The Office of the Chief Economist, formerly BREE, has done a reasonable job of slashing the outlook for Australian dirt earnings below Budget forecasts, but not enough.

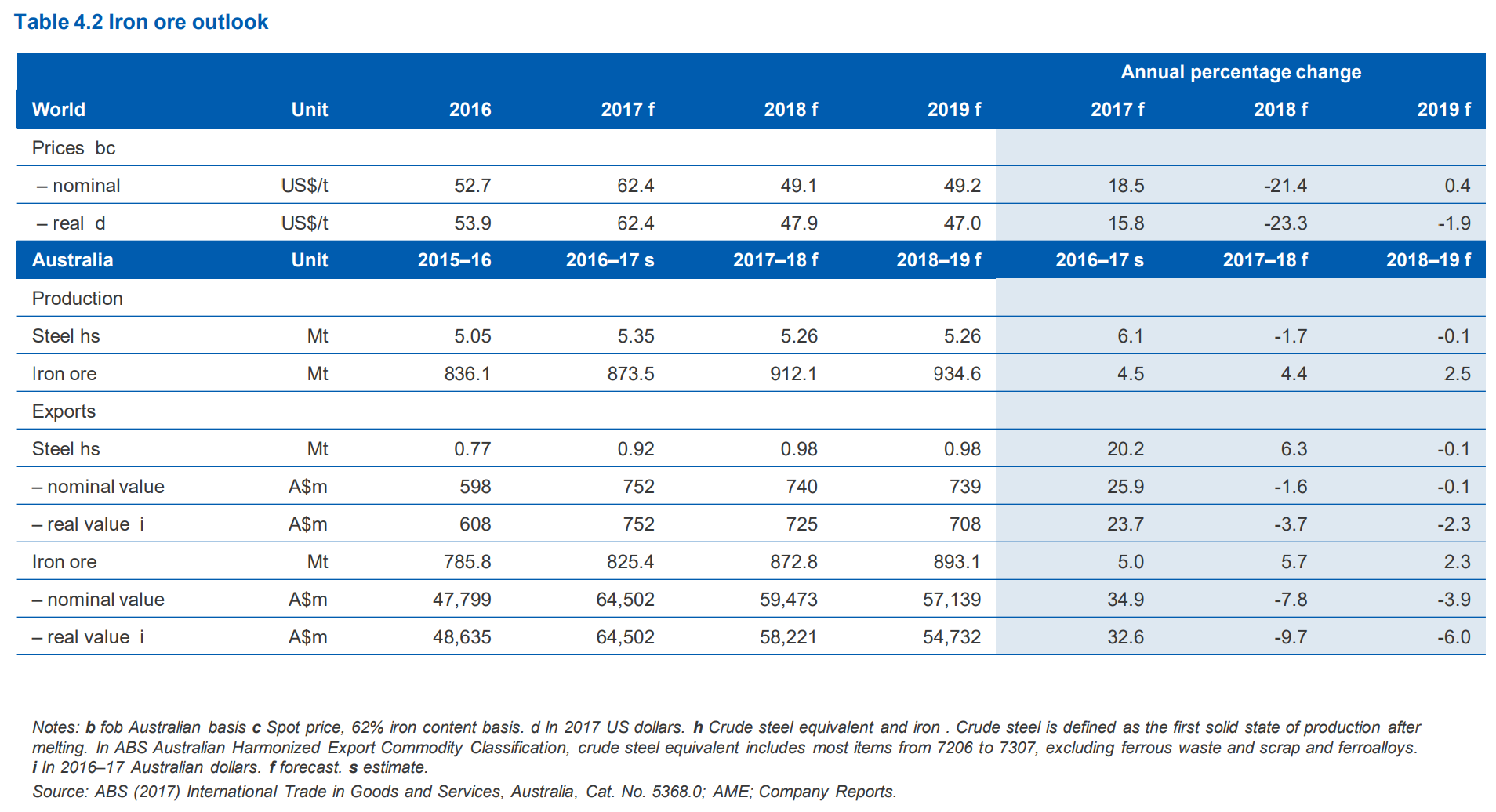

First, iron ore:

The iron ore price fell sharply in the June quarter, at one point reaching a 12-month low of US$47 a tonne (FOB Australia) in mid-June, before rebounding late in the month. While the decline in the iron ore price was expected, it occurred earlier than forecast in the March 2017 Resources and Energy Quarterly. As a result, the iron ore price forecast has been revised down from US$65 a tonne (average) to US$62 a tonne in 2017. The iron ore price is forecast to average US$55 a tonne in the second half of 2017. The recent strength of China’s steel sector (please refer to the Steel chapter) is expected to provide some short-term support. Nevertheless, the iron ore price is forecast to ultimately decline. Iron ore port stocks in China have steadily grown to record highs, reaching an estimated 140 million tonnes in June 2017. The seaborne iron ore market is forecast to remain well-supplied by low-cost producers in 2018 and 2019. Demand for iron ore is forecast to moderate over the same period, as steel production declines in China. High iron ore prices at the end of 2016 and start of 2017 resulted in a rebound in iron ore production in China and other nations, such as Iran. An extended period of low prices is likely to be required to displace the additional supply. The price forecast has been revised down from US$51 per tonne to US$48 a tonne in 2018, and to US$47 a tonne in 2019.

The Budget still has $55 FOB for 2018. You must add $5-6 for freight to convert to CFR spot equivalent. That’s more or less the price today.

Both are still too high. My guess is more like $40FOB for next year. BREE also has 38mt of volume growth in there which is dubious. Juniors will die and majors probably try to not to overproduce. I’d say half that is likely.

Advertisement

In sum, that reduces the outlook for iron ore revenues in 2018 by roughly 20% to $45bn.

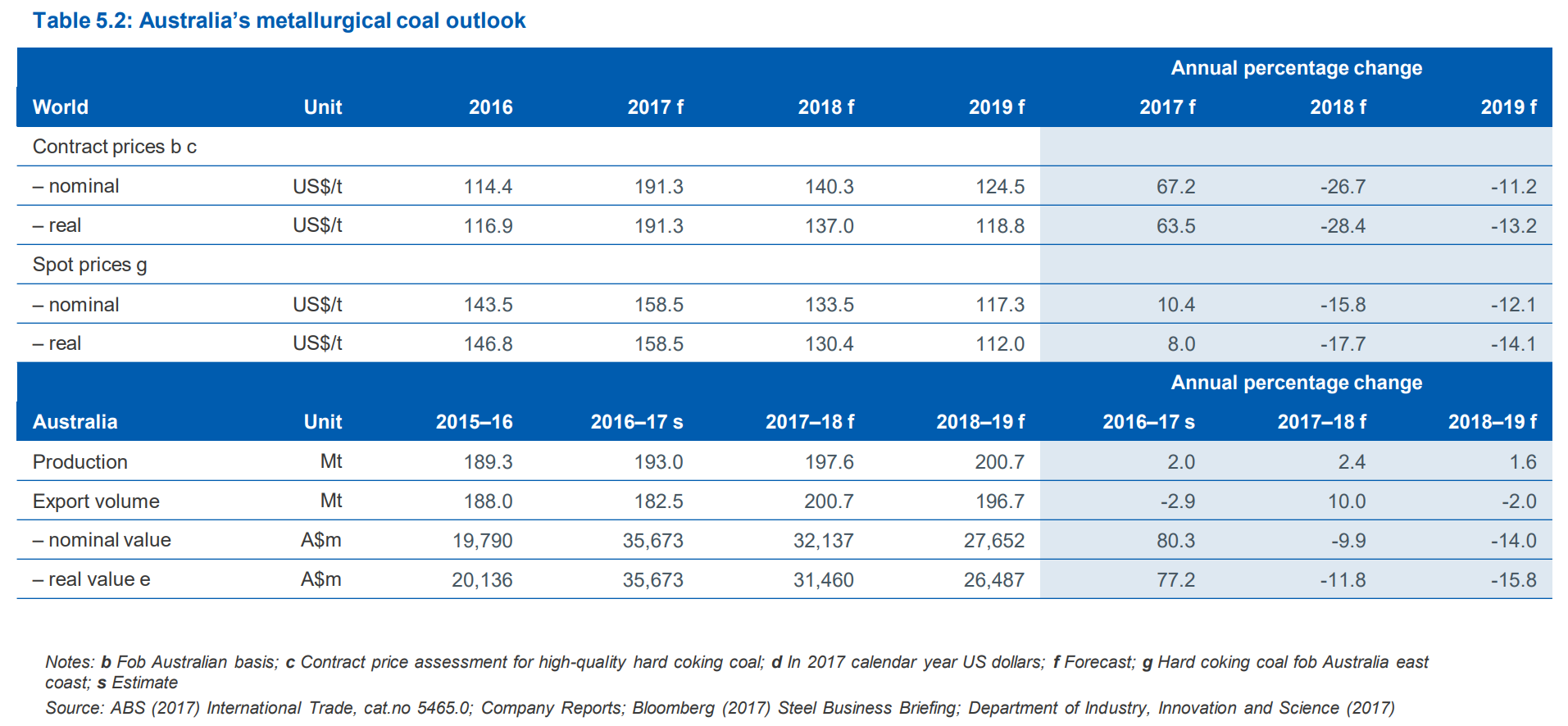

Coking coal is also too bullish:

The fall in price in the latter half of 2017 is expected to be driven by both increased metallurgical coal production in China and a return to average production levels in Australia. Price declines may also be exacerbated by further increases in metallurgical coal production at mines unaffected by Cyclone Debbie, as producers (even high-cost ones) respond to the (still relatively high) price level. Australian benchmark metallurgical coal contract prices are forecast to decline by 28 per cent in 2018, to US$137 a tonne. A further decline of 13 per cent to $US119 a tonne is forecast in 2019, as import demand and supply normalise. China is expected to be a large contributor to the improved balance between supply and demand, as its metallurgical coal production increases. Spot prices are expected to follow the same trend as contract prices, with an increase in the average price in 2017 but declines in 2018 and 2019. Premium hard coking coal spot prices are forecast to increase by 8.0 per cent in 2017 to US$159 a tonne. In 2018, premium spot prices are forecast to decline by 18 per cent to US$130 a tonne, with a further 14 per cent decline to US$112 a tonne forecast in 2019.

Not bad, just 20% too high pulling down 2018 earnings by $5bn or so.

Advertisement

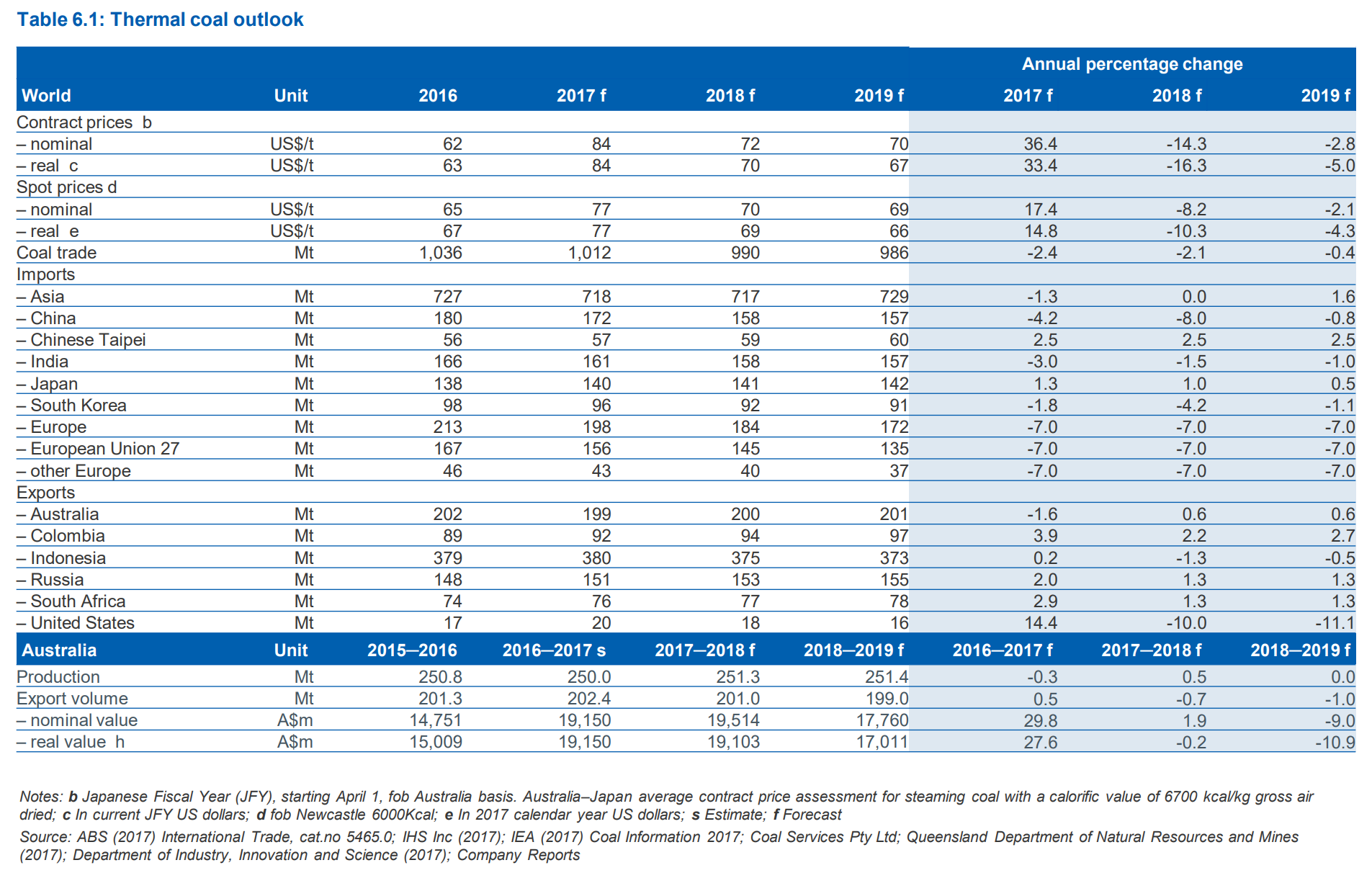

Thermal coal:

The JFY contract price is projected to decline over the outlook period, by 16 per cent to US$70 a tonne in JFY 2018, and by 5.0 per cent to US$67 a tonne in 2019. The falls in price are expected to be caused by declining import demand from China — as it moves to a more diversified energy mix — and by constrained import growth in India. Global benchmark spot prices are expected to follow the same declining trend as contract prices. In 2018, Australia’s Newcastle FOB spot price is forecast to decline by 10 per cent to US$69 a tonne, and decline by 4.3 per cent to US$66 a tonne in 2019.

Spot on my outlook.

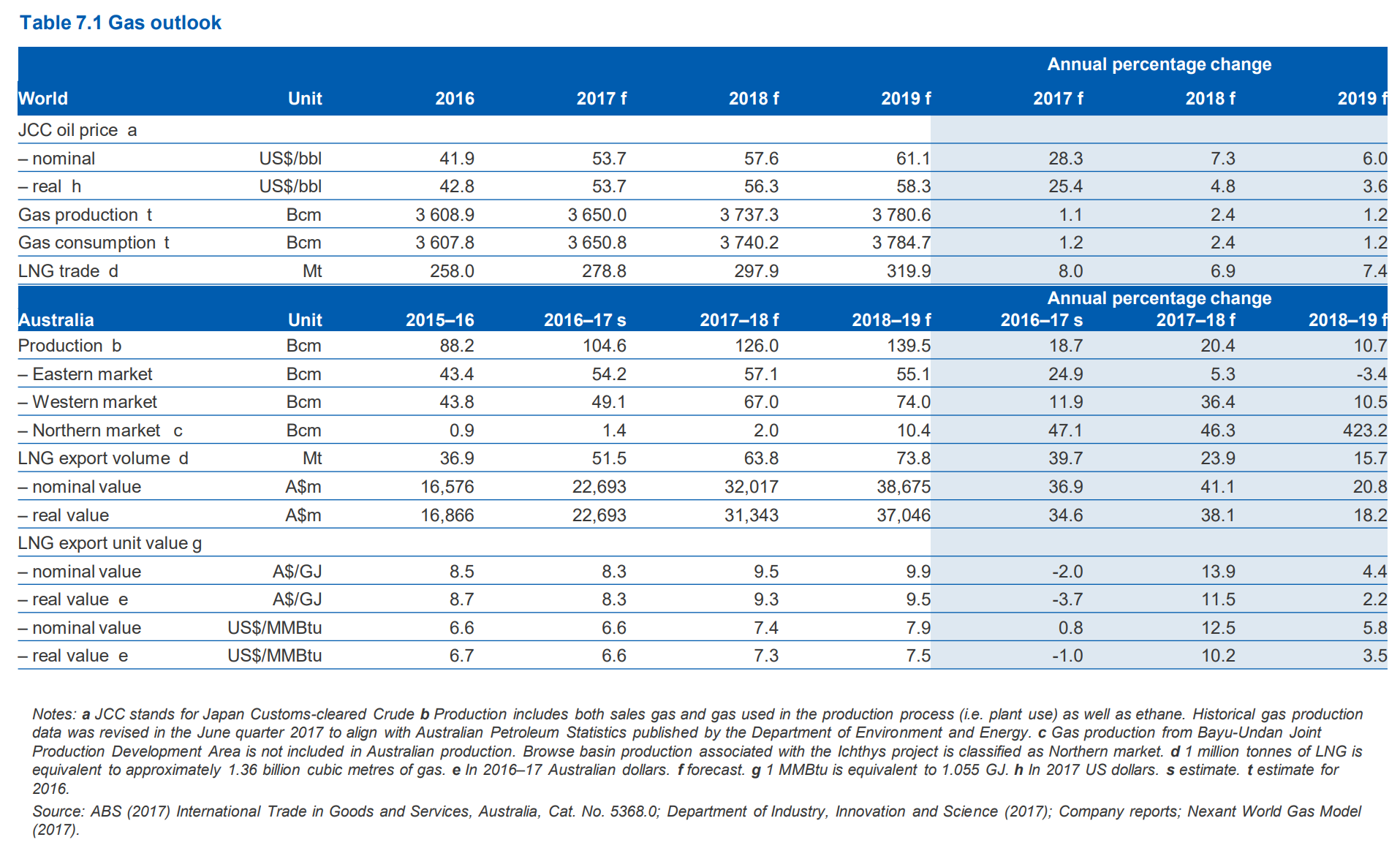

Finally, LNG:

Brent $57 is ten dollars too high, reducing earnings by $6bn or so.

Advertisement

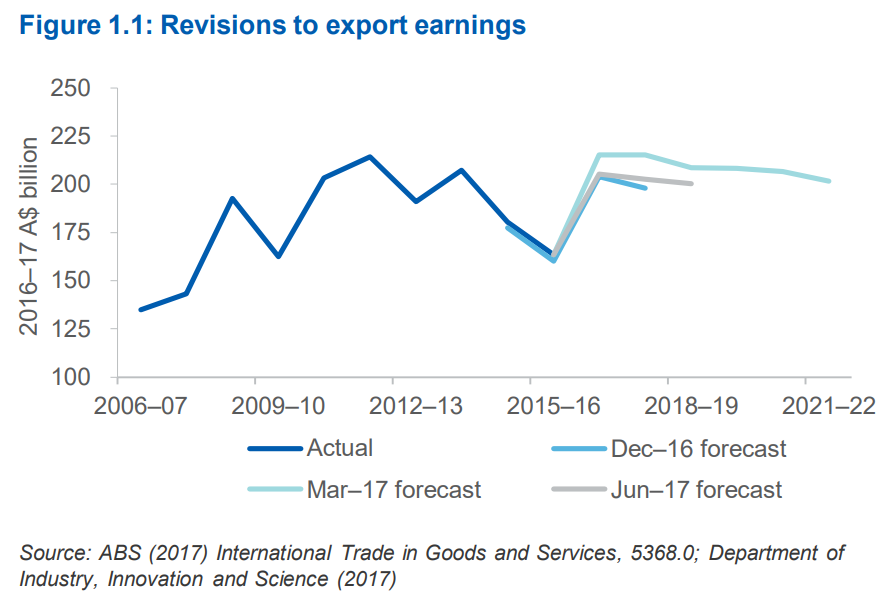

Total miss for BREE is roughly $22bn. HEre’s it’s outlook:

Since the March 2017 Resources and Energy Quarterly, the value of Australia’s resources and energy export earnings in 2016–17 has been revised down by $9.9 billion (4.6 per cent) to $205 billion. The downward revision primarily reflects an earlier than expected decline in iron ore prices since the March 2017 Resources and Energy Quarterly.

I’m seeing something around $180bn, roughly 14/15 year. Then down again the next year. Of course if China returns to more robust reform it will be worse or, conversely, kicks the can then it will be more like the BREE outlook. My numbers are a middle path.

Advertisement

It’s farewell Budget outlook, not just because of the hit to commodity revenues but because the multiplier effect is that wages will never rebound as hoped to boost bracket creep.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.