Labor leader, Bill Shorten, confirmed over the weekend that the party would target trusts, which it views as a tax shelter favouring the wealthy. From The AFR:

Opposition Leader Bill Shorten will detail a Labor clampdown on trusts and other tax minimisation vehicles…

Mr Shorten confirmed the push against trusts on Sunday…

Asked if family trusts – estimated to hold about $3 trillion – were in Labor’s sights for reform, Mr Shorten said trusts had sound legal protection.

“But I’ve made it very clear that I do have a principle and that is we should have one tax system for all,” he said on the ABC’s Insiders…

Mr Shorten said trusts were “a legitimate business tool”, and he was committed to “clarifying, updating and rewriting Australia’s trust laws” in a way that would “greatly assist the 660,000 trusts in Australia”…

Shorten’s proclamation over the weekend follows new research released by The Australia Institute (TAI), which shows that the equivalent of 21.6% of Australia’s national income was run through a trust, which is overwhelmingly skewed to high income earners. Below are the key extracts:

Advertisement

According to the ATO in 2014-15 (the latest year available) there were 823,448 trusts with assets of $3.1 trillion and revenue (total business income) of $349.2 billion.10 Of the 823,448 trusts 642,416 or 78 per cent were discretionary trusts which ‘are established by the person who sets up the trust i.e. the trustee, and the trustee has the power to choose, at his or her own discretion, the amount of money that will be paid to each beneficiary under the trust… the trustee has the discretion to choose which beneficiaries receive payment and how much payment they receive’.

From the national accounts data for the year 2014-1512 The Australia Institute estimates that 21.6 per cent of Australia’s national income was run through a trust.

To most people this must seem very strange. We understand how individuals are taxed and recognise other taxable entities such as companies but most people would be unfamiliar with trusts. And the fact that they are so large, some 22 per cent of GDP, does sound very high. Moreover, trusts have been growing rapidly in recent years.

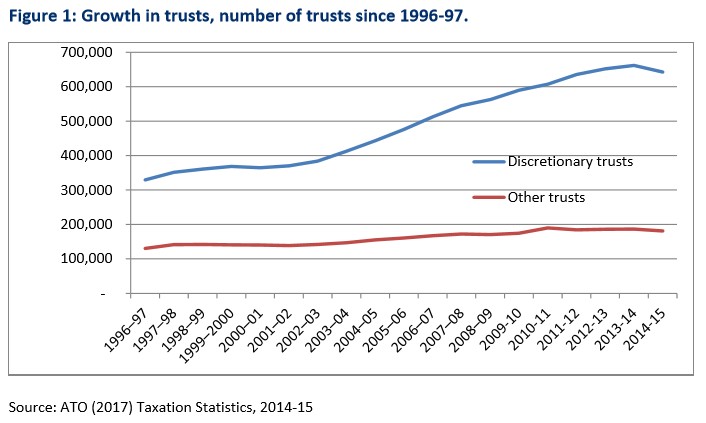

Figure 1 gives illustrates the data for the number of trusts for the period over which the ATO has made the data available.

Figure 1 shows how most of the growth has been in discretionary trusts which grew from 329,475 in 1996-97 to 642,416 in 2014-15, and increase of 95 per cent. The nondiscretionary trusts grew by a more modest 39 per cent from 130,555 to 181,032 over the same period. Growth in discretionary trusts has far outweighed the growth in nondiscretionary trusts…

Revenue forgone

One observer, Dale Boccabella, Associate Professor of Taxation at the University of NSW, has estimated the revenue loss at $2 billion per annum.13 It is hard to imagine anyone would set up a trust unless there was another legitimate reason or there were tax advantages of at least one per cent of income. An alternative and very conservative estimate would be that the revenue foregone might be one per cent of the total business income received by trusts or $3.5 billion. Given the ATO figures for the number of taxpayers, tax avoidance through trusts would cost each taxpayer an average of $202 per annum on Boccabella’s figures and $354 per taxpayer if the one per cent assumption is correct…

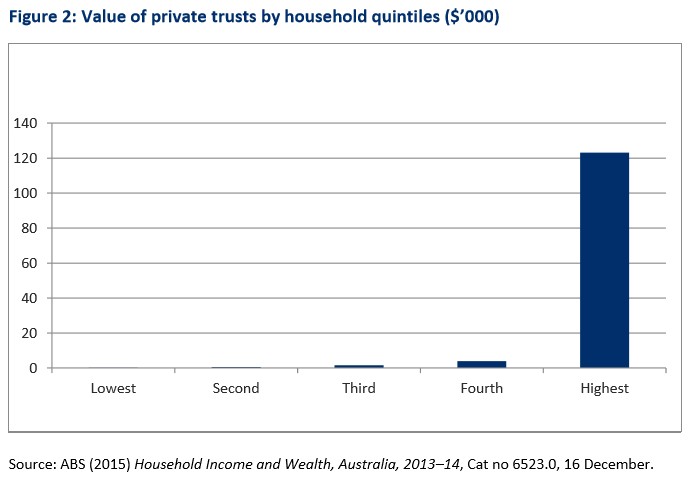

The Australian Bureau of Statistics gives estimates of household wealth which includes specific assets such as bank accounts, shares and other categories and, for our purposes, includes a series for the value of private trusts. These figures are shown for households by quintiles starting with the bottom quintile of wealth holders and ending up at the highest quintile. That data is presented in Figure 2.

Figure 2 shows clearly that virtually all wealth held in all private trusts is by the 20 per cent wealthiest households who hold an average $123,100 in private trusts. Indeed, while the net wealth of the top 20 per cent is 71 times the bottom 20 per cent, in relation to private trusts the top 20 own 1231 times the amount owned by the bottom 20 per cent. Put differently the top 20 per cent account for 95 per cent of the value of all wealth held in trusts…

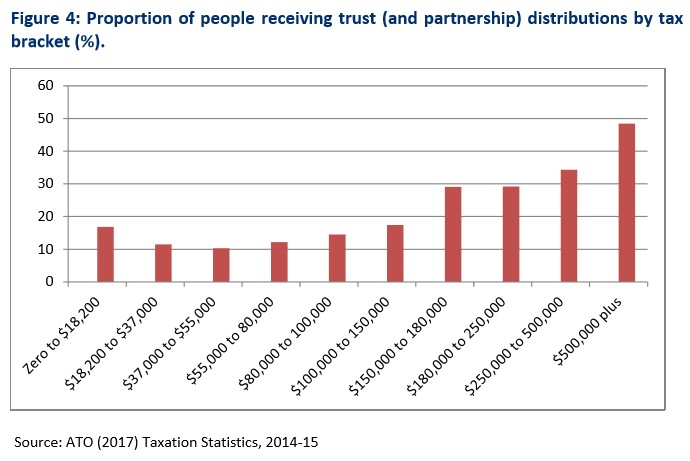

On average 13.6 of all taxable taxpayers receive a distribution from a trust (or partnership). Figure 4 shows the proportions in each tax bracket who have some distribution/s.

Figure 4 clearly shows that higher income earners are most likely to receive a distribution from a trust (or partnership). Hence 48.4 per cent of those with incomes over half a million dollars—almost half—receive some sort of distribution…

In short, Labor appears to have strong grounds for targeting trusts.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.