Fairfax’s Matt Wade is the latest to warn on China’s debt time bomb:

Many thousands of Australian jobs depend on the health of the Chinese economy…

For some years now China’s economic growth has been underpinned by an explosion in corporate lending. China has accounted for half – yes half – of all new credit created globally since 2005 according to the New York Federal Reserve. That’s a huge share for an economy that now only accounts for about 15 per cent of the global economy.

Alarm bells rang last August when the International Monetary Fund pointed out the trajectory of credit growth in China was eerily similar to countries that experienced painful post-debt boom adjustments in the recent past. This includes Japan in the 1980s, Thailand prior to Asian Financial Crisis and Spain prior to the European debt crisis.

The sheer pace of lending growth makes it likely many loans are going to marginal borrowers or unviable projects. A recent Oxford University study that evaluated 65 major road and rail projects in China concluded just 28 per cent could be considered “genuinely economically productive”.

The rapid expansion of China’s less regulated “shadow banking” sector adds to the complexity. The Reserve Bank has described China’s financial system as “increasingly large, leveraged, interconnected, and opaque”…

The best outcome is for what economists call a soft landing. Under this scenario Chinese authorities would accelerate reforms, somehow scale back credit growth and clean up bad debts while economic growth keeps humming along at a healthy rate…

But as economist George Magnus, an associate at Oxford University’s China Centre, says “you can’t resolve a debt problem peacefully”.

…slower Chinese growth… would hit Australia in two ways, first by reducing the price of the commodities we export but also by reducing Chinese demand for Australian goods and services.

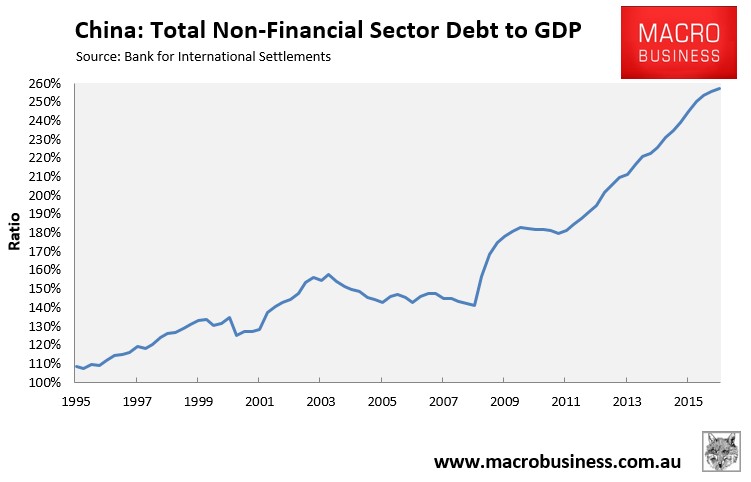

To put China’s debt build-up into perspective, here’s a summary chart using data from the Bank for International Settlements:

Note the explosion in Chinese non-financial sector debt over the past decade.

As noted earlier by Houses & Holes, China will hold a long-delayed key financial work conference later this month, which will focus on financial security in the run-up to an expected changing of the top Communist Party guard later this year. The big issues up for debate are expected to include an overhaul of the financial regulatory regime, financial security and opening up of the financial markets.

If Xi Jinping’s poliburo takes another crack at reform then Chinese growth could really slow and the bad loans could turn unruly.

The Chinese debt time bomb continues to tick.