Special Report: Gerard Minack on when debt-stuffed Aussies will puke positions

Advertisement

Exclusively from Gerard Minack.

A housing boom prevented the 2014-15 commodity bust pushing Australia into recession. Now, however, pressure on consumer incomes is increasing the risk that even a moderate downturn in housing could cause a recession in 2018.

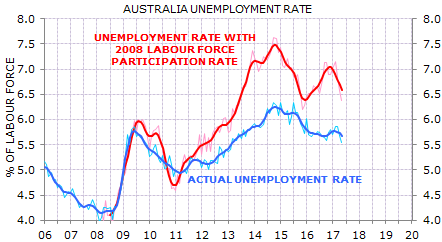

Australia coped well with the mining boom busting in 2014-15. Even so, growth has run below trend through most of the past 4 years, as evidenced by the rising unemployment rate. The degree of slack in the labour market has been partly obscured by declining labour participation (Exhibit 1).

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

Advertisement