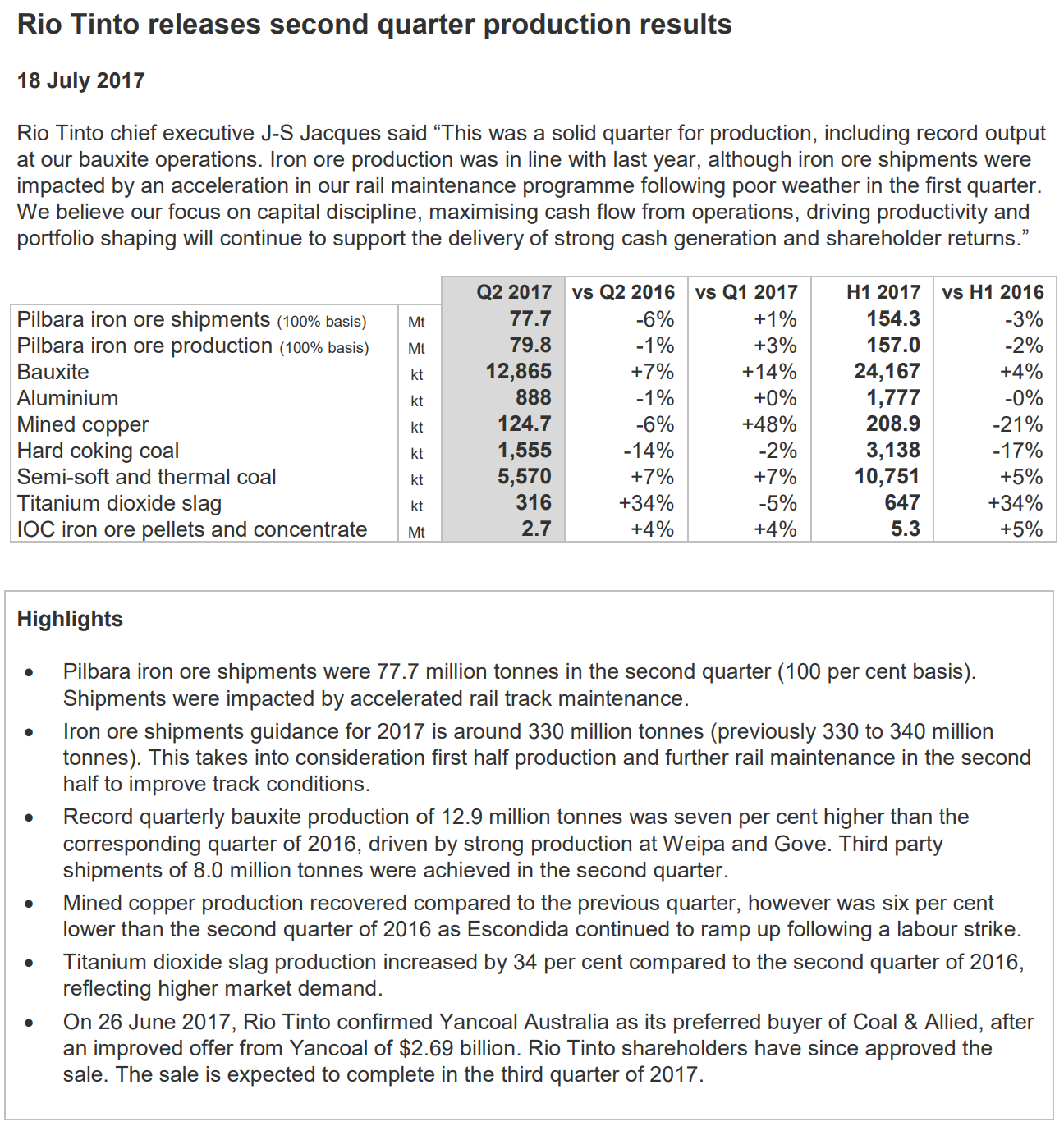

Pilbara operations Pilbara operations produced 157.0 million tonnes (Rio Tinto share 128.7 million tonnes) in the first half of 2017, two per cent lower than the same period of 2016 reflecting adverse weather conditions in the first quarter. Second quarter production of 79.8 million tonnes (Rio Tinto share 65.0 million tonnes) was slightly lower than the same quarter of 2016 and three per cent higher than the first quarter due to fewer weather impacts. First half sales of 154.3 million tonnes (Rio Tinto share 127.2 million tonnes) were three per cent lower than the same period of 2016 due to weather impacts in the first quarter and accelerated rail maintenance activity in the second quarter. Second quarter sales of 77.7 million tonnes (Rio Tinto share 64.0 million tonnes) were six per cent lower than the same period of last year, also reflecting the rail maintenance. Further rail maintenance will continue throughout the remainder of 2017, albeit at a lower level than in the second quarter. The expenditure, a portion of which is capital, is included within the Group’s existing guidance. Approximately 19 per cent of sales in the quarter were priced with reference to the prior quarter’s average index lagged by one month. The remainder was sold either on current quarter average, current month average or on the spot market. Approximately 64 per cent of sales in the quarter were made on a cost and freight (CFR) basis, with the remainder sold free on board (FOB). Achieved average pricing in the first half of 2017 was $62.4 per wet metric tonne on an FOB basis (equivalent to $67.8 per dry metric tonne). In 2016, the full year price achieved was $49.3 per wet metric tonne (equivalent to $53.6 per dry metric tonne).

So, RIO will have to ship at accelerated rate in H2 to reach that 330mt guidance.

I guess there is no end of excuses RIO can roll out to cover its withholding 30mt of iron ore from the market. Last year it was automated trains, this year rail maintenance. Next year it could be Elvis spotted at Silvergrass.

The strategy makes no economic sense given its is preventing 10% of its volumes reaching market. By doing so it may be supporting prices a little but it’s keeping less efficient mines in business for longer. That may create value over the short term for executive bonuses but over the long it only means even lower prices for longer shareholders. Previous investment to build unused capacity is going to have to be written down at some point.

Advertisement

Bring back Sam Walsh. He knew the business better.

To wit:

Andrew Forrest’s Fortescue Metals Group has flagged it will add the capacity for another 20 million tonnes a year of iron ore production when it develops its next Pilbara mine, just two years after it led a controversial campaign for Australia’s big iron ore producers to cap their output.

Planning documents unveiled by Western Australia’s Environmental Protection Authority yesterday show that Fortescue’s proposed Eliwana mine will have infrastructure capable of pumping out 50 million tonnes a year of iron ore, well above the 27 million tonne capacity of the ageing Firetail mine it is meant to replace.

The extra capacity could allow Fortescue to lift its total annual output towards 200 million tonnes a year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.