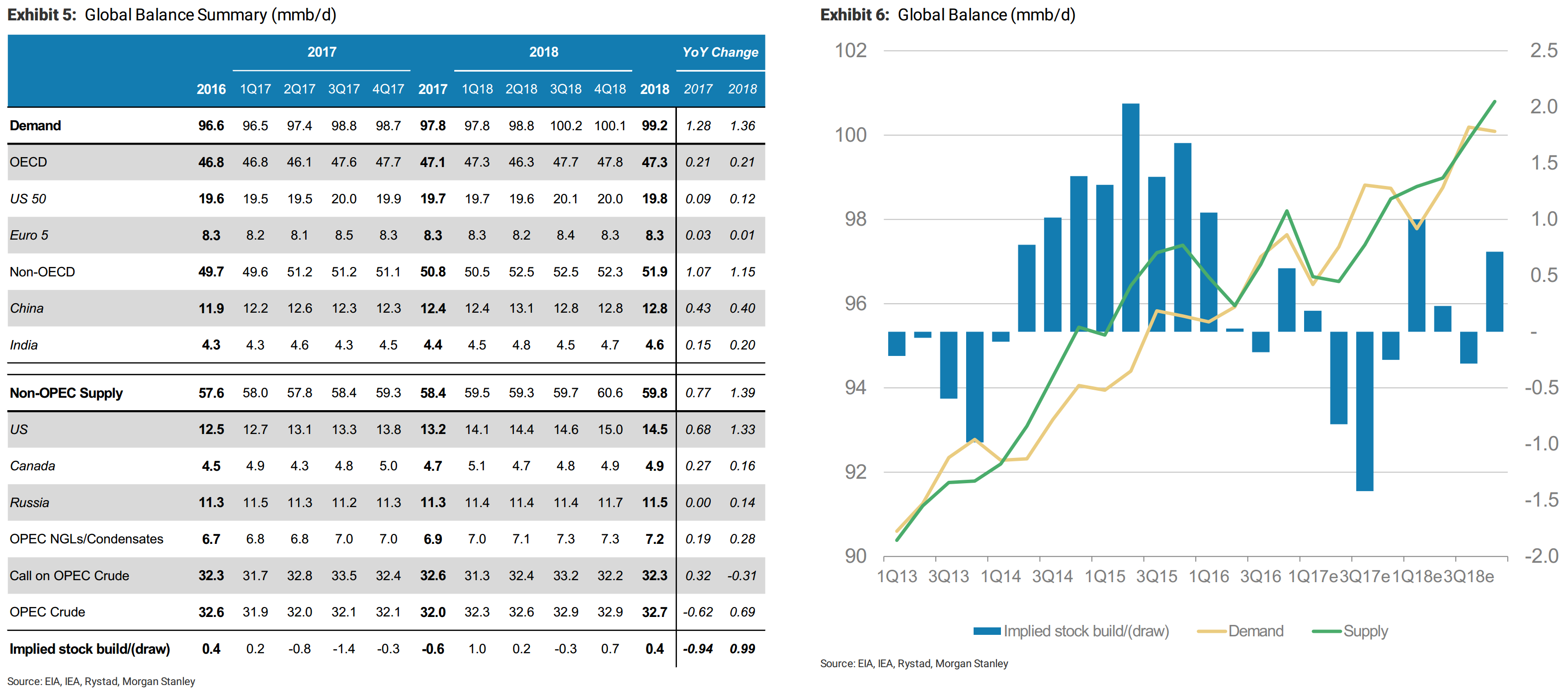

The return of oil inventories to five-year average levels was characterised this week by the IEA as “the currency used to express re-balancing”. We still expect some draws in 2Q/3Q but on our estimates, a return to five-year average stock levels remains elusive for some time to come.

The currency of rebalancing: Saudi Arabia’s oil minister Khalid al-Falih has described “bringing stock levels back to the five-year average”as the object of OPEC’s production cuts. Earlier this week, the IEA called it “the currency to express rebalancing”. It is indeed the case that current bloated stock levels – somewhere between 300-350 mln barrels above their five year average – are putting a firm lid on oil prices. In this note, we discuss whether a return to ‘normal’ levels is likely.

Recent data point sare not encouraging: Identifiable oil inventories – both crude and product in the OECD, China and selected other non-OECD countries – increased at a rate of ~1.0 mb/d in 1Q. This week, the IEA mentioned that OECD inventories continued to build in April at a rate of 620 kb/d, which is above the seasonal norm. Weekly data, which is only available for a much smaller sub-set of countries,has shown onshore stocks continuing to build since the end of April at a rate of ~130 kb/d, partly due to a staggering increase of 1.6 mb/d over the last two weeks. This does not include floating storage, which is also on the rise again, building at a rate of ~0.8 mb/d since early May. On top, we discussed the high level of tanker loadings in last week’s note. Even since then, this has increased further: so far this month, over 52 mb/d has been loaded on tankers,a record since at least 2012.

On our estimates, stocks draw around 3Q but build again in 2018: Still,a seasonal upswing in demand means that oil inventories will probably decline during the rest of the year, mostly during 3Q. However, we see this reversing in 2018 as strong growth from US shale will likely coincide with rising production from OPEC and Russia after expiry of the current output agreement in 1Q18. We do not expect that OPEC will ‘flood the market’, but on current trends,even a partial unwind of recent cuts will likely see the market oversupplied again next year. Our base case forecast is for inventories to build in 2018 at a rate of 0.4 mb/d.

This suggests oil inventories will not reach their five-yearaverage: Exhibit 2 highlights what this means for global stocks. We estimate observable inventories at ~4.13 bn barrels at the end of April, which is 340 mln barrels above the five year average of 3.79 bn. On our estimates, inventories will fall to ~3.93bn bbl by the end of the year,eroding slightly over half of the current excess over the five year average. However,after that inventories build again back to 4.1 bn bbl by end 2018. Unless the US oil rig count declines substantially and US shale production rolls over, we estimate that OPEC would need to continue its current quota for the entirety of 2018 to prevent an inventory increase, or would need a much deeper cut to see inventories decline back to their five-year average.

The back-end of thecurveis still anchored by $50-55, but if thestructure needs to be in contango, theshortend naturallytrades below that: Exhibit 4 shows how the forward curve has changed over the last month. We believe this chart summarises the current market dynamics. The long-end of the curve seems anchored by $50-55/bbl, which roughly corresponds with the break-even of US shale. However,even four weeks ago, the market expected that OPEC could create some tightness in oil markets during 2018, which would require inventories to draw and hence a backwardated curve. That putupward pressure on the short end of the forward curve.

At the moment however, this no longer seems to be the case. Stocks are likely to build again next year, which requires contango across the entire forward curve. The long-end is still supported at $50-55, but the need for a contango structure has driven the short end well below $50/bbl. Unless the case for inventory draws next year becomes stronger, this is likely to remain the case.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

The return of oil inventories to five-year average levels was characterised this week by the IEA as “the currency used to express re-balancing”. We still expect some draws in 2Q/3Q but on our estimates, a return to five-year average stock levels remains elusive for some time to come.