy debate. To that end, Figure 6 presents a history of residential electricity prices in the NEM states since 2001, expressed in real 2016-17 dollars.

The graph shows that:

prices in the four mainland states have increased by between 60 and nearly 100 per cent since 2001, with smaller increases in Tasmania and the ACT;

the relative increase has been less in South Australia than in the three mainland eastern states;

most of the increase has occurred between2007 and 2013, and, although this cannot be concluded from the graph, was largely caused by higher transmission and distribution (“poles and wires”) costs;

prices in the ACT have always been lower than elsewhere, mainly because of the low cost, compact structure of its distribution network, but, importantly, will be little affected in coming years as its renewable generation share grows towards 100%, because most of the contract prices for renewable electricity are close to or below the expected NEM wholesale prices shown in Figure 7;

prices in South Australia have, conversely, always been higher than in other states, but the difference is no more now than it was in 2001 and less than it was in many of the years in between.

It can also be deduced that, when the 1 July price rises flow through to CPI figures, the resultant retail prices in NSW, Queensland, SA, Tasmania and the ACT will be the highest ever, in real terms as well as nominal terms, and that will also be the case in Victoria from 1 January next.

The reason that prices are higher in South Australia than elsewhere is that the state does not have the large, low cost coal resources of other states, and is completely lacking in significant hydro resources. Together, these were the foundation of the rest of the Australian electricity supply system throughout the 20th century. Until the mid 1950s South Australia was completely dependent on coal imported from NSW, and imported petroleum products. It then developed the remotely located, poor quality coal resources at Leigh Creek, which fuelled a series of power stations built at Port Augusta, and then, when gas was discovered in the far north of the state in the 1960s, was able to add natural gas. Its generation costs have always been significantly higher than those in most other parts of Australia. However, in the 21st century, as the electricity system transitions to renewable generation, South Australia’s abundant wind and solar resources will eliminate, and may even reverse its current generation cost disadvantage.

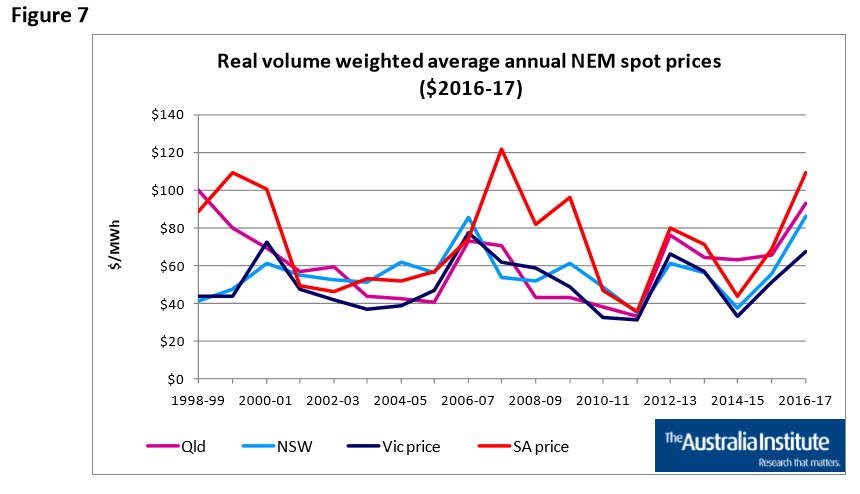

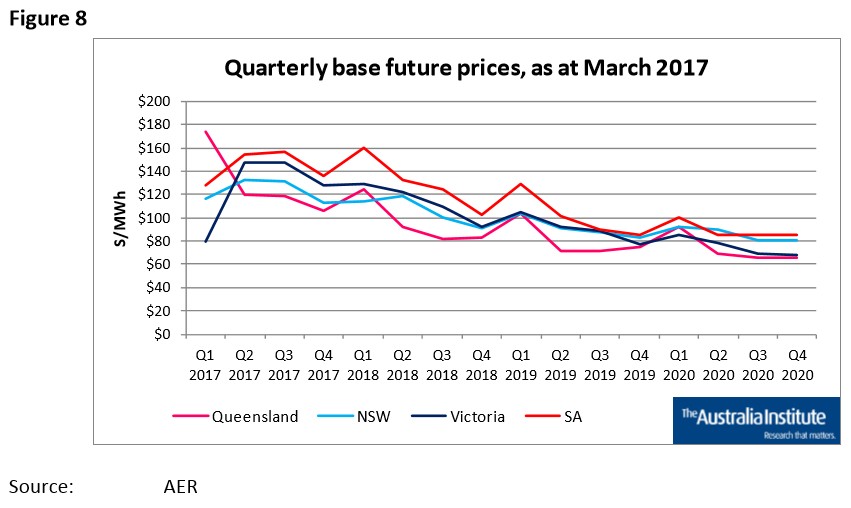

Why have retail prices gone up? The answer is easy to see in the combination of Figures 7 and 8. Figure 7 shows past real wholesale market prices in each NEM region (excluding Tasmania).

The large increase in the year just ended, most of which occurred during the six months from January, is easy to see. Figure 8 shows market expectation of how wholesale prices will move over the next four years, which serves as an indicator of the sorts of prices at which electricity retailers are contracting to buy the electricity they will be supplying to their customers over the coming months. Few anticipated the large wholesale prices increases of the past six months, which means that prices for 2016-17 were largely based on wholesale prices of around $40 to $50 per MWh (4 to 5 cents/kWh). A level of around $100 to $120 per MWh, as Figure 8 suggests, would equate to an increase in retail prices of about 6 cent/kWh. Most of the announced price increases have been a little below this level.

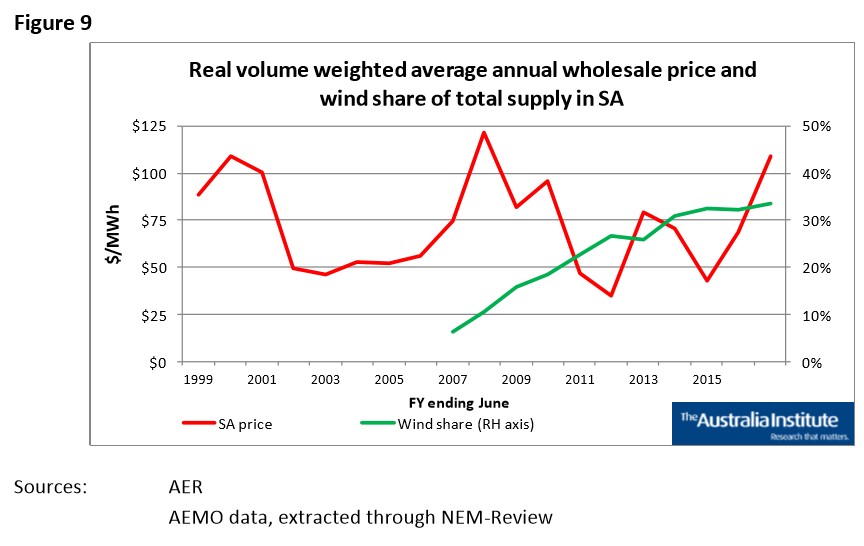

Turning again to South Australia, it is fairly clear from Figures 6 and 7 that higher prices in that state have nothing to do with the amount of wind generation there. That is confirmed by Figure 9, which shows wholesale prices from Figure 7 superimposed on the annual share of total electricity supplied in South Australia (including net imports from Victoria) supplied by wind generation. Clearly, there is absolutely no relationship between the two.

More detailed analysis shows that market wholesale prices are consistently lower when there is a high level of wind generation, than when there is little wind. Over the past four or five years in the South Australia wholesale market, volume weighted prices received by wind generators have been around 20 to 30 per cent lower than volume weighted average prices for the market as a whole, and even further below the volume weighted average prices received by gas generators.

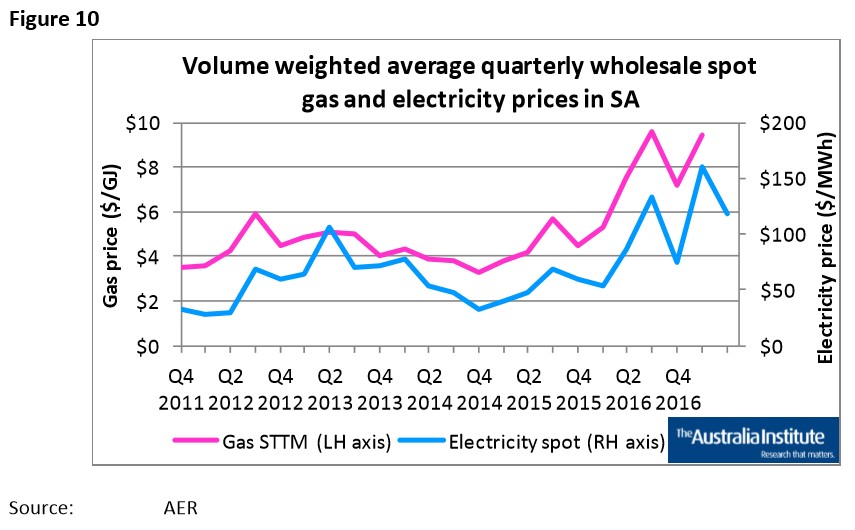

Most of the time, gas generators are the marginal source of supply in the SA market, and thus set the market price. Figure 10 shows the relationship between wholesale gas and electricity prices in the SA market. The gas price is what is called the Short Term Trading Market (STTM) price at the Adelaide gas trading hub. This is the price needed to balance supply and demand each day in the SA gas market. Most gas is traded under term contracts, not through the STTM, but the STTM is a good indicator of the marginal price of gas. Similarly, the NEM spot price is not the actual price at which most electricity is traded, but is the marginal price.

The correlation between the two data series is striking, confirming that higher wholesale electricity prices, and hence higher retail prices in SA are almost entirely caused by higher gas prices. Technical data on power station performance makes it possible to calculate the quantitative relationship between the two sets of prices. The two largest gas fired power stations in SA are Torrens Island B and, when it is operating, Pelican Point. According to AEMO data, Torrens Island B has a sent out efficiency of 28.5%, meaning that 12.6 GJ of gas are burned for each MWh of electricity sent out. This means that an increase in the price of gas, from $5 per GJ in Q1 2016 to $9.5 per GJ in Q1 2017, will increase the fuel cost of Torrens Island B by $57 per MWh, or just under 6 cents/kWh. The corresponding increase at Pelican Point, which is much more efficient, but much smaller, would be $35 per MWh. No wonder retail electricity prices have gone up in South Australia.

A similar, though less stark effect is seen in the other mainland NEM states…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.